FX Daily Strategy: Asia, February 21st

Eurozone PMIs may limit the EUR upside

GBP may also struggle on weak PMIs and retail sales data

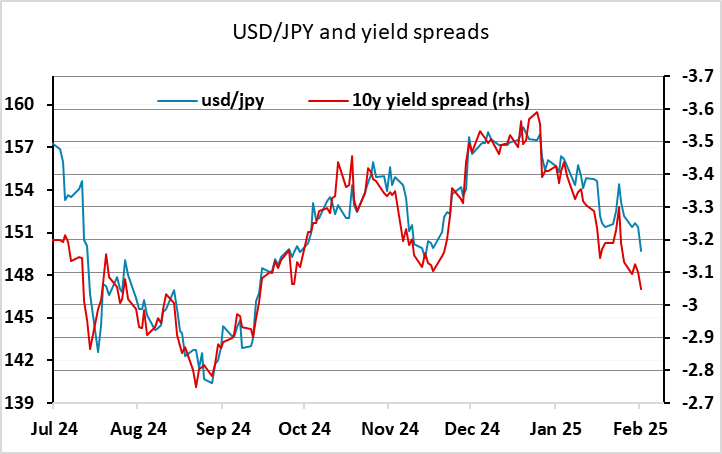

The JPY remains well bid but is approaching important resistance levels

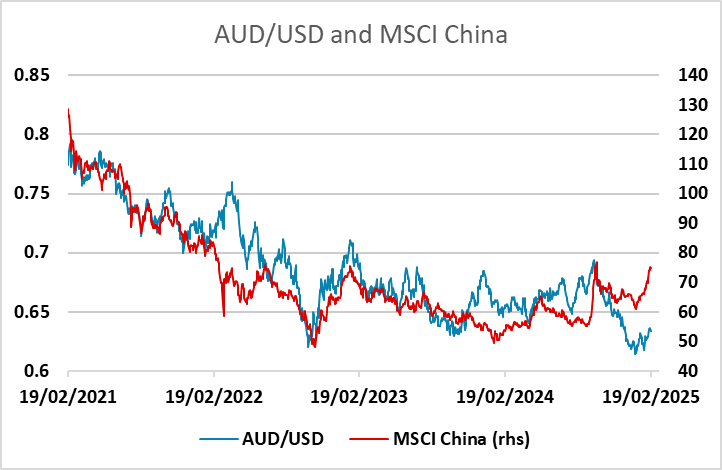

AUD can also outperform if Asian equities are resilient

Eurozone PMIs may limit the EUR upside

GBP may also struggle on weak PMIs and retail sales data

The JPY remains well bid but is approaching important resistance levels

AUD can also outperform if Asian equities are resilient

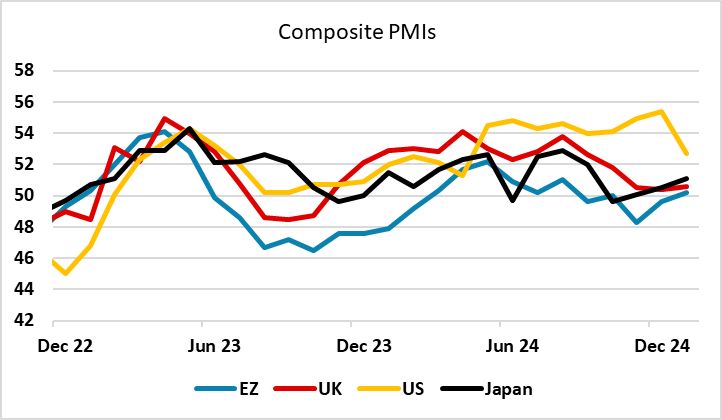

PMIs are likely to be the main focus on Friday, with the European data as usual the main focus. January’s Eurozone composite PMI rose 0.6 point to 50.2, the first monthly increase in private sector business activity since August last year. A slower fall in factory production was central to January’s overall tepid expansion, sector data showed, as services activity posted a slightly softer rise on the month. We see no further improvement in the composite, while the consensus is for a small rise, so the EUR may struggle in the face of continued soft data.

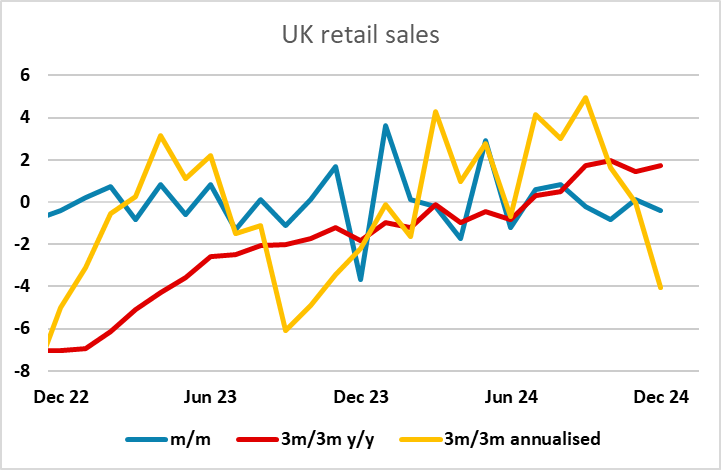

The UK PMI data are already pointing to weakening business optimism and we see the headline edging back down slightly, these coming just after GfK consumer confidence readings but alongside retail sales data for January where cold and stormy weather may result in another soft outcome. GBP has performed well in the last couple of weeks against both the USD and the EUR, helped by the stronger than expected employment and CPI data earlier this week, but evidence of a weak economy in the OMI and retail sales data may lead to GBP slipping back, with EUR/GBP potentially seeing a rise back above 0.83.

The USD was soft on Thursday despite a lack of news, with the JPY performing particularly strongly helped by some tariff induced weakening in risk sentiment. Threats of tariffs on pharma, cars and semiconductors as well as the reciprocal tariffs already promised cover all the US’s trading partners, and the net impact on currencies is likely to be less about which country suffers most from tariffs than what the impact s on global growth and risk sentiment. There seems little doubt that any tariff imposition will be negative for risk and thus positive for the JPY. But even without much weakness in risk appetite, yield spreads have narrowed sufficiently to justify USD/JPY progress sub-150. Even so, we are hitting some key technical levels in USD/JPY and JPY crosses so further downside may require some clear news.

Along with the JPY, the AUD continues to make good progress and hit another new high for the year on Thursday. Of course, the AUD will tend to require positive rather than negative risk sentiment if it is to advance, and is also close to important resistance at 0.64. But there is much less good news priced into Asian equities than US equities, and if these prove resilient yield spreads remain at levels that suggest scope for AUD gains.