FX Daily Strategy: Europe, March 19th

BoJ kept rates unchanged

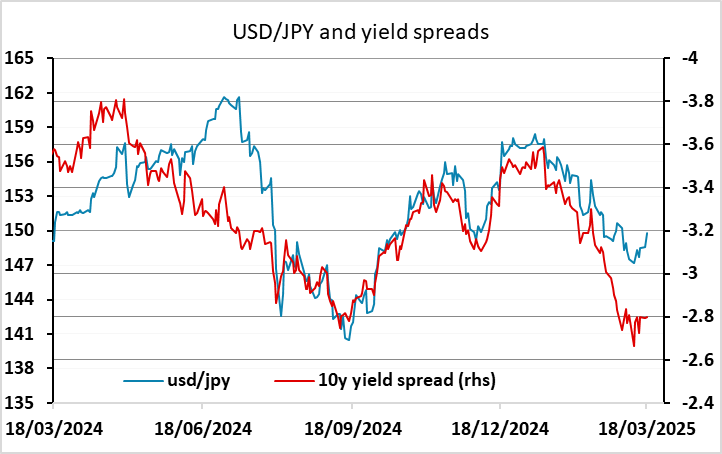

JPY can recover some recent lost ground

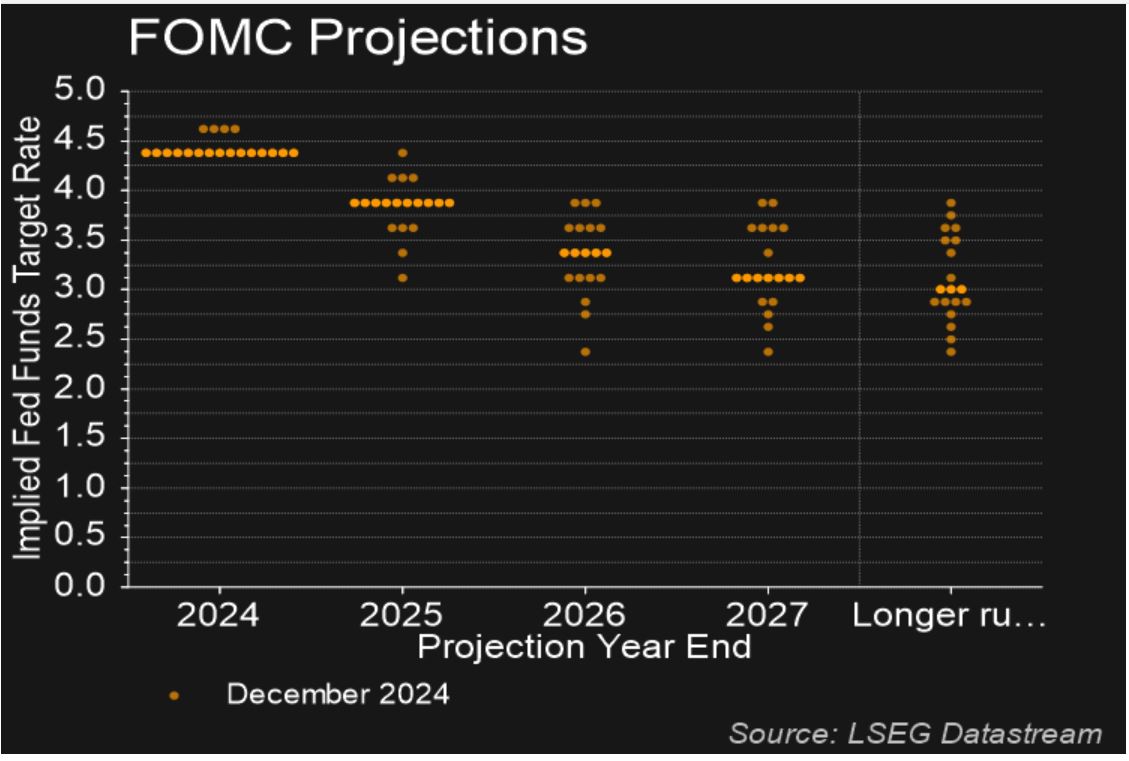

Fed to remain on hold given major uncertainties

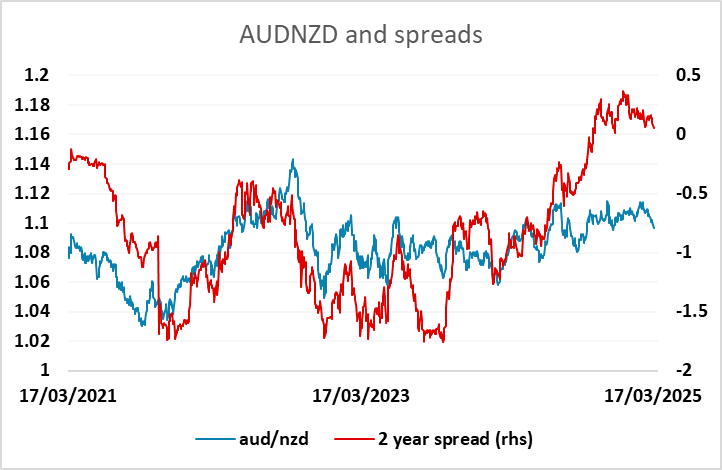

NZD may have downside risks against the AUD unless GDP is unexpectedly strong

BoJ kept rates unchanged

JPY can recover some recent lost ground

Fed to remain on hold given major uncertainties

NZD may have downside risks against the AUD unless GDP is unexpectedly strong

Wednesday kicks off with the BoJ meeting. The market isn’t pricing in any risk of action, and indeed is only pricing in around 5bps of tightening for the May meeting with the first 25bp rate hike not fully priced in until the October meeting. This looks overly conservative, as the BoJ comments have remained on the hawkish side, and provided that we see the spring wage round deliver the wage hikes that are publicly being agreed, we would expect he BoJ to rise rates in May as long as there isn’t a major deterioration in the global growth outlook in the intervening period.

While we don’t expect a rate hike at this meeting, we do see some risk of hawkish remarks from Ueda's press conference relative to market pricing, perhaps even suggesting the likelihood of a May rate hike if things turn out as forecast. There is therefore potential for a boost for the JPY from the meeting, and given that there is so little tightening priced in, there isn’t much risk of a negative JPY impact. However, the JPY has been under a little pressure in the last couple of days, and momentum may remain JPY negative if the BoJ meeting doesn’t impact market expectations, with the JPY suffering from a combination of long positioning and positive risk sentiment. But we would still see very little further JPY downside form here, and moves above 150 in USD/JPY and 164 in EUR/JPY should be seen as a medium and long term selling opportunity.

