FX Daily Strategy: Asia, March 12th

Rather Quiet Calendar Sees Headline Dominates

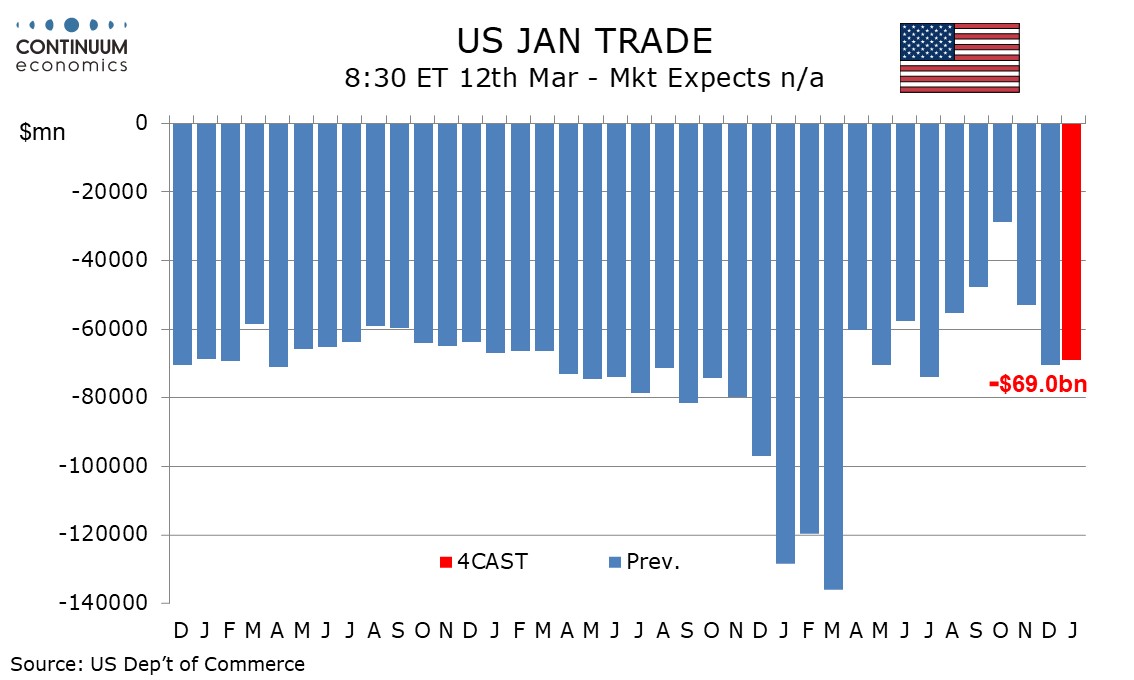

U.S. January Trade Balance May be stabilizing

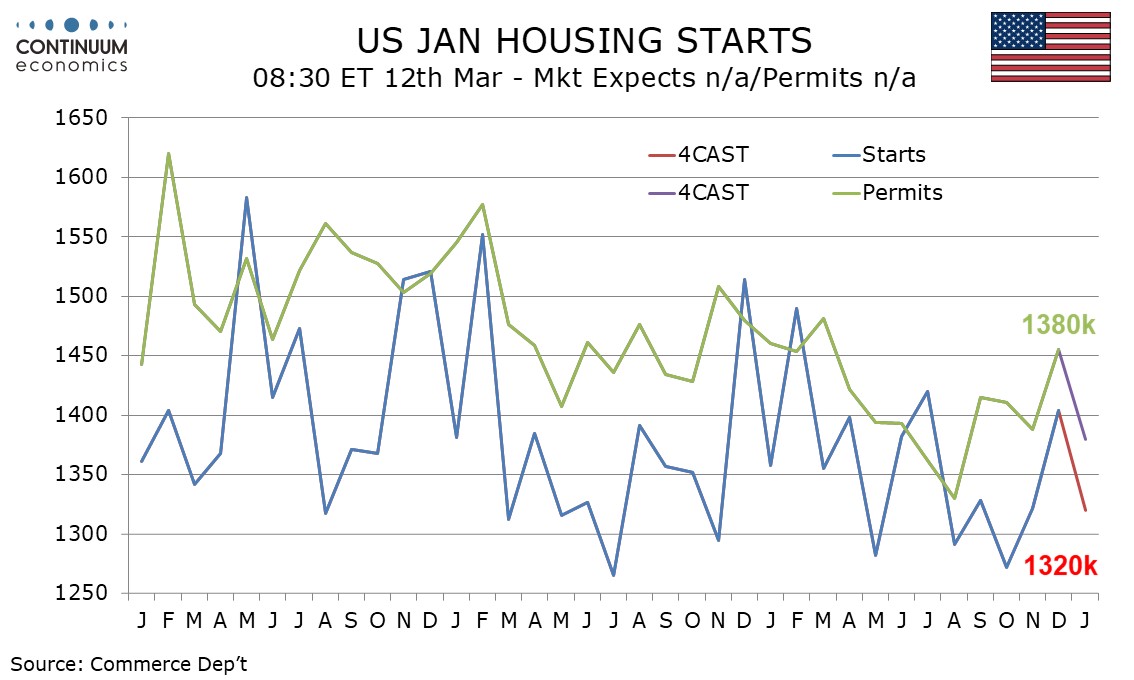

U.S. January Housing Starts and Permits Weaker

The economic calendar is rather empty on Thursday. It means major volatility will likely come from headlines, especially in the U.S.-Iran front. The market sentiment has turned calm and may see further improvement if oil tanks begin to pass Strait of Hormuz or Trump announcing the military operation is over. It could lead to lower oil and USD (haven bids fade) and higher equities.

On the chart, the test of resistance at 99.50 has given way to selling interest, as intraday studies turn down, with the break below 99.00 putting focus on congestion support at 98.50. Overbought daily stochastics are turning down, unwinding negative divergence, and the positive daily Tension Indicator is also coming under pressure, highlighting room for a break below 98.50 towards further congestion around 98.00. Broader weekly charts continue to rise, however, suggesting any initial tests of here could give way to consolidation. Meanwhile, a close back above congestion resistance at 99.00 would help to stabilise price action and give way to consolidation beneath strong resistance within the 99.50 - 99.68/70 range.

We expect a January trade deficit of $69.0bn, which would be only a marginal correction from December’s $70.3bn which was the widest since July, though still well below the record $136.0bn deficit seen in March of 2025 shortly before the tariff announcement. Despite the huge volatility in monthly trade data caused by