BoE Review: Being Careful Amid Data Conflicts

Even amid a BoE rate cut last month that was delivered with a clear(er) degree of action, all MPC members opting for easier policy. Even so, it was clear there were still MPC divisions that probably reflected increased uncertainty enough for the BoE to have altered its rhetoric somewhat to stress the need for policy to be framed carefully as well as gradually, wording reused this time around. Indeed, this shift very much pointed to what has turned out to be stable policy (Bank Rate still at 4.5%) at this March meeting, with it increasingly likely that the MPC majority envisages rate cuts no faster than every quarter this year and a little further into 2026 but with no pre-set path being considered – at least openly. The BoE still believes that policy needs to remain restrictive, with the appropriate degree of restrictiveness to be decided at each meeting.

Given what we think is a flailing real economy backdrop, which growing global trade tensions may only accentuate, BoE easing may yet come faster and further as the BoE reassess its optimism about growth and upgrades its estimate extent of slack – particularly in the labor market (Figure 1). Indeed, the likelihood is that additional fiscal and trade details due by the May MPC meeting, alongside the already frail real economy backdrop, may persuade the BoE into a further growth downgrade. Thus we see at least three more moves this year and possibly four.

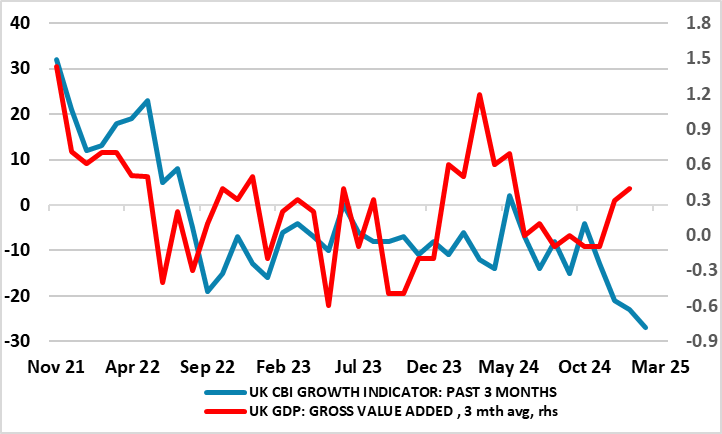

Figure 1: Surveys Pointing South!

Source, ONS, CBI

Data Conflicts on Growth…

Indeed, it does seem as if, while not being entirely rosy, the BoE is showing optimism not supported by data. It suggested it saw GDP growing around ¼% q/q, higher than the 0.1% that had been incorporated in the February Report. Such a growth rate tallies with actual GDP numbers to date but as the BoE admit present a stronger picture than the combined steer from business surveys (Figure 1) and that this is probably more representative of the underlying rate of growth. Indeed, its own survey data (ie the Bank’s Agents) had reported that activity remained subdued, with weak consumer and business sentiment perceived as the main barrier to growth.

…And On Wages

In addition, the alleged strength in pay as denoted by circa-6% growth in average earnings looks suspect – HMRC data suggest growth nearer 5%. But it may be even weaker certainly in terms of pay deals as the BE has acknowledged. Data from the Bank’s settlements databases suggested that the median rate of pay awards had remained at around 3 to 4% in the three months to February, while latest intelligence from the Agents suggested average pay rises for 2025 of 3.5% to 4%, consistent with the average of 3.7% reported in the Agents’ annual pay survey conducted ahead of the February Report. The latest Decision Maker Panel (DMP) survey had reported that businesses’ pay growth expectations for the year ahead had remained at 3.9% in the three months to February.

Reassessment Looming?

The last set of BoE forecasts were notable for one possibly major thing – an assumption that underlying growth has fallen, possible to under 1%, much to do with the labor market. This does not explain all of the higher inflation profile which it pointed to in last month’s Monetary Policy Report that now only delivers a below target outcome into 2028 – the higher rates projected this year reflect higher energy and regulated prices. Admittedly energy prices have fallen back since and markedly so but this is unlikely to calm what if anything may be a greater inflationary concern among the MPC majority. Indeed, pseudo MPC-dove Dep Gov Ramsden has very much flagged an increased worry about possible inflation persistence based around recent wage data, albeit what we think are still dubiously accurate ONS numbers as suggested above.

But at the moment and in somewhat contrast to its view about supply and demand, the MPC is currently focused on two particular risks. First, the extent to which there could be greater or longer-lasting weakness in demand relative to supply in the economy. Second, the extent to which there could be more persistence in domestic wage and prices, The MPC would review the evidence on the impact and likelihood of these broad risks as a part of its May policy round, thereby updating and re-weighting its scenario outlook

Scenario Shifting

Admittedly, the BoE is also aware of these risks, hence why it believes the outlook is more uncertain and enough so that it has to suggest that policy will have to be conducted carefully as well as gradually - with a clear debate about the wording of guidance evident from the minutes. This may explain the dissents even though this migrated back to just one such dissent this time around. What is clear is that the MPC is still keen on offering alternative scenarios. Hitherto, the first case saw remaining persistence in inflation dissipate quickly as pay and price-setting dynamics continued to normalise following the unwinding of the global shocks that had driven up inflation. In the second case, a period of economic slack might be required to normalise these dynamics fully. In the third case, some inflationary persistence might also reflect structural shifts in wage and price-setting behaviour.

As suggested above, it seems that the MPC majority is now leaning more toward the latter two scenarios, hence a more hawkish leaning. However, we think that real economy consideration will come increasingly to the fore in coming months both by a weak data backdrop (now including survey data suggesting a hitherto solid construction sector has gone into reverse) and where the fiscal stance is likely to become an issue as the government considers tightening welfare payments and other spending in order to meet fiscal goals.