FX Weekly Strategy: December 1st-5th

Risky currencies may struggle to rise further with S&P 500 approaching the highs

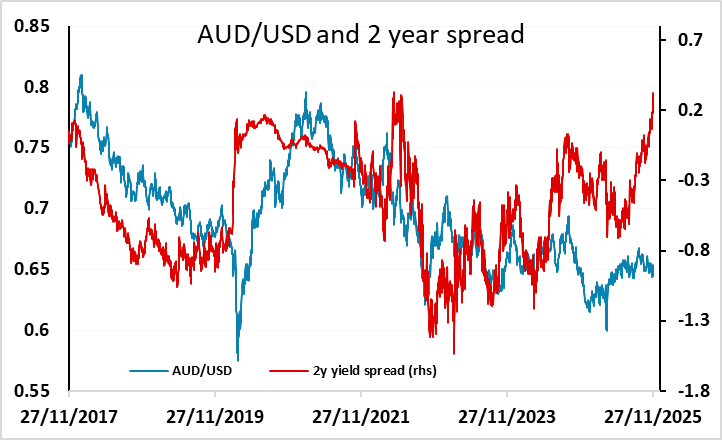

AUD still look good value relative to yield spreads

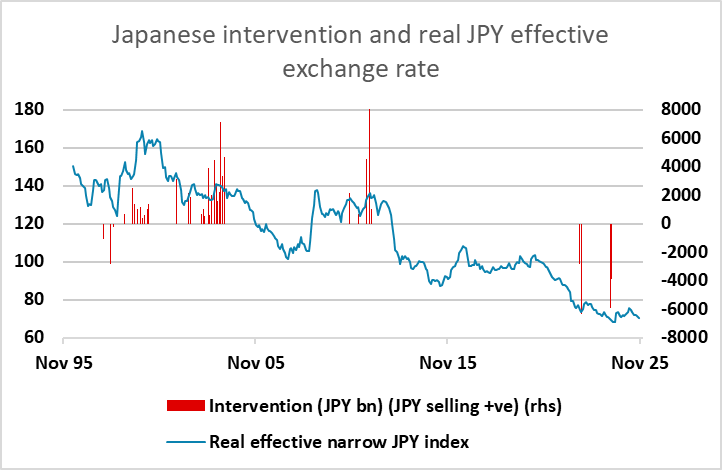

JPY could benefit from Ueda speech, and downside should be protected by intervention

