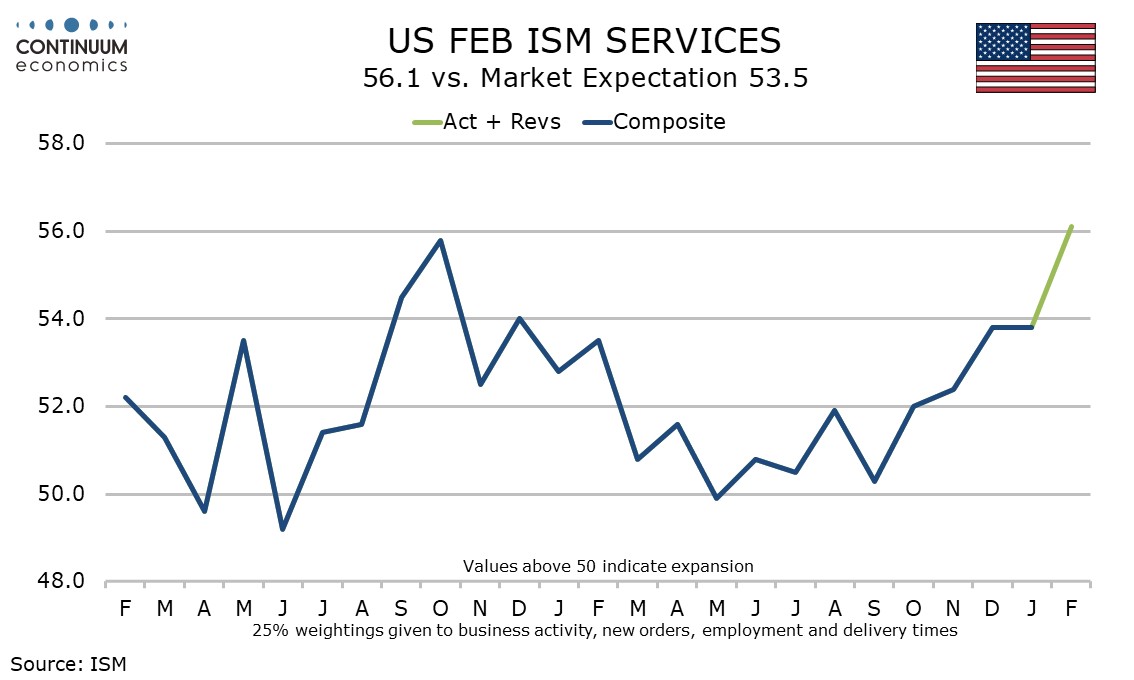

U.S. February ISM Services strength contrasts slower S&P Services PMI

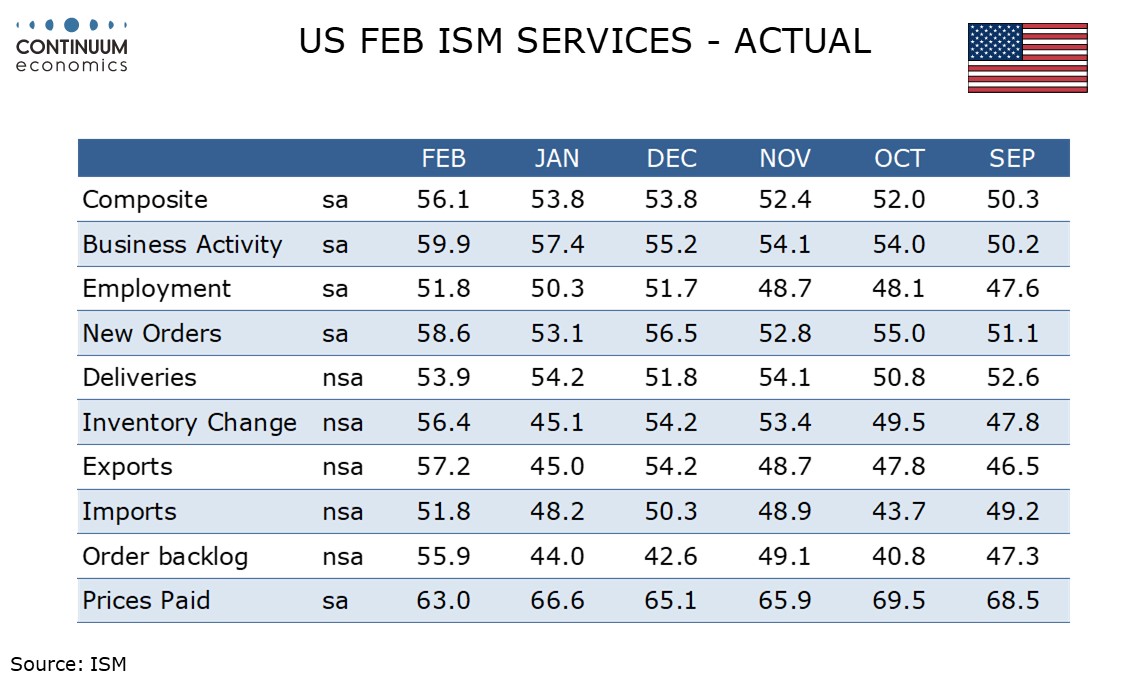

February’s ISM services index of 56.1 from 53.8 is the strongest since July 2022 and in a stark contrast to a weaker S and P services PMI of 51.7, revised down from 52.3 to its weakest level since April 2025. The true picture probably lies somewhere between the two surveys, but averaging the two at 53.9 still suggests a respectable pace of economic growth.

The ISM services detail is positive, with the strongest gain coming in new orders, to 58.6 from 53.1. More moderate gains came from business activity, to an even stronger 59.9 from 57.4, and employment, to 51.8 from 50.3. The only component of the composite to slip was delivery times, to a still firm 53.9 from 54.2.

Prices paid do not contribute to the composite and at 63.0 from 66.6 contrasted an acceleration in ISM manufacturing prices paid. The ISM services price index is seasonally adjusted, but the manufacturing price index is not.

Export and import indices also do not contribute to the composite. The firmer at 57.2 from 45.0 is sharply stronger, comfortably outperforming the latter, though at 51.8 from 48.2 imports also saw a notable improvement.