FX Weekly Strategy: March 24th-28th

JPY still has potential for gains unless market sentiment improves

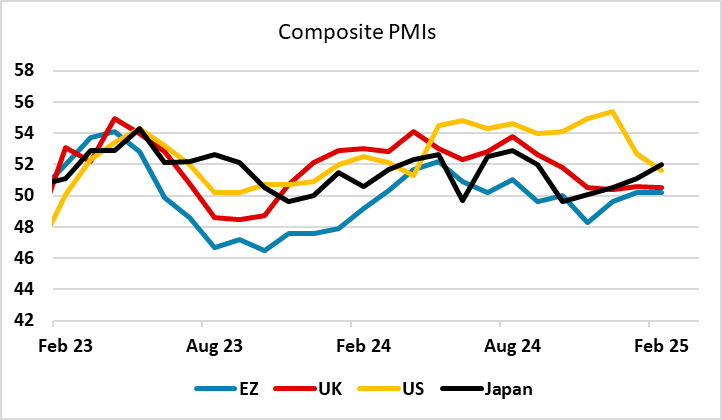

EUR may get some support from PMIs

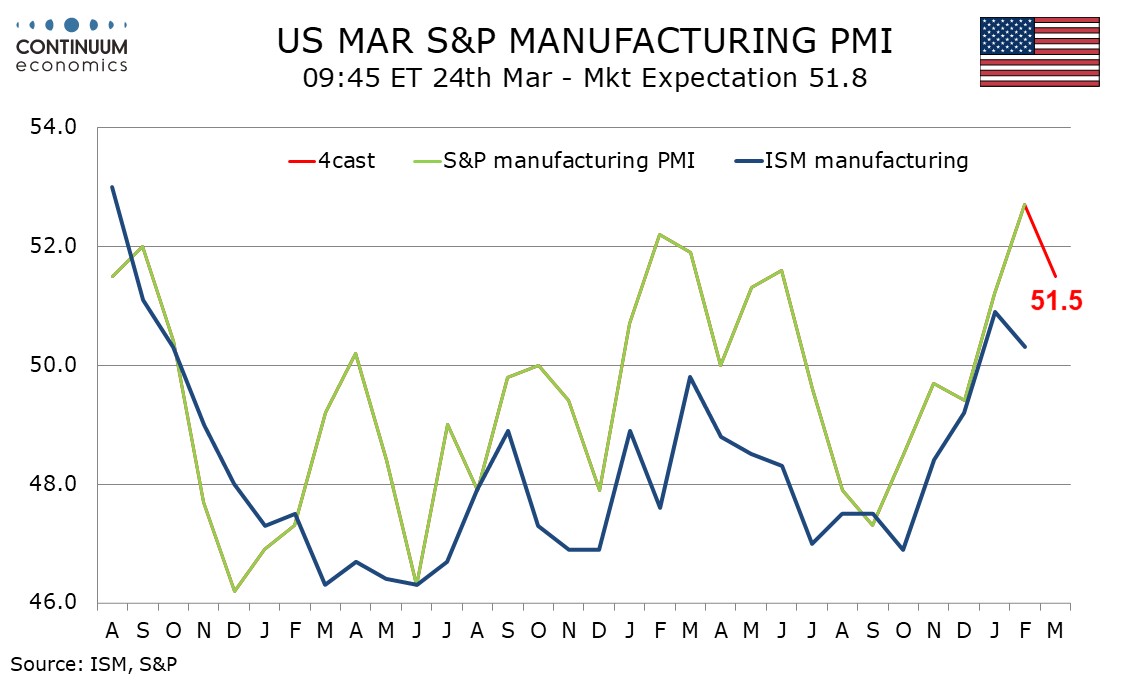

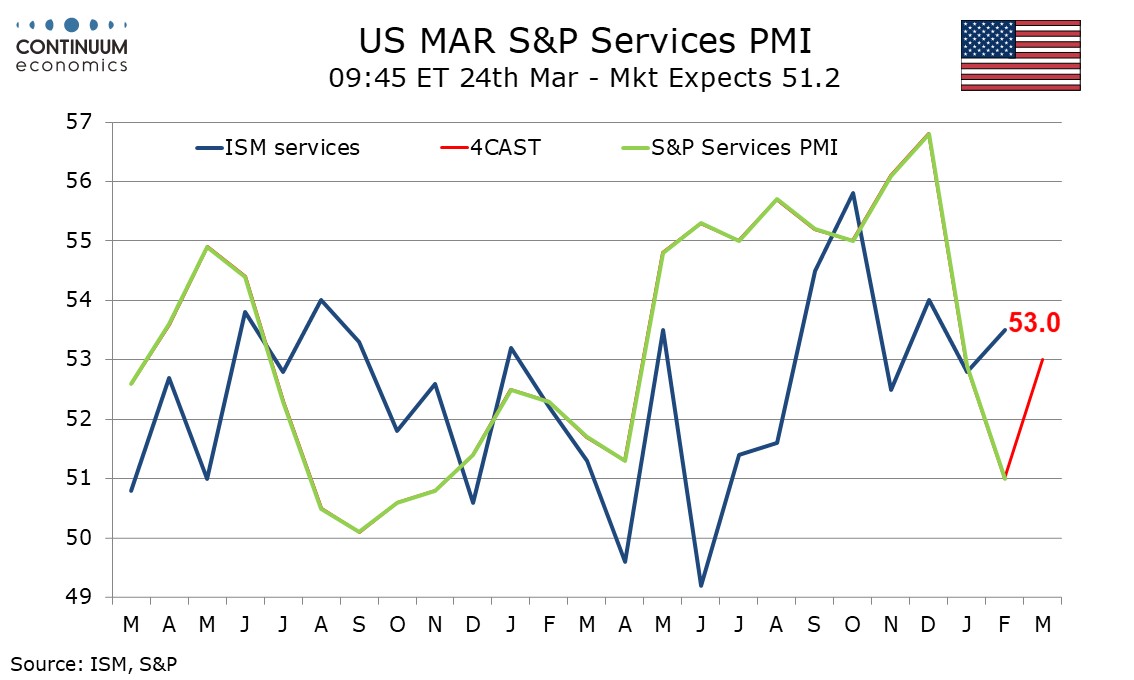

US PMI, trade and confidence data has potential for more impact than usual

GBP may be vulnerable to CPI and fiscal update

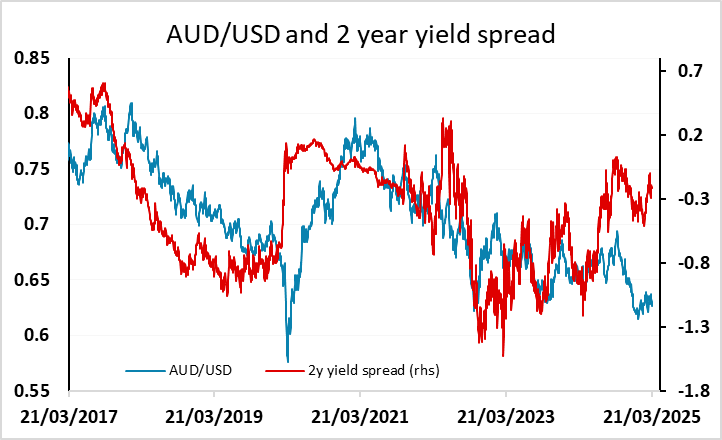

AUD tone has weakened but big picture still looks positive

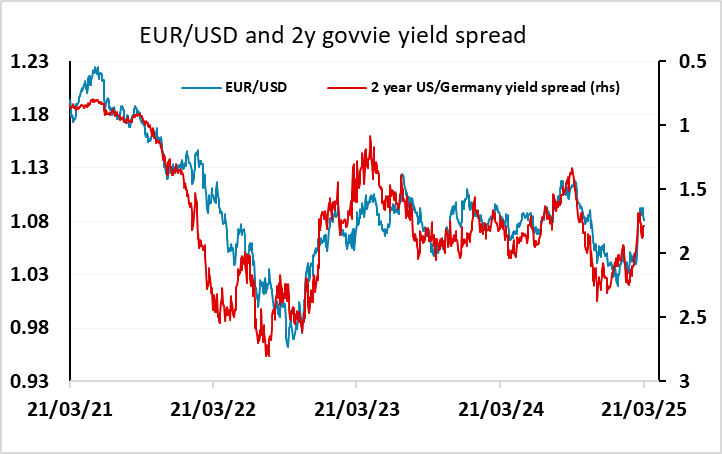

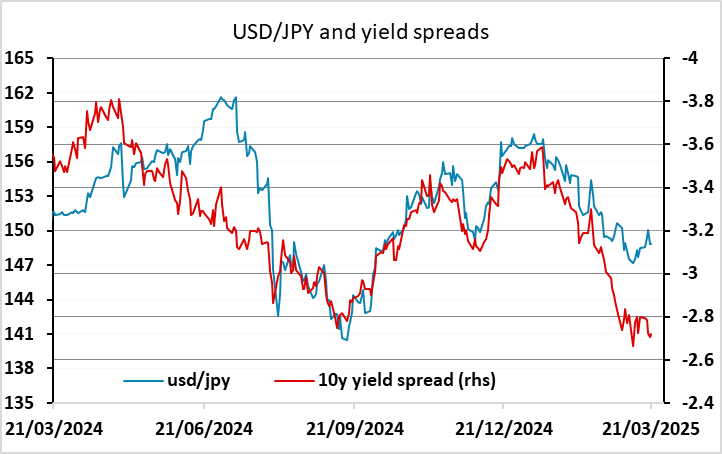

The USD stabilized last week after the losses seen in the previous couple of weeks, helped by some modest contraction in yield spreads versus the EUR and a less risk positive tone to equity markets. However, the USD recovery against the JPY was harder to justify, with no movement in yield spreads in the USD’s favour, and with risk appetite softening by the end of the week, there looks to be scope for renewed JPY gains in the coming week.

US data would normally be considered mostly second tier, but could have more impact than usual given the uncertainty around US economic prospects. The PMI data on Monday will be of interest in both the US and Europe. The US data saw a sharp drop in the services index in February and consequently in the composite index despite a strong rise in the manufacturing index. Both will likely see corrections in the opposite direction, and if so this should be modestly USD positive as the impact of a stronger services sector will dominate the composite index. The Eurozone PMIs are normally more of a focus, and there are prospects of a pick-up given the expectations of increased European government spending. This suggests a generally more positive tone which might mean some strength in the higher yielders and a weaker JPY, although as we note above, the JPY is coming from a low starting point so the JPY downside seems quite limited. Of course, while stronger numbers are our central view, there would be more sensitivity to weaker US data in particular, in which case there is likely to be a more substantial JPY move higher.

