8th Consecutive Cut: CBR Reduced the Rate to 14.5% Despite Risks

Bottom Line: Following the Central Bank of Russia’s (CBR) 50 bps cut on March 20—driven by the disinflationary trend in Q1—the CBR continued its easing cycle on April 24 reducing the rate from 15.0% to 14.5% despite inflationary risks. CBR maintained a cautious tone on inflation and future policy decisions. We are maintaining our year-end key rate forecast of 13% for 2026, as the need for higher real yields will require the CBR to keep monetary policy restrictive for the foreseeable future coupled with inflationary risks.

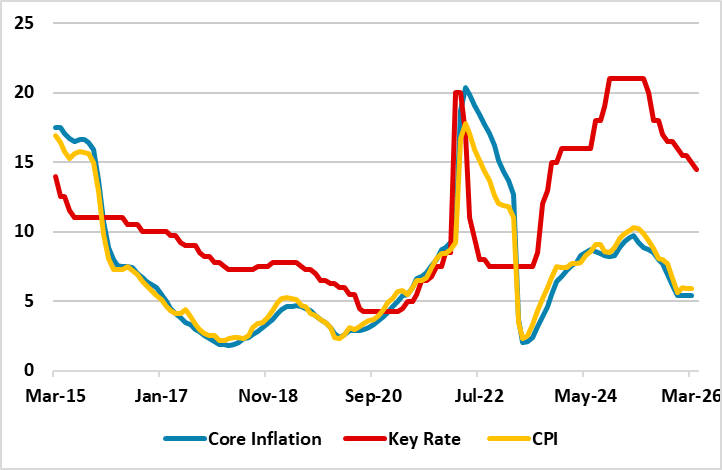

Figure 1: CPI, Core Inflation (YoY, % Change) and Policy Rate (%), January 2015 – April 2026

Source: Continuum Economics

Following a key rate cut to 15% on March 20, the Central Bank of Russia (CBR) further reduced the policy rate to 14.5% on April 24. In March, annual inflation slowed to 5.9%, driven by the lagged effects of previous monetary tightening, a resilient ruble, and moderate core inflation. This trend was supported by improving inflation expectations; recent data showed household expectations edged down to 12.9% in April from 13.4% in March. Notably, expectations among respondents with savings saw a sharper decline, dropping from 12.3% to 11.4%.

Following the MPC decision, CBR said in its written statement that the measures of underlying price growth have not yet decreased, adding that uncertainty remains significant regarding the external environment and fiscal policy parameters. CBR added that it would consider the need for further key rate reductions at its upcoming meetings, depending on the stability of the slowdown in inflation and inflation expectations.

The CBR projects annual inflation will decline to 4.5–5.5% in 2026, aiming for a return to its 4% target by 2027. However, we believe meeting this target range will be challenging in 2026. Persistent sanctions, the fallout from the conflict in Iran, and sustained military spending are likely to prolong the disinflationary process beyond the CBR's expectations. In our view, a peace deal in Ukraine remains the primary catalyst needed to ease inflationary pressures and resolve chronic supply-demand imbalances.

We are maintaining our year-end key rate forecast of 13% for 2026, as the need for higher real yields will require the CBR to keep monetary policy restrictive for the foreseeable future coupled with inflationary risks.