FX Daily Strategy: N America, Sep 17th

FOMC likely to cut 25bps but dots may disappoint the doves

USD risks consequently on the upside

BoC may be more dovish than expected, suggesting USD/CAD upside risks

GBP little changed after marginally softer UK CPI

FOMC likely to cut 25bps but dots may disappoint the doves

USD risks consequently on the upside

BoC may be more dovish than expected, suggesting USD/CAD upside risks

GBP little changed after marginally softer UK CPI

Wednesday is a very busy day, with the FOMC decision the highlight, but also a BoC rate decision and UK CPI as a focus for the European morning ahead of tomorrow’s BoE meeting.

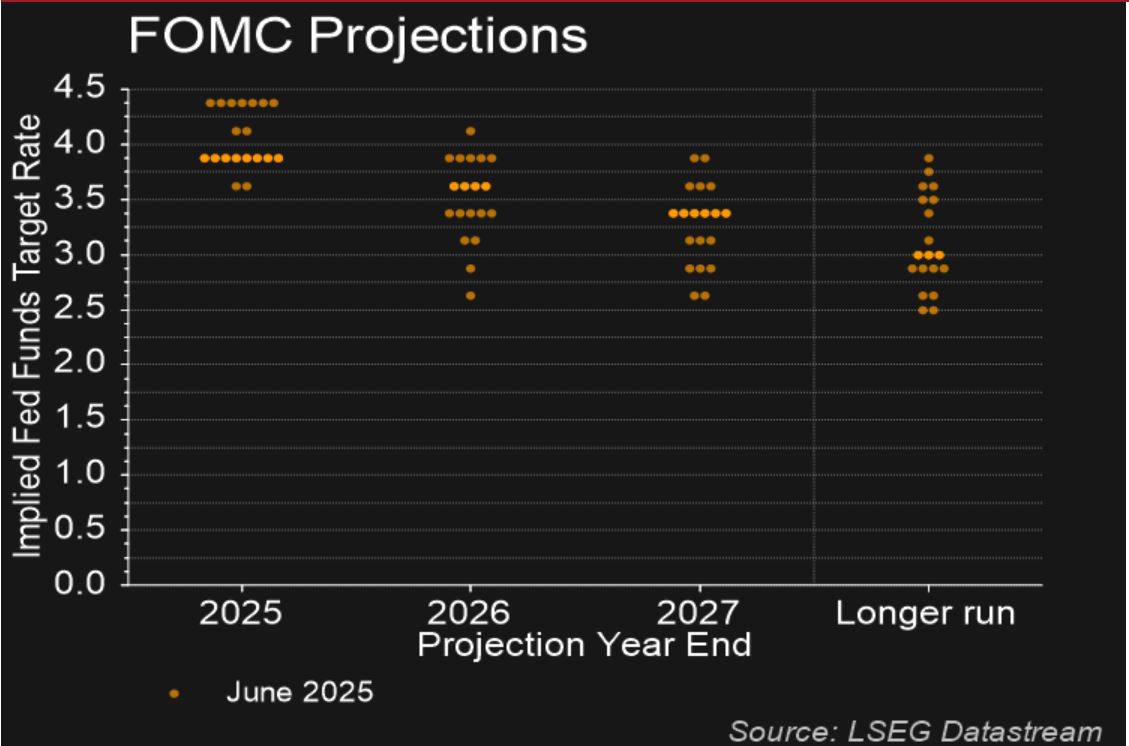

We expect a 25bps easing to a 4.0-4.25% Fed Funds target range at the FOMC meeting. The FOMC will continue to see similar upside risks to inflation but increased downside risks to the labor market. The dots are likely to continue to expect only one more move in 2025, but three moves in 2026 rather than one as was the case at the June FOMC, which would take the rate close to neutral. The risks to this view look to be towards a less dovish Fed than expected, as the extra 50bps of easing in 2026 is not necessarily easily justified by the most recent data despite the softer employment data we have seen. The market is pricing in 146bps of easing by the end of 2026, which is (nearly) an extra 25 bps over our expectations, and 75bps more than easing seen by the median dots at the June meeting.

The USD has been weakening in the run-up to the meeting, with EUR/USD hitting a new high for the year on Tuesday, even though there wasn’t much movement in US yields. Indeed, the US retail sales data was on the strong side, and didn’t encourage expectations of more aggressive Fed easing. The risks therefore look to be towards a USD recovery on Wednesday, albeit not necessarily a large one, as the market is likely to cling on to a more aggressive easing view than the Fed dots suggest. If we do see somewhat higher US yields, there could also be a negative impact on the equity market. The S&P 500 hit another new all time high on Tuesday, and looks ripe for a correction. The riskier currencies, which have been the main beneficiaries of USD weakness this week, could therefore be then most vulnerable.

We also expect to see a 25bp rate cut from the BoC, in line with market consensus. While surveys only have a little below 80% of forecasters looking for a rate cut, the market is pricing a cut as a 95% chance, and some of those calls may now be out of date. After the Bank of Canada’s last meeting on July 30 we expected rates to be left on hold in September before easing resumed in October. However, data since that meeting having been mostly weak, so a 25bps easing to 2.5%, the first move since March, now looks likely his time. We expect two more easings from the BoC, in Q4 2025 and Q1 2026, which would take the rate down to 2.0%. The market is slightly less aggressive, pricing a total of 60bps of easing by the end of next year, so the CAD may suffer if the BoC presents a dovish stance along with the rate cut.

UK August CPI data has come in slightly softer than expected, with the core rate down to 3.6% y/y from 3.8% in July, against a market consensus of 3.7%. Air fares, which boosted the index in July, fell back in August and were the main reason for the lower than expected number. However, the headline CPI was in line with consensus at 3.8% y/y.

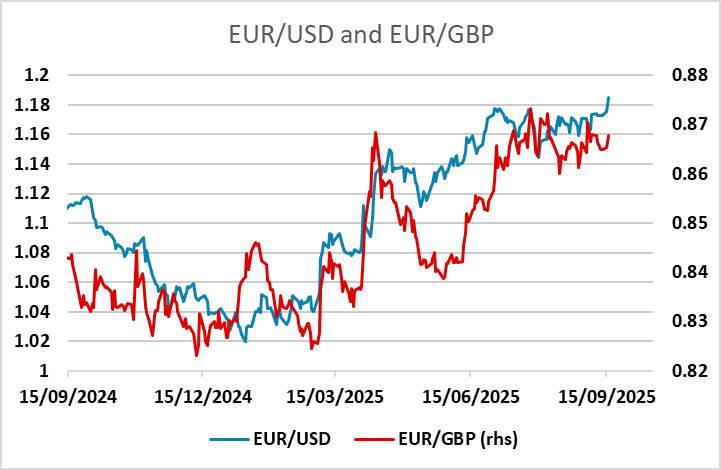

GBP is little changed in response to the data. EUR/GBP firmed up in the North American session yesterday, challenging the top of the range at 0.87, but there has been only a marginal reaction to the UK data, which certainly won’t make any real difference to Bank of England thinking. There is still next to no chance of any rate cut at tomorrow’s MPC meeting. There is therefore no clear rationale for a break of the 0.86-0.87 range, but the gains yesterday came on the back of general EUR strength, itself related to underlying USD weakness. If we see more USD weakness following today’s FOMC, there is scope for EUR/GBP to break higher, but as we note in today’s daily, the risks on the FOMC may be on the USD upside, as there is a lot of easing priced in and the Fed dots are likely to fall short of market pricing.