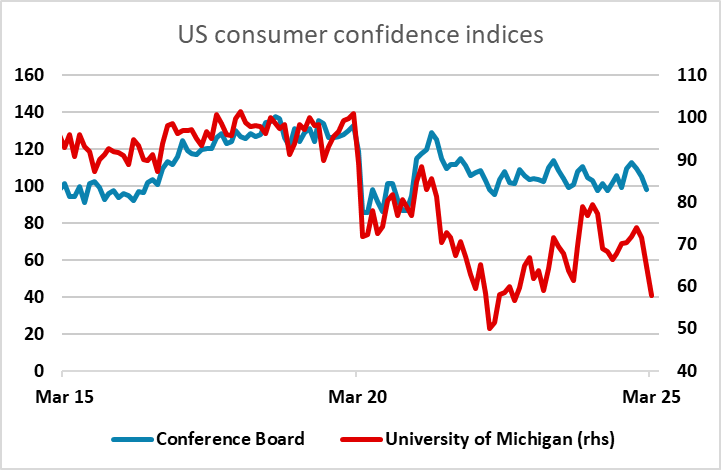

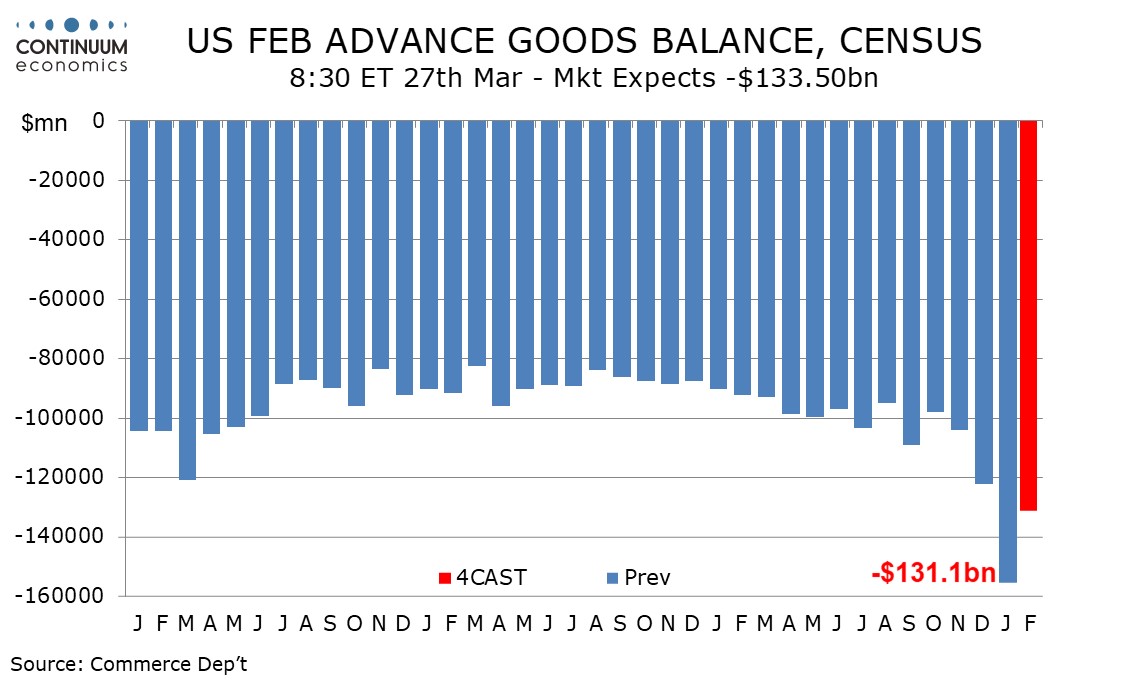

There might also be more interest than usual in the US trade data after the sharp rise in the deficit in the last couple of months. This has been doubly significant because it has strengthened expectations that the Trump tariffs will be maintained, while also significantly damaging US growth. The Atlanta Fed GDPNow nowcast is currently predicting a 1.8% annualized Q1 US GDP decline, mainly because of the big drag from trade. This is unlikely to stay so weak, as the January import surge is at least partly erratic, but an improvement in the trade numbers is required to turn the nowcast positive, so there will be more interest than usual in the trade figures. There will also be more sensitivity to the Conference Board confidence index, after the further decline in the University of Michigan preliminary March index. The Conference Board index has been much stronger in recent years, mainly because it is much more dependent on employment prospects, and with most employment indicators still solid, t seems unlikely to follow the UoM index lower despite a weaker number last month. Nevertheless, it will be closely watched. On balance, we expect the US data to calm some of the fears about the economy, and should provide modest USD support as a result, but there is likely to be greater sensitivity to weak than to strong data.

