FX Daily Strategy: APAC, Oct 23rd

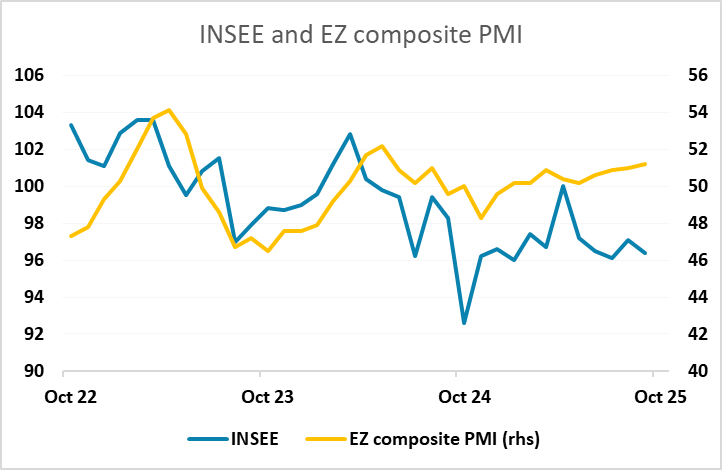

EUR may be vulnerable to weak French confidence data

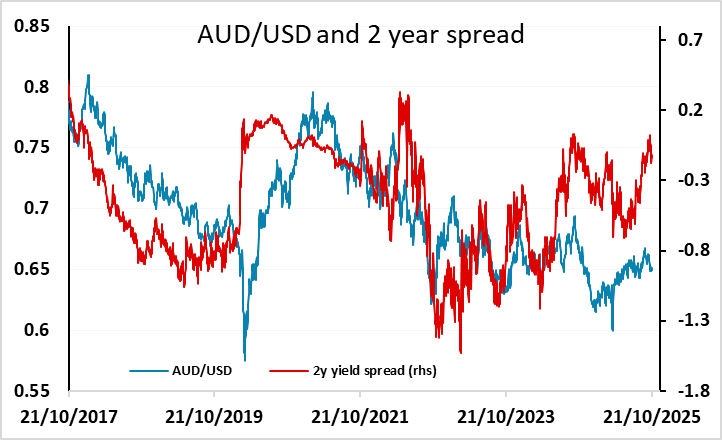

AUD can recover if domestic data is solid

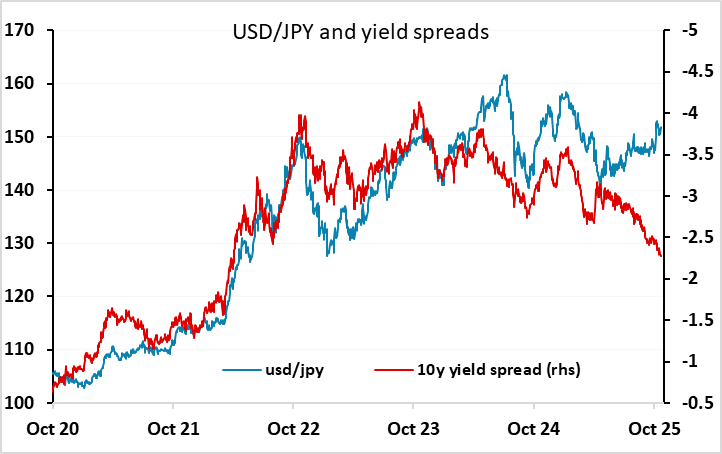

JPY gets little encouragement from new finance minister Katayama

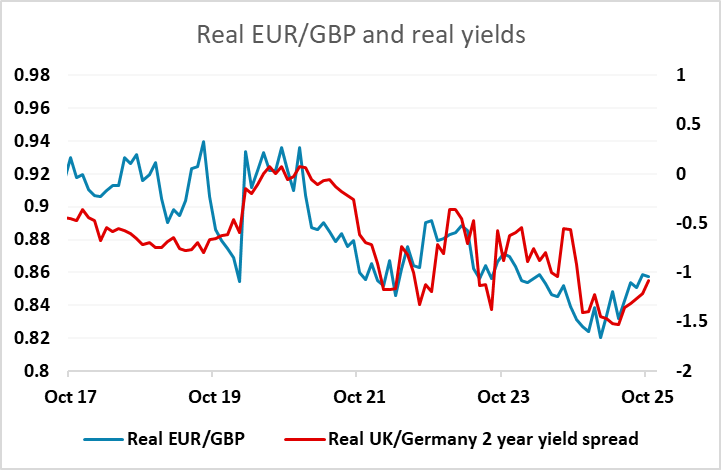

GBP looking more vulnerable after weaker UK CPI

EUR may be vulnerable to weak French confidence data

AUD can recover if domestic data is solid

JPY gets little encouragement from new finance minister Katayama

GBP looking more vulnerable after weaker UK CPI

There is little significant data due on Thursday, with the US jobless claims data still not being released. There is business confidence data in Australia and France, and while it is unlikely that either will have major impact, the market will be on watch for any evidence of weakness in France after the recent downgrade, given the fiscal and political problems the country faces. France has generally been underperforming the rest of Europe, but any further weakness might put some more downward pressure on the EUR, which has moved towards the bottom of its recent range in the last few days.

For the AUD, the quarterly business confidence numbers are accompanied by an RBA bulletin, and we would expect them to provide some support to the AUD which has slipped a little since Trump’s announcement of tariffs on China. The evidence form the domestic economy has still generally been supportive, and some more of the same could propel AUD/USD back above 0.65. However, some resolution to the China tariff question is likely to be necessary if the AUD is to move back towards the top of the year’s range.

USD/JPY didn’t do a great deal on Wednesday, despite comments from new finance minister Katayama. She avoided making any comment about FX rates, and this is significant since the previous finance minister Kato had protested the recent weakness of the JPY. This suggests there is no immediate threat of intervention, any may embolden the JPY bears. She also said that monetary and fiscal policy needed to be co-ordinated and that Japan hadn’t fully exited deflation, which sounds like a preference for monetary policy to be left on hold near term. While she said the specifics of monetary policy were up to the BoJ, an October rate hike might be seen as unwelcome. Of course, that doesn’t mean it can’t happen, but the BoJ may prefer to wait for the specifics of her supplementary budget before acting again. All in all, her comments look slightly JPY negative, inasmuch as policies to strengthen the JPY look unlikely to be implemented. But JPY weakness already looks very overdone given current yield spreads and risk premia, so we still don’t favour JPY downside.

Although we saw GBP decline after the UK CPI data on Wednesday, the decline was largely reversed by the end of European trading on Wednesday, even though the chances of a BoE rate cut in November were seen to have risen significantly, with the market now pricing it as 40% chance from 15% ahead of the data. We still see the next cut as more likely to come in December after the MPC have seen Chancellor Reeves’ budget, but the resilience of GBP looks a little complacent. The inflationary problems in the UK do look to be diminishing, and there is little good rationale for real UK rates to be above Eurozone rates in the longer run. So the medium term risks or EUR/GBP are on the upside, and we would expect some upward pressure to be maintained as we head towards the November MPC meeting.