FX Weekly Strategy: May 11th-15th

Positive risk tone suggests good news largely priced in

JPY may have scope to gain on the crosses

CAD weakness can extend

GBP likely toppy against the EUR

Strategy for the week ahead

Despite the renewed skirmishing between the US and Iran at the end of the week, the S&P 500 managed to make a new all time high on Friday, helped by the solid US employment report and slightly lower yields. This suggests to us that markets are vulnerable to any bad news from the Gulf, specifically an Iranian rejection of the US peace deal, as some positive outcome looks to be being priced in judging by the price action in oil and equities. Admittedly, it is hard to see why Iran would reject the deal as it commits them to very little. Negotiations on keeping the Straits of Hormuz open and the Iranian nuclear program would only start once the deal is agreed, and this is no doubt why the market has taken a positive view for now. There is therefore very little upside for risk sentiment if the deal is agreed and plenty of downside if it isn’t, so we would tend to favour positioning for a negative outcome, even though this is not the central view.

From an FX perspective, the USD would likely benefit if there is a negative outcome, with risky currencies most vulnerable. The JPY may now offer the best optionality, as the BoJ is limiting the JPY downside against the USD. The JPY continues to be very undervalued across the board, but it is particularly difficult to see the case for JPY weakness on the crosses, given the underwhelming growth picture in Europe. From a risk perspective, JPY weakness on the crosses has tended to correlate with declining US equity risk premia for the last 10 years, but JPY weakness extended after the Japanese election last August despite a broadly steady risk picture. With there now being much less expectation of major fiscal changes from the Japanese government, there is a case for the JPY to return to its previous relationships, suggesting scope for EUR/JPY to move sub-170 and GBP/JPY to move sub-200. However, a risk negative trigger is likely to be necessary for such moves to occur.

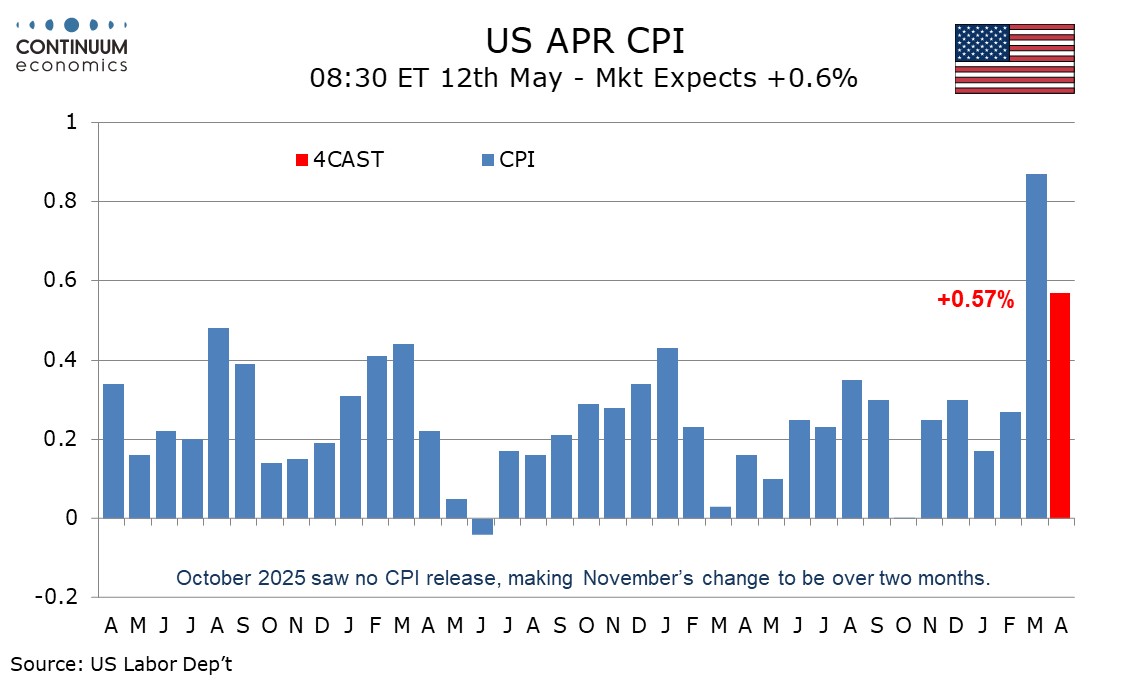

Datawise, US CPI is the main release this week. Our forecast of 0.6% headline and 0.4% core is in line with consensus, so is unlikely to impact market expectations of Fed policy. This isn’t the main driver of the USD at the moment, but other things equal, the market expectation of tightening in Europe and Japan and a flat Fed picture suggests some USD downside in neutral conditions.

