FX Daily Strategy: N America, December 17th

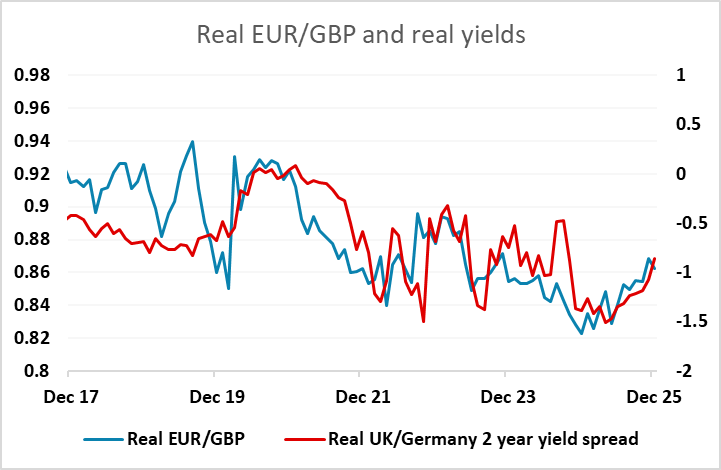

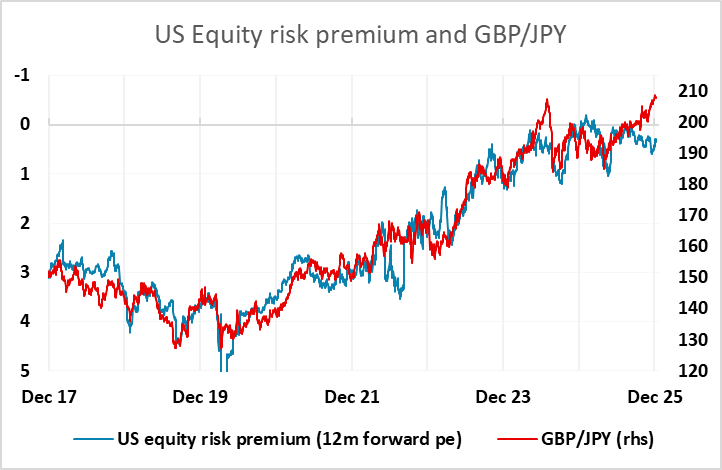

UK CPI a downside risk for GBP

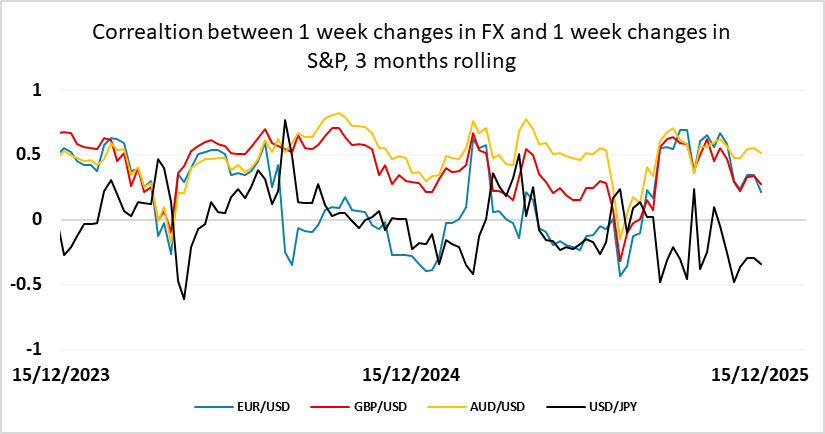

Softer equities to weigh on riskier currencies

JPY to benefit in more risk negative conditions

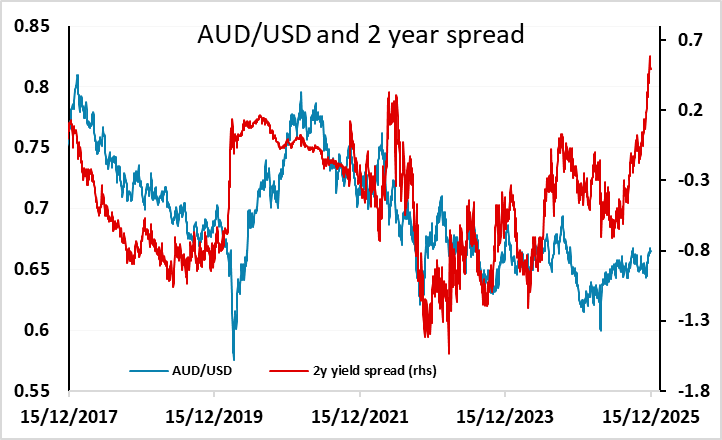

AUD still represents value

UK CPI a downside risk for GBP

Softer equities to weigh on riskier currencies

JPY to benefit in more risk negative conditions

AUD still represents value

UK November CPI has come in significantly below expectations at 3.2% y/y for both the core and the headline. This should remove any doubt that the BoE will cut rates tomorrow - this was already 90% priced in, but there should now be no uncertainty. But combined with the weakness of private sector pay growth in the labour market data yesterday, the continued decline in employment and the declines in GDP in the last two months, this should increase the chances of more aggressive easing in the next year. With just 60bps of easing priced into the market, including the expected cut tomorrow, there is scope for further cuts to be priced in based on the weakness of the data. The stronger PMI data yesterday was seen as GBP positive, but we regard this data as having very little credibility given the lack of correlation with official data.

GBP has slipped a little lower in response to the CPI data, but the decline is quite modest and we see scope for a more substantial decline which may come after the BoE MPC meeting tomorrow which we would expect to deliver a dovish message along with a rate cut. We would still see scope for the 0.8865 high of the year in EUR/GBP to be tested before the end of the year, while GBP/JPY also looks dramatically overvalued and ought to have scope to drop well below 200.

EUR/USD tested above 1.18 on Tuesday but fell back as equities softened after the weaker than expected US PMI data. The European data had also been softer, but the weakness in the US data led to some weakening in equities which generally undermined the riskier currencies. The JPY continues to look the best placed of the majors in these circumstances, with a rate hike still odds on this week and, more importantly, risk sentiment starting to turn a little weaker. The US numbers aren’t particularly bad, but still suggest modest growth and slowing employment growth, which are insufficient to justify the current equity valuations even with AI optimism. Softening equities can be expected to continue to weigh on riskier currencies if we don’t see any significant response in lower US yields.

We continue to see value in the AUD, even though its upside will be restricted as long as equities struggle. Yield spreads reman extremely favourable, and modest softening in equities ought not to be enough to prevent a retest of the highs of the year above 0.67. But in a more risk negative environment, the JPY ought to be the best performer.