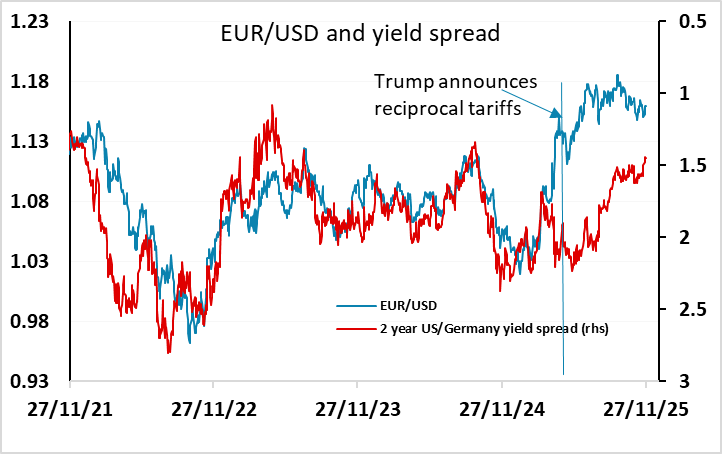

GBP and EUR both look vulnerable

Strategy for the week ahead

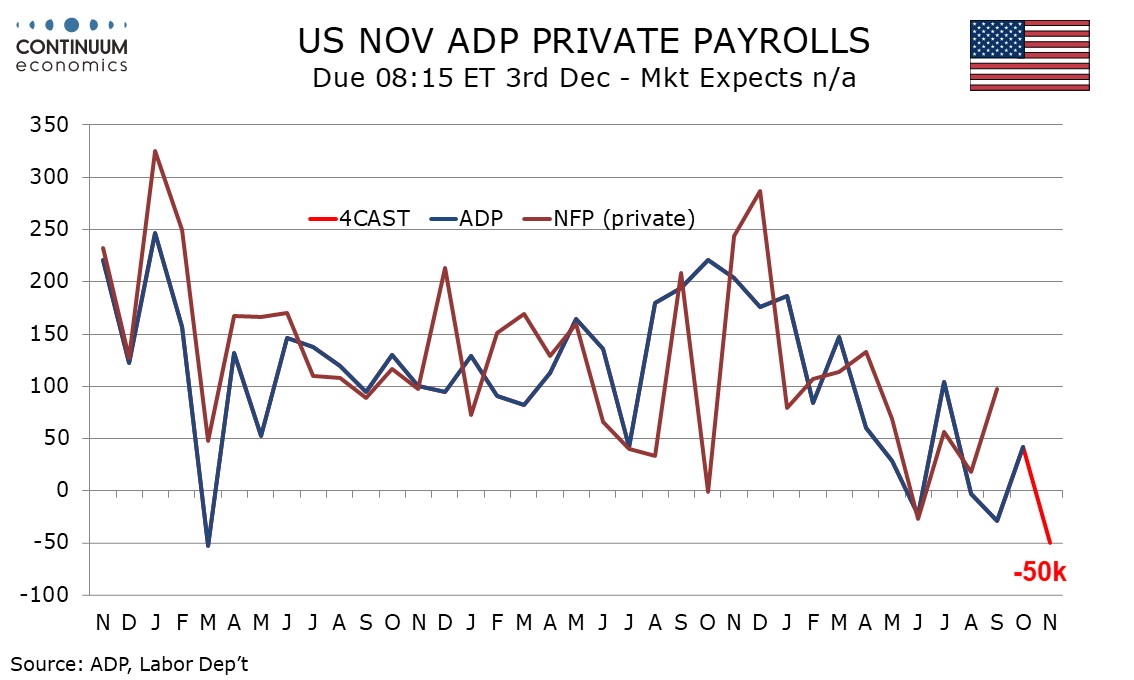

Once again, much will depend on equity market performance. The S&P500 rose every day last week and is back to less than 100 points off its high. This helped the riskier currencies on the week, with the AUD, CAD and NZD all doing well, although NZD gains had a lot to do with the RBNZ’s less dovish stance. Coming into the new week, the case for more equity gains is harder to make so close to the highs, but a new high is certainly possible if the market were to, for instance, fully price in a December Fed rate cut, as long as that move wasn’t based on a significant downgrade in growth/earnings expectations. This week’s ADP employment report for November could be significant in that regard. We look for a decline on the month based on the weekly ADP data, and while that would likely mean the market did come close to fully pricing in a Fed rate cut, it may not be seen as a positive growth signal.

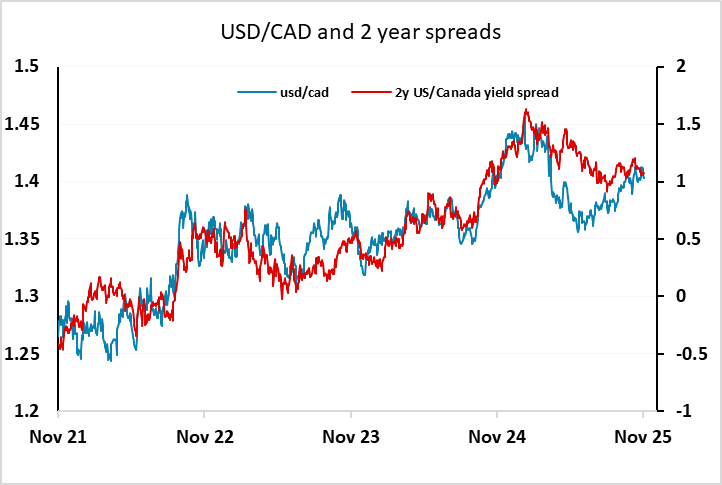

Nevertheless, we still see upside for the AUD in particular, which continues to look very attractive on a yield spread basis and once again has bounced strongly from a dip into the 0.64s. This week’s Australian Q3 GDP data may well come in on the strong side and support further gains towards the top of the year’s range. Upside for the CAD looks less substantial after the strong rally on Friday following the Q3 GDP data, as we expect tis Friday’s employment report to show some weakness after strength in recent months, and there is little scope for any further rise in CAD yields with no further rate hike priced in.