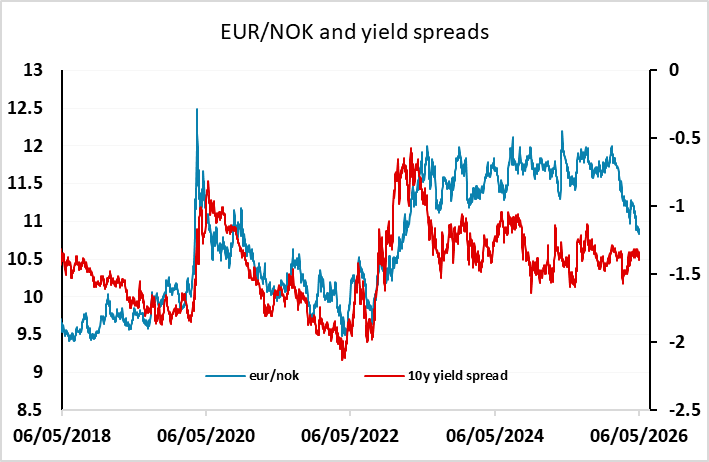

The weakness of the CAD on Friday after the weak Canadian employment report could extend this week, especially if we see some more negative risk sentiment. However, the CAD will tend to benefit if there is any recovery in the oil price. CAD bears may therefore favour short CAD/NOK positions to prevent any impact from oil price surprises. The NOK has benefited more from any oil price rises in recent months, and the Norges Bank rate hike last week gave it a further boost. There is still plenty of scope for NOK appreciation against the EUR to realign with its historic yield spread relationship after a couple of years of weakness.

GBP was not much changed on Friday after the UK local election results, which saw big losses for the ruling Labour Party, primarily to the right wing populist Reform party. That GBP was not much changed reflected the fact that the losses, while large, were if anything slightly less than expected, and also that the losses were primarily to Reform rather than the Greens. This may reduce the chances that PM Starmer is replaced, as the alternative leaders are all to his left, and the pressure on Labour, judging by the election results, is more to deal with the pressure from the right. Even so, EUR/GBP looks likely to struggle to break below the year’s lows near 0.86 in these conditions, especially as the March GDP data due this week can be expected to show a significant decline after the sharp rise in February.

Data and events for the week ahead

USA

On Monday we expect a modest 2.0% increase in April existing home sales to 4.06m to follow a 3.6% decline in March. Tuesday sees the week’s key release, April CPI, which we expect to rise by 0.6% overall with a 0.4% increase ex food and energy, the latter lifted by energy feed through to air fares and a one-time distortion in housing. Also due on Tuesday are April’s NFIB survey of small business optimism and April’s budget, while Fed’s Williams and Goolsbee will speak. On Wednesday we expect April PPI to rise by 0.5%, 0.3% ex food and energy, while Fed’s Collins, Kashkari and Logan will speak.

