Norges Bank Preview (Mar 27): No Change but a Close Call?

Norway sees the widely awaited Norges Bank decision later this month where recent inflation data have questioned whether the well flagged rate cut will now be delivered – we think the decision may be more finely balances that many are suggesting not least as economic activity signs are mixed even with the regional survey having improved. But if pressed see no move at this juncture. Clearly, inflation has moved further above target (see above), but has been boosted by a series of one-offs and also by the CPI basket re-weighting. The question is whether the (hawkish) Norges Bank judge price pressures appear to be more persistent than it previously assumed. Regardless, a significant reassessment, including a deferment of the planned rate cut next week. As suggested the odds may be nearer balanced. Regardless, under any scenario, the rate path will be revised significantly higher. But we see the Norges Bank deferring the move, the question how much

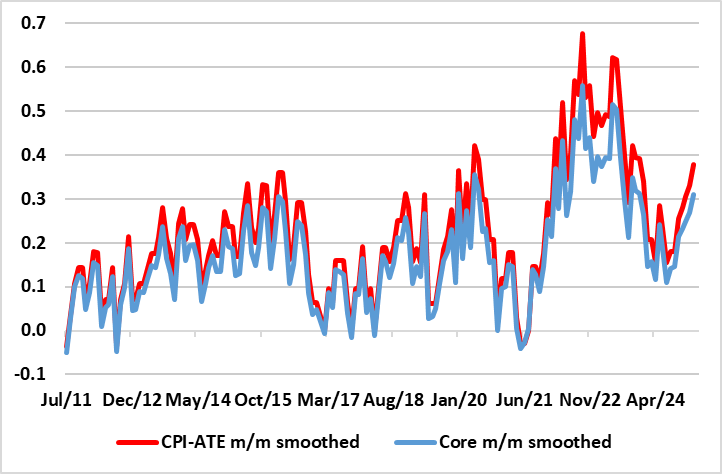

Figure 1: Higher Short-term Price Pressures Led by Food Surge not Included in Core Measure

Source: Stats Norway, CE, smoothed = 3 mth mov avg

As for the outlook beyond, the Norges Bank also worries about business costs, but has noted two-sided risks around it, encompassing the risk of an increase in international trade barriers but with less overt concern about the weak currency this time around. The worry is that higher tariffs will likely dampen global growth, but the implications for price prospects in Norway are uncertain. We still see some 100 bp of rate cuts in 2025 – ie likely to be more than 50 bp greater than the Norges Bank may be advertising in its looming policy assessment and at least the same amount of cuts in 2026!

Obviously, inflation has surprised markedly on the upside of late, albeit mainly food and energy but also due to CPI basket re-weighting, all creating possible marked downward base effects for early 2026. And short-term dynamics are not nearly as worrying, especially in a core measure that excludes the food component dominating the chosen policy measure of CPI-ATE. But as we have noted before inflation is bolstered by 4%-plus annual rental increases (19% of the CPI) which we think are policy pro-cyclical. Indeed, ex-rent inflation is has jumped too, this will slow in due course which makes our forecast of 2% inflation both next year more likely, albeit after an upwardly revised (by 0.7 ppt) to2.7%. But much

Supporting this disinflation story, the productivity picture makes it more likely that an output gap may already have appeared and one that could enlarge through 2025 and persist in 2026. Admittedly, this may be inconsistent with a second successive year of negative fixed investment, and one that extends beyond weak construction, the latter very much likely to extend though the coming year. But in contrast to what we think is optimistic consensus thinking on household spending, we do not see any faster recovery than in 2024 and only modest growth next year broadly chiming with GDP. This is especially as the recent rise in house prices is fragile and unemployment is starting to rise although the jobless rate may just exceed 4% in 2025 and then stay there through 2026.