In Europe, the PMI data will be important as mentioned above, but the most interesting event could be the UK fiscal update on Wednesday. This will see updated forecasts from the OBR and likely more spending cuts to balance weaker GDP and higher debt service costs, as well as commitments to more defence spending. Recent fiscal adjustments haven’t generally been received well by the markets, with any increase in debt issuance becoming increasingly difficult for the market to absorb, especially given the huge Bank of England QT programme. The first budget of the current government saw a similar, albeit much smaller scale, reaction to the infamous Truss budget of 2022, with yields rising and GBP falling. There are once again risks in that direction with the government needing to tighten policy against a background of weaker growth forecasts. So while GBP was initially a little firmer after the BoE MPC meeting last week, the risks for GBP this week look to be on the downside, especially since we expect the CPI data on Wednesday to be on the weak side of the market consensus of 3.0%.

While there isn’t much of interest out of the Eurozone other than the PMI data this week, there will be some uncertainty related to Friday’s Norges Bank meeting. While this had been flagged for a likely rate cut at the last meeting, the subsequent strength in the CPI data has meant that the market now sees a 25bp cut as only around a 30% chance. The NOK has strengthened since the CPI data, making up some of the large amount of ground it lost through 2024, and continues to look to have potential for further substantial gains based on the relationship with yield spreads. But the rally could be stopped in its tracks if Norges Bank decide to cut in any case. We slightly favour no change in rates, and that should allow further NOK gains against both the EUR and SEK.

Japanese Tokyo CPI for March and Australian CPI for February are also both due, and have potential for market impact, although the trends in the JPY and the AUD are still likely to depend more on the general risk tone than the domestic data. The AUD sold off sharply last week after weaker employment data and some regional equity weakness, and may be vulnerable to further short term losses. Even so, we favour the upside medium term if the employment weakness proves to be a flash in the pan.

Data and events for the week ahead

USA

On Monday we expect a correction lower in March’s S and P manufacturing PMI to 51.5 from 52.7 but a correction higher in services to 53.0 from 51.0. On Tuesday January house price data from FHFA and S and P Case-Shiller are due, while April consumer confidence will be closely watched for increasing signs of weakness. We also expect a 3.5% increase in February new home sales to 680k. On Wednesday we expect February durable goods orders to be unchanged, but with a 0.5% increase ex transport. Fed’s Musalem is also due to speak.

On Thursday we expect February’s advance goods trade deficit to fall to $131.1bn from January’s import-led surge to $155.6bn, but this will remain above December’s $122.1bn, which itself was a record high until January’s data was released. Weekly initial claims are also due while we expect the third estimate of Q4 GDP to be unrevised at 2.3%. February pending home sales follow, and Fed’s Barkin will speak.