policy changes, the average monthly deficit in 2025 of $75.1bn was almost exactly the same as that for 2024 at $75.3bn. December’s trade deficit may represent a return to normalization, implying little change in January should be expected. Goods exports surged in September and October largely on strength in nonmonetary gold but have since corrected back. Nonmonetary gold exports are still probably marginally above likely long-term levels but we expect a modest 1.0% in January goods exports, more on prices than volumes. Goods imports have also been volatile, plunging in October led by pharmaceutical preparations which are still quite weak and have some upside scope. However imports of computers have recently been very strong but are showing signs of peaking. We expect goods imports to rise by a modest 0.5% in January, with little contribution from prices.

We expect January housing starts to fall by 6.0% to 1.32m to follow a 6.0% December increase while permits fall by 5.2% to 1.38m to follow a 4.8% December increase. Underlying slowing in demand and bad weather are both likely to contribute to the decline, with the latter impacting starts more than permits. We expect starts to show singles down by 4.2% after a 4.1% December increase while multiples fall by 10.2% after an 11.3% December increase. For permits we expect a 1.2% drop in singles to extend a fall of 1.7% in December, while multiples fall by 10.1% after a 15.2% December increase. Housing demand does appear to be slowing as signaled by softer January data from the NAHB and MBA surveys, as well as slippage in existing and pending home sales for January. Fading hopes for further Fed easing may be weighing on demand.