FX Daily Strategy: APAC, December 20th

US to hold most of its post-FOMC gains

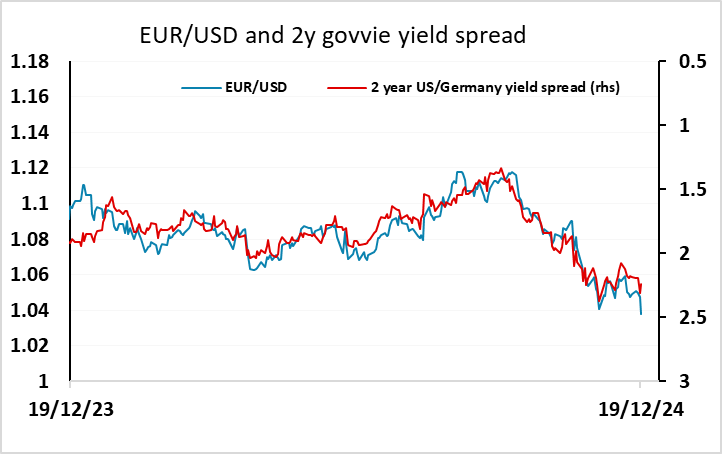

Some scope for EUR recovery based on yield spread metrics

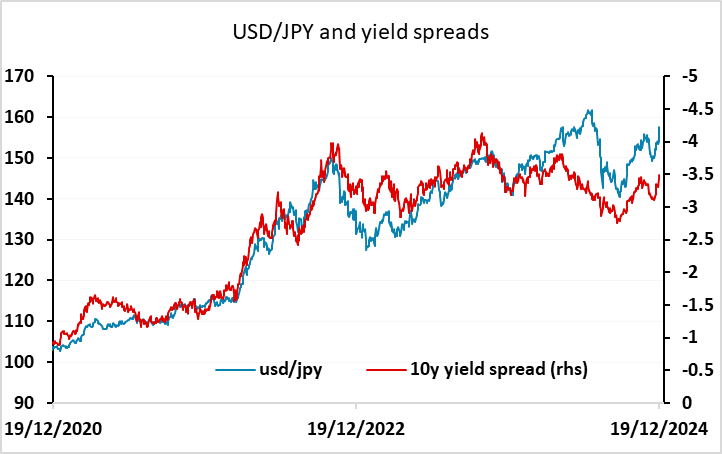

JPY still struggling

GBP has scope to fall further but retail sales may be mildly supportive

US to hold most of its post-FOMC gains

Some scope for EUR recovery based on yield spread metrics

JPY still struggling

GBP has scope to fall further but retail sales may be mildly supportive

After all the events of this week, Friday is a much quieter day, with no central bank meetings and no data of any great import, although the November PCE price index and the UK retail sales data will be of some interest.

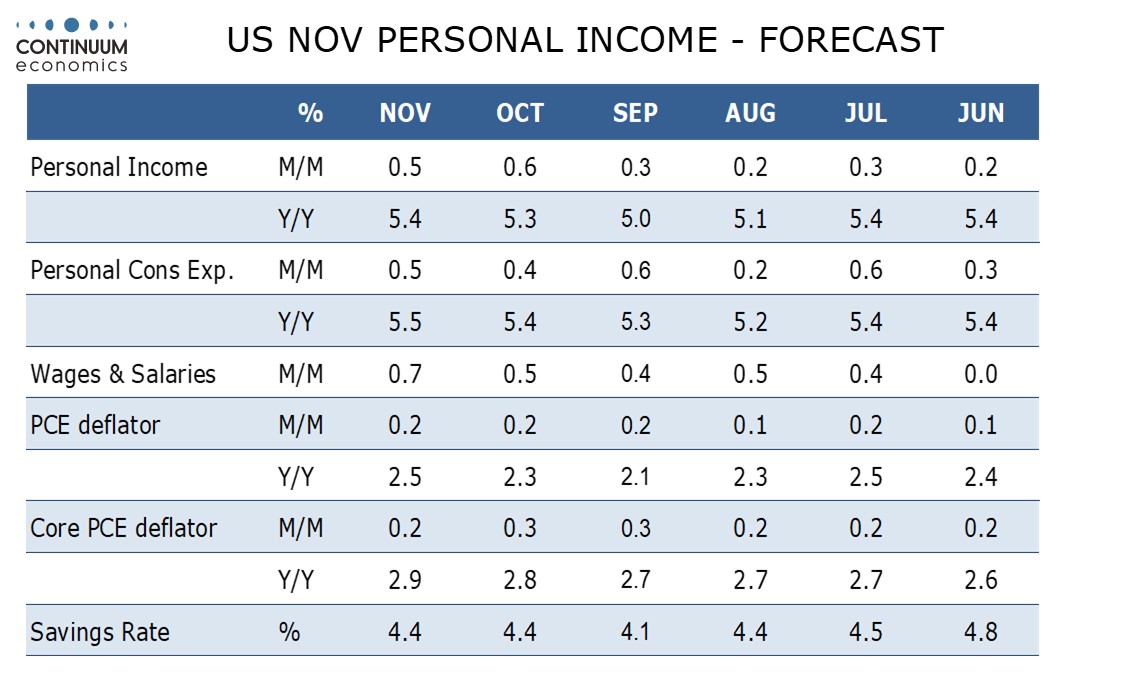

We expect November to see a 0.2% increase in the core PCE price index, underperforming a 0.3% core CPI as is usually the case but was not so in September and October. We expect 0.5% increases in personal income and spending. Core CPI has seen four straight gains of 0.3%. While September and October saw the core PCE price index match the CPI (though marginally underperforming before rounding) August saw only a 0.2% rise in core PCE prices, and lower still before rounding. We expect core PCE prices to underperform the core CPI once again in November. This is in line with market consensus, but may nevertheless serve to pause the rise in US yields that we have seen since the FOMC, which is starting to look a little overdone. There may therefore also be some correction to recent USD strength, although any significant reversal is likely to require a decline rather than a stabilisation in yields.

EUR/USD is underperforming the moves in 2 year yield spreads, and may have scope to recover above 1.04. USD/JPY is moving in line with the yield spread correlation that has heled since August, so may not have much downside scope, although longer term correlations suggest current levels are too high. The rise in US yields has also led to a new low in the nominal US equity risk premium, despite the decline in equities that it has engendered, and this is likely to maintain downward pressure on JPY crosses, supporting gains in EUR/JPY. Even though it is hard to be comfortable with USD/JPY at these extreme levels, where the Japanese authorities have been prepared to intervene in the past, the lack of concern from the BoJ at the short term consequences of their rate decision for the JPY makes it hard to believe we will be seeing any official opposition to current JPY weakness.

UK retail sales are expected to edge higher in November after a sluggish couple of months, which would maintain a positive and improved if still quite modest underlying trend. GBP fell back a little after the BoE MPC meeting and could still fall further as the market’s pricing of just 50bp of BoE easing in 2025 looks at odds with weakening data and a more dovish than expected voting split. While the current pricing of BoE policy is similar to that for the Fed, economic data suggests it should probably be close to the ECB, and if that were the case UK yields and GBP could be expected to move significantly lower.