For the JPY, life may well be difficult unless we see some turn lower in equities. However, BoJ governor Ueda is due to speak on Monday and may encourage recent rising expectations of a December BoJ rate hike. While this seems increasingly likely because of the weakness of the JPY and the persistence of inflation well above 2%, and some more hawkish comments from other board members of late, it is still only 33% priced in the market, so there should be potential for a significant JPY boost if Ueda signals a willingness to hike. At the same time, there is also room for disappointment, but we expect the Japanese authorities to intervene if the JPY moves to new lows after the recent strong warning from Katayama, so we see JPY risks as biased to the upside.

In Europe we have preliminary HICP data for the Eurozone for November, but with the French, German and Spanish data already released we wouldn’t expect any significant surprises. The EUR showed a little softness early on Friday but this was largely reversed by the end of the day, helped by the German HICP data coming in stronger than the state data suggested. The national CPI measure was much weaker. Nevertheless, we still see scope for further ECB easing in the coming months as lending surveys show weakness and CPI still look more likely to fall than rise. The EUR also continues to be stretched relative to yield spreads against most of the other majors.

GBP performed well after the Budget last week, but we are a wary of the positive response as the positive Budget surprises all came because of better OBR tax take forecasts rather than attractive Budget measures. Forecasts can always change, and the measures themselves didn’t look favourable for the longer term health of the economy or public finances, involving significant increases in spending and taxes. We expect sentiment to turn more negative on GBP, but for now EUR/GBP will likely hold below 0.88.

Data and events for the week ahead

USA

Monday sees November’s ISM manufacturing index, where we expect a modest increase to 49.0 from 48.7, while Wednesday sees November’s ISM services index, where we expect a modest slowing to 52.0 from 52.4. More significant on Wednesday may be the ADP employment report for November, where weekly ADP data suggests a decline, we expect of 50k. Wednesday also sees September industrial production, where we expect gains of 0.1% both overall and in manufacturing. Thursday sees weekly initial claims, while the November layoffs report from Challenger, Gray and Christmas may get some attention after a spike in October caused some alarm. On Friday we expect a 0.2% increase in September’s core PCE price index, with a 0.2% rise in personal income and a 0.3% increase in personal spending. The preliminary December Michigan CSI follows.