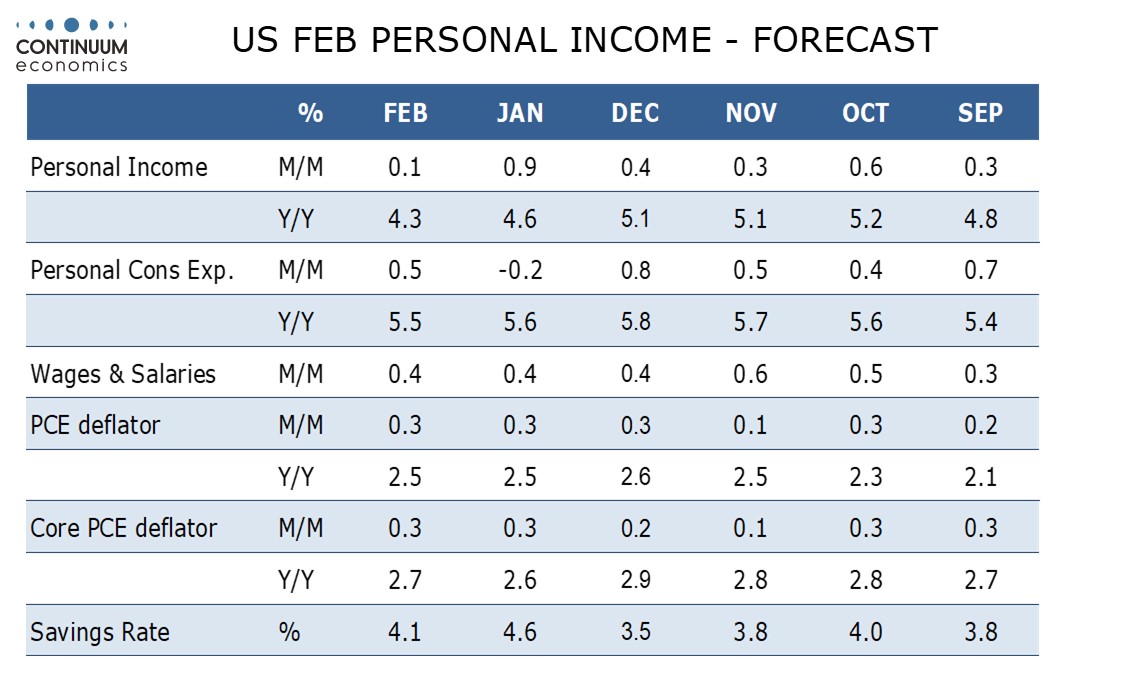

On Friday we expect a 0.3% increase in February’s core PCE price index, a little above a 0.2% core CPI. We expect personal income to rise by only 0.1% after a strong 0.9% rise in January but personal spending to rebound by 0.5% after a 0.2% drop in January. Friday also sees final March Michigan CSI data, which was weaker in the preliminary release, with inflation expectations significantly higher. Friday will also see Fed’s Bostic speak.

Canada

In Canada, Friday sees January GDP, where we expect a healthy 0.3% increase in line with a preliminary estimate made with December’s data. However the preliminary estimate for February is likely to be flat at best as tariff concerns build.