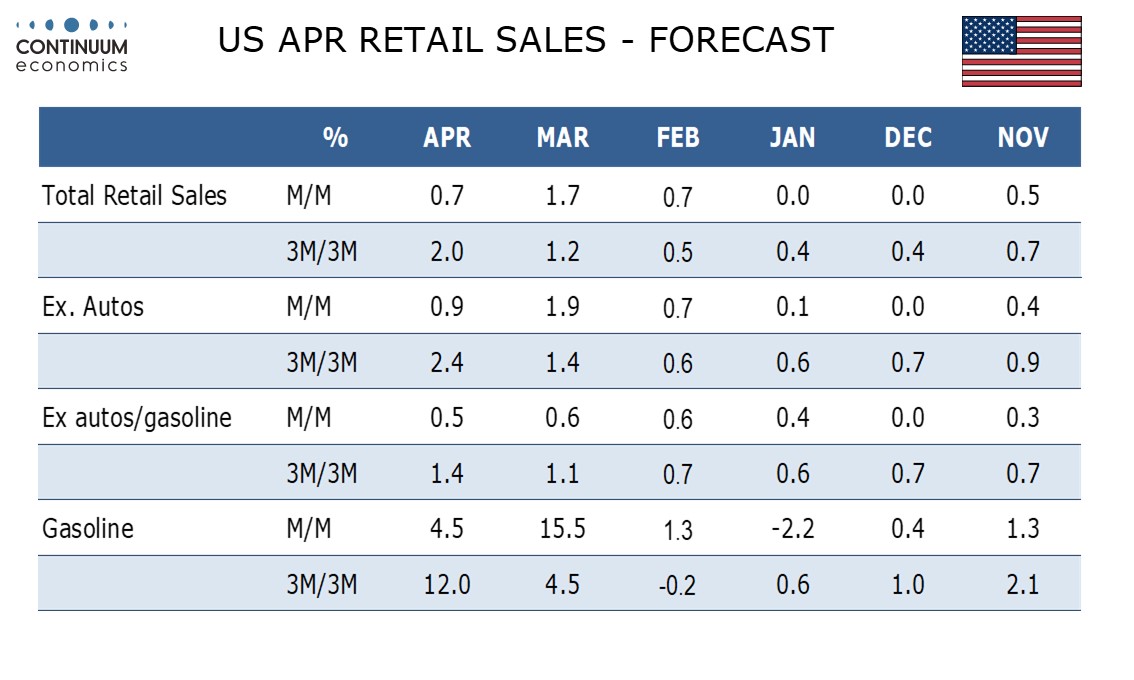

On Thursday we expect April retail sales to rise by 0.7% overall, 0.9% ex autos and 0.5% ex autos and gasoline, still showing some resilience from consumers. Weekly initial claims, which have recently been very low, and April import prices are also due, with March business inventories following. Fed’s Hammack and Williams are due to speak. Friday sees May’s Empire State manufacturing survey and April industrial production.

Canada

In Canada April existing home sales are due on Thursday and April housing starts on Friday. March wholesale sales are due on Thursday with March manufacturing shipments following on Friday. Preliminary estimates were for respective gains of 1.3% and 3.5%, with prices likely to be a factor in the gains.

UK

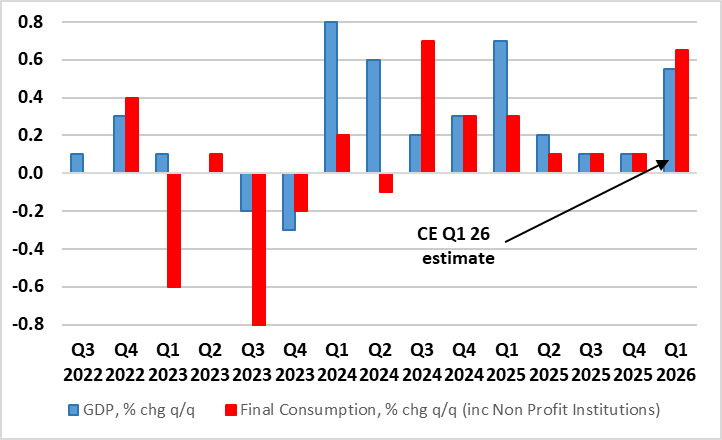

After the likely drubbing in the May local elections, the Labour government is unlikely to find much support from the King’s Speech which opens the next parliamentary session on Wednesday. The same day sees MPC member Mann speak, she likely to underscore her ‘activist’ credentials. Although a little more important as it now reaches to covers war numbers, March and Q1 GDP data arrive on Thursday, alongside production and trade figures. After the much stronger than expected February GDP update, which showed a m/m rise of 0.5%, we expect to see some correction of 0.2%-0.3% in the March update even with further warm weather, consumers hoarding and the impact of the early Easter.

Figure 1: Despite Likely Q1 Jump, GDP Growth Hardly Strong and With Increasing Downside Risks Ahead?

Source: ONS, CE

But the question is whether any such a drop is merely a correction to the February upside surprise or heralds a much weaker trend in the aftermath of the surge in energy costs and related added uncertainty. In this regard, we tend to the latter and see a fresh q/q dip in the current quarter after a 0.5%-0.6% Q1 result. Thursday (evening) also sees what are likely to be more soft housing market data from RICS.

Eurozone

Data wise sees EZ industrial production numbers data (Wed) likely to see a second successive rise and this coming in the first month of the conflict, but he data may merely reflect caution-induced inventory building. Updates but still detail-free for Q1 GDP and employment data arrive on Wednesday. ECB wide there are several speakers most notable being Lane (Wed). Otherwise, the German ZEW survey is likely to report more bleak findings.

Rest of Western Europe

Sweden sees details of what turned out to be further surprisingly friendly CPI data this time for April (Wed) and they may have featured in this month’s Riksbank decision, the minutes to which arrive the same day. In Norway, Tuesday sees the Norges Bank’s Financial Stability Survey but with more interest in the April CPI data (Mon) where we see the CPI-ATE measure rising to 3.2%-3.3%, ie in line with Board thinking.

Japan

Kick starting the week with overall household spending. Household spending was poor in February despite solid wage growth. We will need to see a rebound to know Japanese consumers are not fatigued by new higher prices. Else, it is mostly tier two data but consumer activity is critical to support the next BoJ hike.

Australia

Wage price index on Wednesday will be critical for Australia. The RBA has hiked three times in a roll to curb the rising inflationary pressure. Wage growth is no doubt one of the factors as the labor market remain solid. If we see a hawkish surprise above 4%, it may shift market expectation of another RBA hike, though the likelihood is low. There is also consumer confidence on Tuesday and consumer inflation expectation on Thursday.

NZ

Only RBNZ Inflation expectation on Wednesday would be important. Very likely we will see an upward revision. The magnitude is important as the RBNZ is on the verge from changing from very accommodative to perhaps more tightening.