Canada

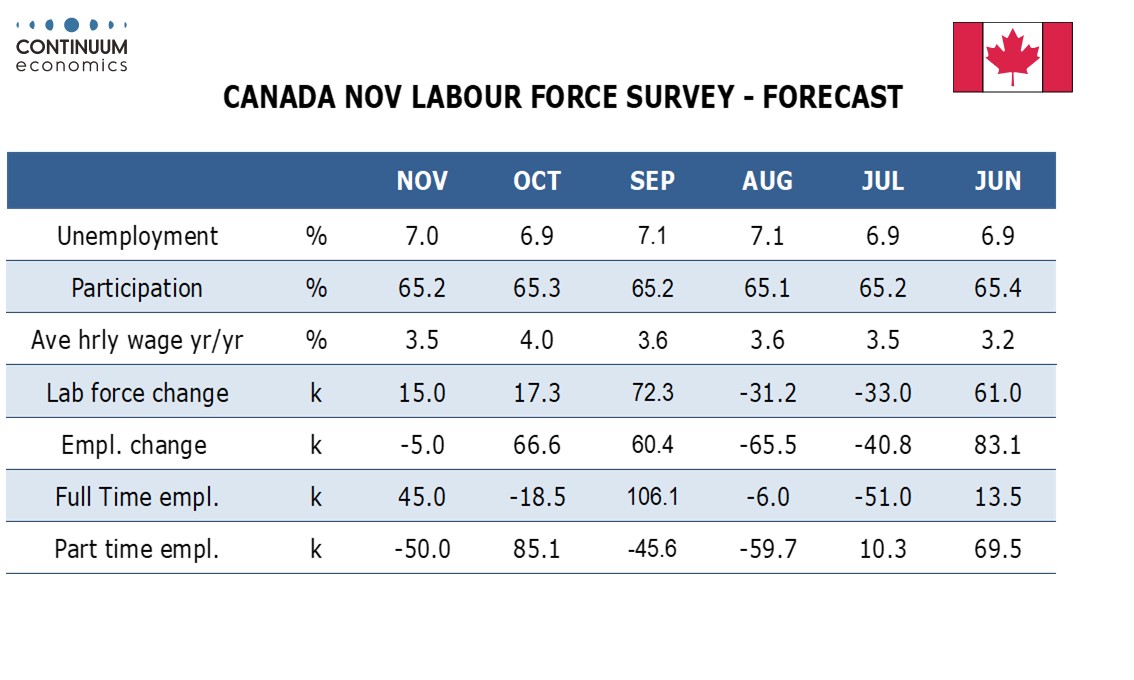

Canada’s data highlight is November employment on Friday, where we expect a decline of 5k after two straight strong gains with a rise in unemployment to 7.0% from 6.9%. November PMIs are also due, the S and P manufacturing index on Monday, the S and P services index on Wednesday and the Ivey manufacturing index on Thursday. Q3 productivity is due on Wednesday. Thursday’s October trade data has been postponed due to the continuing absence on inputs from the United States.

UK

The week sees more BoE insight with MPC speeches (Mon, Wed), these coming ahead of more BoE survey data on Thursday useful for gauging the labor market (DMP). There is also the BoE money and credit data (Mon) where housing market volatility and distortions may again be the order of the day but with further signs of an underlying weakening. Otherwise, no appreciable revisions are expected in final PMI numbers (Mon, Wed) but perhaps with more interest into the first insight for the month into the Construction PMI (Thu).

Eurozone

Several albeit less important updates are due this week, the question for Germany being the extent to which Friday’s industrial orders show fresh weakness. As for survey data, no appreciable revisions are expected in final PMI numbers (Mon, Wed) but perhaps with more interest into the first insight into the Construction PMI (Thu). EZ PPI numbers (Wed) should show more soft cost pressures while EZ retail sales (Thu) should continue to move sideways. There is also the first full breakdown to Q3 GDP numbers (Fri).

