FX Daily Strategy: N America, May 15th

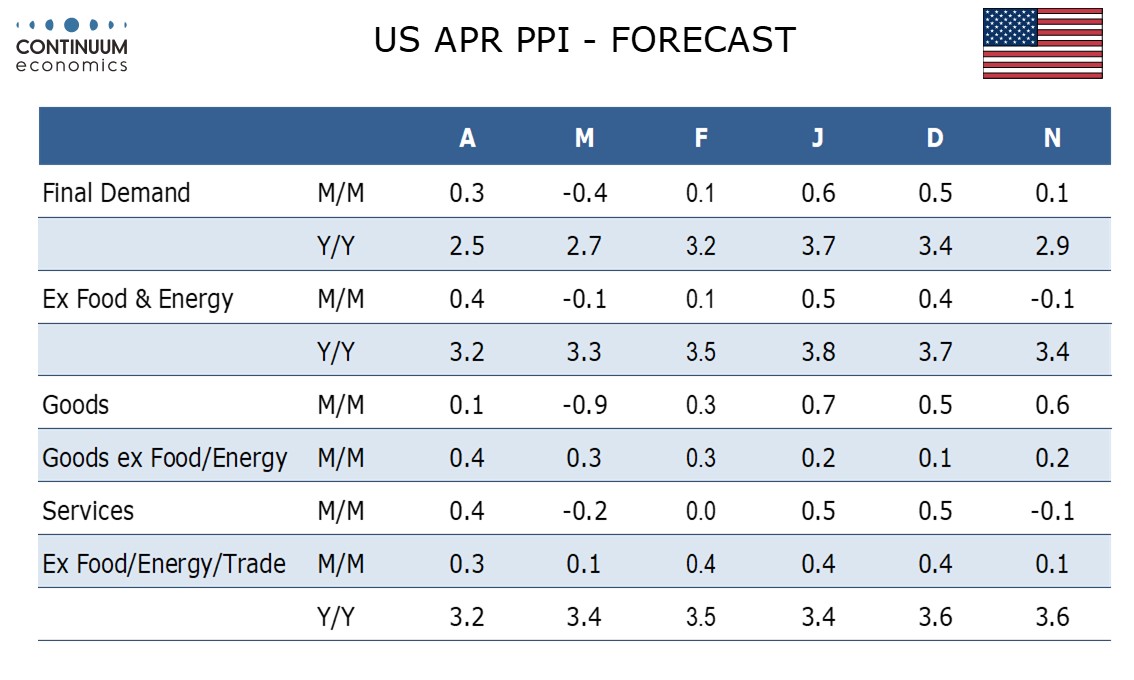

US PPI and survey data may be USD supportive

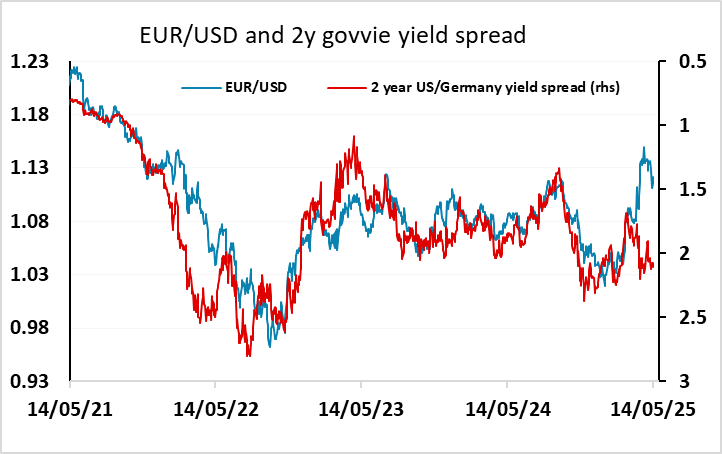

EUR/USD more rangy but risks on the downside

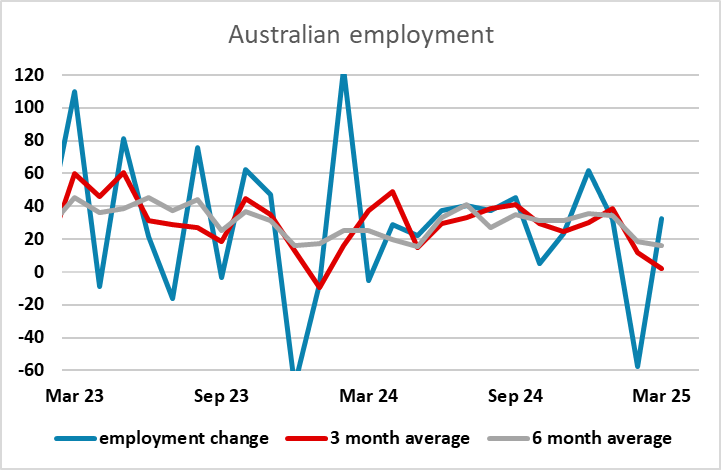

AUD could benefit from solid employment data

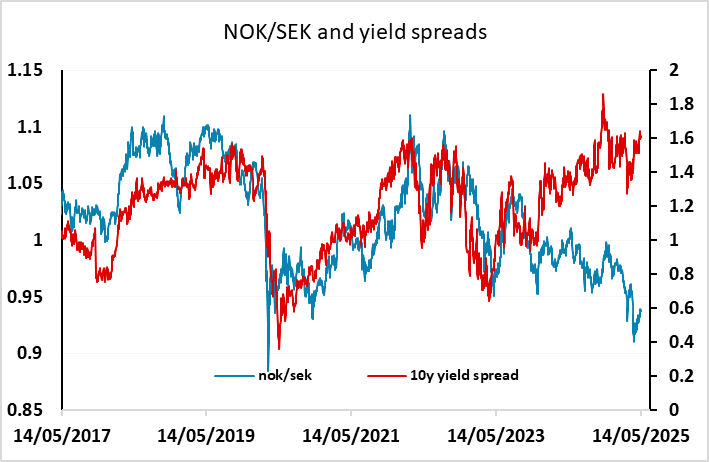

NOK still has scope for recovery after strong GDP

US PPI and survey data may be USD supportive

EUR/USD more rangy but risks on the downside

AUD could benefit from solid employment data

NOK still has scope for recovery after strong GDP

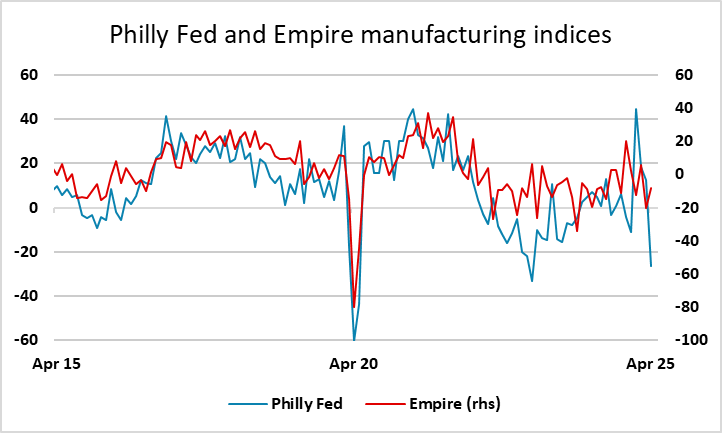

In the US, there is an array of data that might normally be considered second tier but will be seen as potentially significant given the uncertainty about the current state of the economy. We expect April PPI to bounce from a weak March with a 0.3% rise overall and a 0.4% increase ex food and energy. Ex food, energy and trade, we expect a rise of 0.3%. Tariffs are likely to continue supporting goods prices while services are likely to correct from a weak March. Our forecasts are a tad above the market consensus, and may provide some support for the USD. However, this will depend on how the other data come out, with jobless claims and the Philly Fed and Empire manufacturing surveys also due. The Philly Fed showed a sharp dip in April and a recovery in May could be USD supportive if jobless claims continue to show no evidence of weakness.

The softer USD on Wednesday made some sense in that the recovery on the back of the US/China deal was somewhat overdone, given that there is still likely to be a significant negative economic impact from the tariffs that remain. But at this stage it seems unlikely that the effect will be sufficient to trigger a recession, so we would expect EUR/USD to settle into a 1.11-1.13 range. If anything, the risks should be on the downside as EUR/USD remains well above the level consistent with the previous yield spread relationships, whereas the AUD still looks cheap on that basis and the JPY no better than fair.