UK

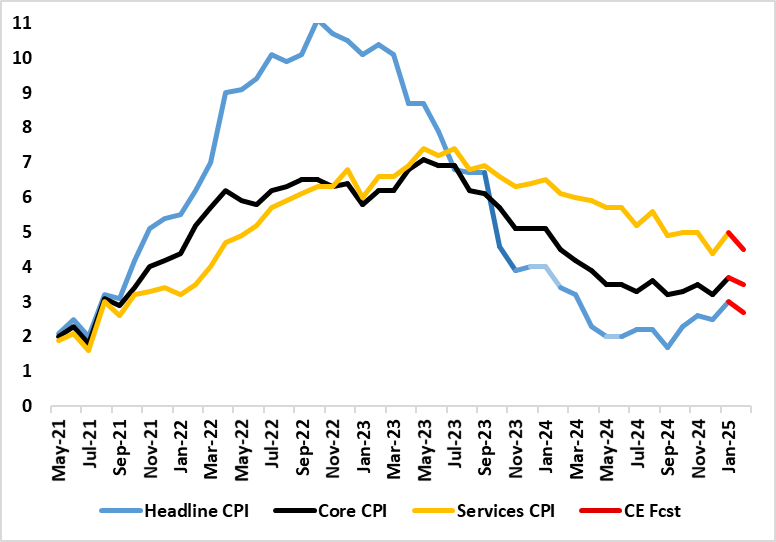

Data takes up importance alongside policy updates this week, important after the upside surprises in the last CPI. Indeed, January’s CPI numbers showed a marked bounce back up, and with the 0.5 ppt rise taking it to a 10-month high of 3.0%. We think some of this services rise is noise which will reverse in February and despite the impact of higher alcohol duties and fuel prices, then headline CPI inflation may slip back to 2.7% or a notch higher – ie the BoE projection of 2.8%. In fact, we see services inflation down 0.5 ppt to 4.5%, very much below BoE thinking, all the more important as the MPC will not have advance insight into these CPI numbers. Even so, it is unlikely to alter the split MPC’ mindset with perhaps the government fiscal update due later the day on Mar 26 more important! This fiscal event will see OBR updates, likely to show weaker GDP growth, higher debt servicing costs and (very likely) further spending cuts as well as more details on those reductions made earlier this week to the welfare bill. The question is to what extent the fiscal leeway from the new fiscal rules will have been repaired and, if so, by how much as markets may not be impressed if it still small, thereby suggesting further fiscal tightening may be need in the not too distant future.

February Inflation Slips Back?

Source: ONS, Continuum Economics

The fiscal backdrop may still be weighing on businesses as Monday’s flash PMI may show with a March outcome little changed for the composite at 50.5. On Friday, the economy will register highly in BoE Governor Baileys speech (Mon). And the weak backdrop will be confirmed by final Q4 GDP data and February Retail Sales, where a drop of over 1% is on the cards. Also Friday sees balance of payments numbers where a fresh deterioration is on the cards reversing in Q4 the improvement of the previous quarter. The UK current account deficit, when trade in precious metals is included, narrowed by £5.9 billion to £18.1 billion, or 2.5% of GDP in Quarter 3 2024

Dep Govs Lombardelli and Ramsden speak on Monday as does MPC dove Dhingra (she speaks again on Wednesday) while Chief Economist Pill appears on Tuesday.

Eurozone

Current ECB thinking, which may be highlighted by an array of Council speeches due almost every day next week) may be more moulded perhaps by the almost as large array of survey data (eg Tuesday’s IFO where a marked upgrade is surely in the offing given the large expectational component) and its own consumer expectations survey on Friday, the latter coming alongside with the European Commission numbers (also likely to show some jumpy). Monday sees flash PMI data and these too should be better, even if they do not include as much expectations over and beyond a 12-mth outlook). We see a small rise in March, after Composite PMI Output Index was unchanged at 50.2 in February. There will also be the monthly update on money and credit (Thu) for the ECB to chew over. There are also March CPI/HICP data from Spain and France (both Fri).

Rest of Western Europe

There are only some key events in Sweden, most notably the Economic Tendency Survey (Wed), which has got less bad of late as have GDP indicator numbers and where more Riksbank insight is due the same day with Board meeting minutes due. In Switzerland, there is the KOF survey (Wed), likely to remain sub-par).

Norway sees the widely awaited Norges Bank decision where recent inflation data have questioned whether the well flagged rate cut will now be delivered – we think the decision may be more finely balanced that many are suggesting not least as economic activity signs are mixed even with the regional survey having improved. But inflation remains has moved further above target, but has been boosted by a series of one-offs. The question is whether the (hawkish) Norges Bank judge price pressures appear to be more persistent than it previously assumed. Regardless, a significant reassessment, possibly including a deferment of the planned rate cut next week. As suggested the odds may be nearer balanced, but under any scenario, the rate path will be revised significantly higher

Japan

Tokyo CPI on Friday continues to be the highlight for the Japanese calendar next week. February CPI has shown moderation but remain very hot and we are only seeing a mild moderation. It would be a surprise to see any upside beat and could see the BoJ to hike earlier than market currently expects. Else, PMIs on Monday will not be as eye catching as service index on Wednesday, which could tell wage momentum.

Australia

We have monthly CPI on Wednesday. It is forecast to be within target range but unlikely to surprise much. The RBA is likely to take it slow in easing wage growth has not been picking up even with a very tight job market. We also have PMIs on Monday.

NZ

Only consumer confidence on Friday.