FX Daily Strategy: Europe, November 4th

AUD slips despite hawkish RBA

EUR soft but downside momentum modest

Scope for JPY gains but a trigger is needed

CHF weakness corrective for now

AUD slips despite hawkish RBA

EUR soft but downside momentum modest

Scope for JPY gains but a trigger is needed

CHF weakness corrective for now

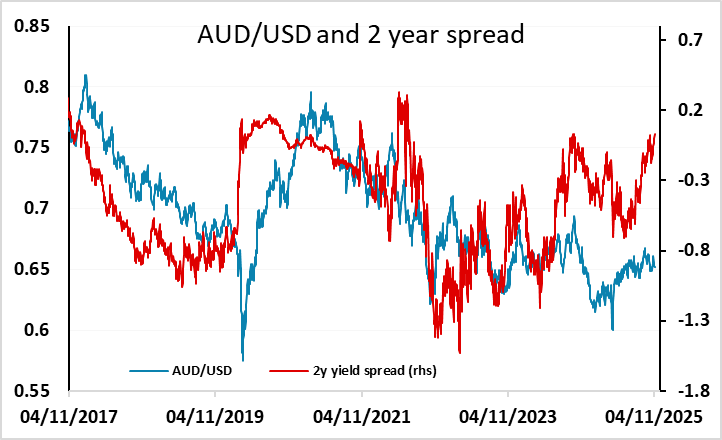

The RBA kept the cash rate unchanged at 3.6% in the November 4th meeting as expected. With headline monthly inflation rising to the upper band of target range in Q3 and showing little sign of moderation in October, the RBA revised their inflation forecast higher and see both trimmed mean and headline CPI to be above the target range throughout most of 2026. They also only assume one more rate cut in 2026, which brings rates to around 3.35%. The revision could support the Aussie in a medium term when market pricing adjusts accordingly, but after a minor rally following the RBA decision, the AUD fell back through the Asian session in line with weakness in global equities. The yield spread picture still looks supportive, but the AUD rarely performs well in risk negative conditions.

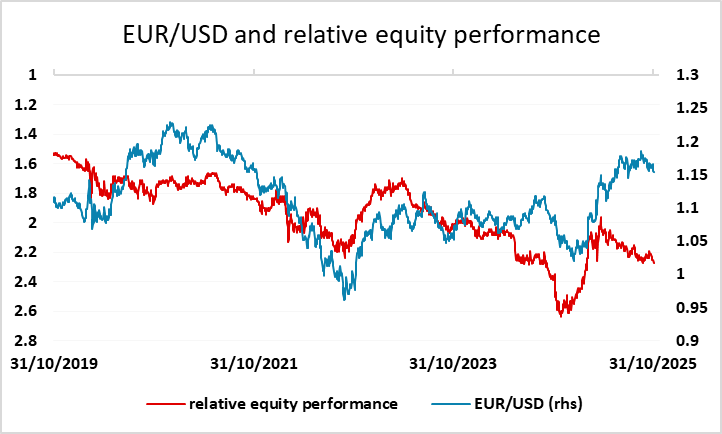

Otherwise, there is very little to focus on. Monday saw the EUR slip back to its lowest since July, once again without much obvious rationale, but the break below the 1.1540 level on Friday and the failure to recover back above it has turned the technical picture bearish. European funds who increased their USD hedges this year and led to the EUR outperformance of the old yield spread correlation are unlikely to reduce them once again despite the recent strong USD performance and the outperformance of US equities, so we wouldn’t expect a sharp EUR move lower. But for the moment the EUR is trading heavy and we could see a drift towards the 1.14 support area.

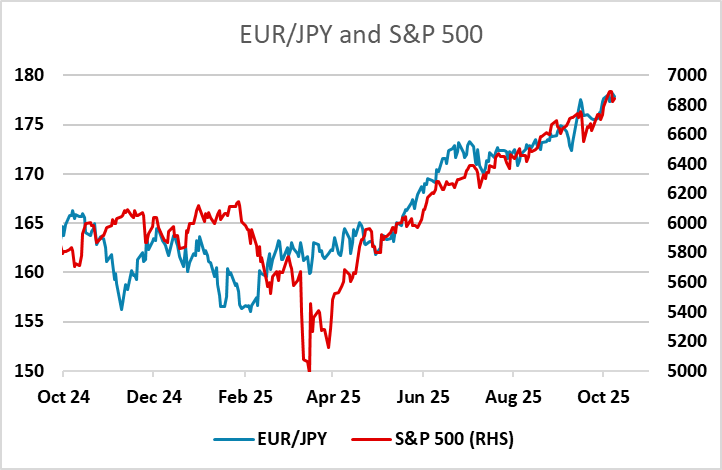

There is more of a case for a decline in EUR/JPY than EUR/USD, with JPY weakness looking increasingly hard to justify now that the new Finance minister has indicated that the recent JPY moves are “rapid and one sided”. Yields spreads and equity risk premia already suggest scope for substantial JPY gains, but EUR/JPY has recently simple been moving up with equities. An equity correction or official intervention still look like a necessary trigger for a major JPY turn, although last week’s comments from Finance minister Katayama do seem to have at least created a short term USD/JPY ceiling at 154.40.

The CHF was the most significant mover on Monday, following the weaker than expected Swiss October CPI data, triggering a EUR/CHF gain back above 0.93. Even so, there is little chance of the SNB seeing the low inflation rate as a reason to reinstitute negative rates, and FX intervention also looks to be off the agenda for now, so extending CHF losses may prove difficult. Of course, it does now make the 0.92 level in EUR/CHF look even better support, and that might encourage some short CHF positioning. There is certainly a case for CHF losses from a value perspective, and from a yield spread perspective, while the economic picture also looks less friendly given the high US tariff on Switzerland. The problem is that these things have not really prevented CHF strength up to now, so for the moment, CHF weakness looks corrective rather than the beginning of a new trend.