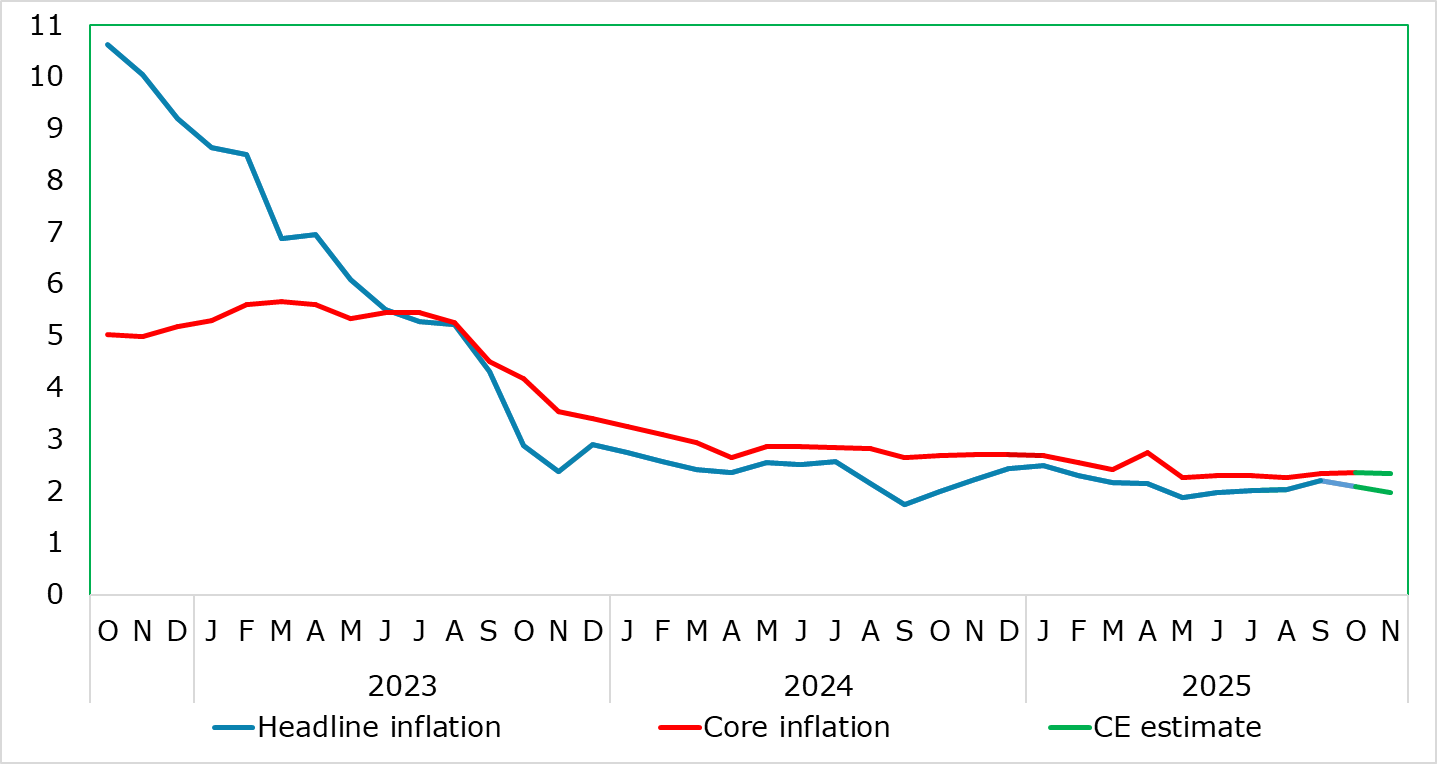

Headline CPI Moves Back To Target as Services Edge Back Down

Source: Eurostat, CE, % chg y/y

But the key data arrive on Tuesday. The HICP inflation picture has clouded somewhat of late to some. With what were previously unfavourable energy-related base effects reversing, EZ inflation edged down 0.1 ppt to 2.1% in October, largely in line with consensus thinking, but with the main core rate stable at 2.4%. The latter reflected a slight pick-up in services. However, we see this reversing and despite some m/m fuel rises, we see the headline down to 2.0% in the November flash and the core down similarly but to 2.3%. The HICP numbers will come alongside labor market data likely to show more signs if a rising workforce but also increasing unemployment! ECB insight will come from several appearances from Chief Economist Lane (Wed, Thu, Fri)

Rest of Western Europe

There are a key events in Sweden, most notably flash November CPI data (Thu) where a clear fall in the y/y rates is likely for both CPIF (to below 3%?) and the ex-energy counterpart, these coming after food prices bolstered the October numbers. Swiss CPI data are also due and where the headline y/y may drop back to zero.

Japan

Overall household spending will likely be the most important release for Japan on Friday, over a slate of tier two data. Household spending has shown signs of positive growth but its momentum is so far moderate. With real wage being negative, it will be a good sign to see if spending stays in positive territory. Other than that, Ueda’s speech on Monday may also be critical if he is willing to cue for rate changes in the December meeting. There has been reinforcement in the BoJ’s rhetoric lately and this speech could cement market expectation.

Australia

The Q3 GDP will be released on Wednesday and should continue to see modest growth. There could be some hawkish surprise as domestic demand seems to be strong in Q3. We also have trade balance on Thursday and expecting solid surplus. Apart from private inflation survey on Monday, it is all tier two data throughout the week.

NZ

No market moving data for NZ next week.