And The Bank of Japan has left policy unchanged as expected at 0.5% with little forward guidance. They seems to be optimistic about consumer spending despite inflationary pressure and limited evidence to show momentum from household spending. The BoJ only sees inflation expectation to be align in a medium run, which is an interesting take after they hike in January and would be up to be interpretation for Ueda in his press conference.

The FOMC meeting is the other main event of the day, but is similarly unlikely to deliver any change in policy. In the current exceptionally uncertain environment, the FOMC is also unlikely to give much away on future policy. The dots will be closely watched but we expect they will change little from January 29. Powell is likely to stress at the press conference that policy will be responsive to incoming data and the dots should not be seen as a plan. The January dots showed a median expectation of 2 more cuts this year, and the market is currently pricing in a further 59bps, so there is some marginal scope for US short term yields to rise on unchanged policy, but we doubt this will have much FX impact. There will be sensitivity to anything Powell has to say on tariffs and the impact on inflation and growth, but knowing this Powell can be expected to be very cagey.

Later on there is NZ Q4 GDP, which we expect will show positive growth, ending the recession seen in H2 2024. The RBNZ is still priced to cut another 50bps off rates this year, and this is likely to remain the case unless the data is exceptionally strong. However, we still see some downside risks against the AUD, which has underperformed relative to yield spreads and will benefit if we see more strength in Asian equities.