The April Australian labor data has come in significantly stronger than expected. Not only headline employment change is a beat of +89k, the participation rate of 67.1% is historic high with no change to unemployment rate of 4.1%. The market is still near enough fully pricing a rate cut at next week’s RBA meeting, and it would now take a lot to prevent a cut, but there is scopefor a decline in future rate cut expectations. This would put the AUD risks on the upside, and given the recent strong performance of equity markets and the risk positive bias in the AUD there may in any case be some potential for further AUD gains. 0.64 in any case looks to be a solid base for AUD/USD and shouldn’t be threatened unless we see renewed sharp weakness in regional equities.

UK Q1 GDP has been revised up to 0.7% q/q from the 0.6% originally reported, with particular strength in business investment, up 5.9% q/q and 8.1% y/y. GBP initially rose slightly on the news, but has levelled off and EUR/GBP remains steady at 0.8430/35. The investment numbers will, however, be encouraging from a longer term growth perspective, as weak investment in the UK has often been cited as a reason for relatively weak growth. But increases in capacity will tend to reduce inflationary pressure longer term, so might allow more rate cuts longer term. The data is thus fairly neutral for GBP, and EUR/GBP is likely to remain well supported near 0.84.

Norwegian GDP has also come in stronger than expected, with the mainland measure up 1.0% q/q in Q1. EUR/NOK is nevertheless not much changed near 11.63, but NOK/SEK has pushed up around 20 pips to 0.9380. We continue to see plenty of upside scope for NOK/SEK, with yield spreads remaining favourable and the Norwegian economy solid.