FX Daily Strategy: Europe, May 8th

US and Canadian employment data offer some USD upside risks

Focus remains on US/Iran negotiations with some good news already priced in

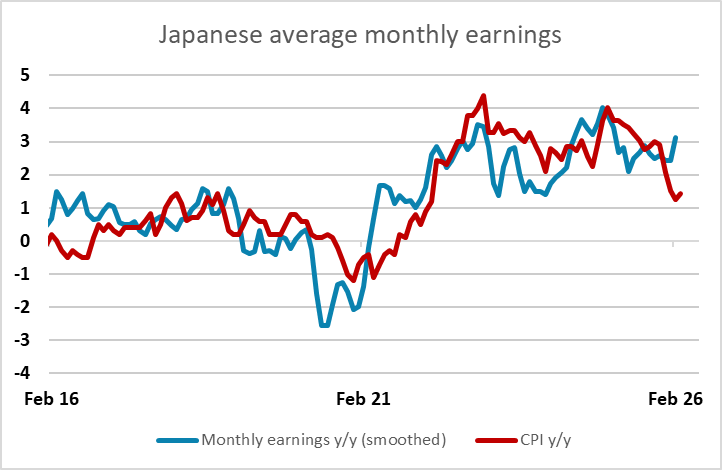

Japanese wage data misses

GBP vulnerable to political fallout from local elections

US and Canadian employment data will be the main data focus on Friday, although developments in the US/Iran negotiations may well be more market moving.

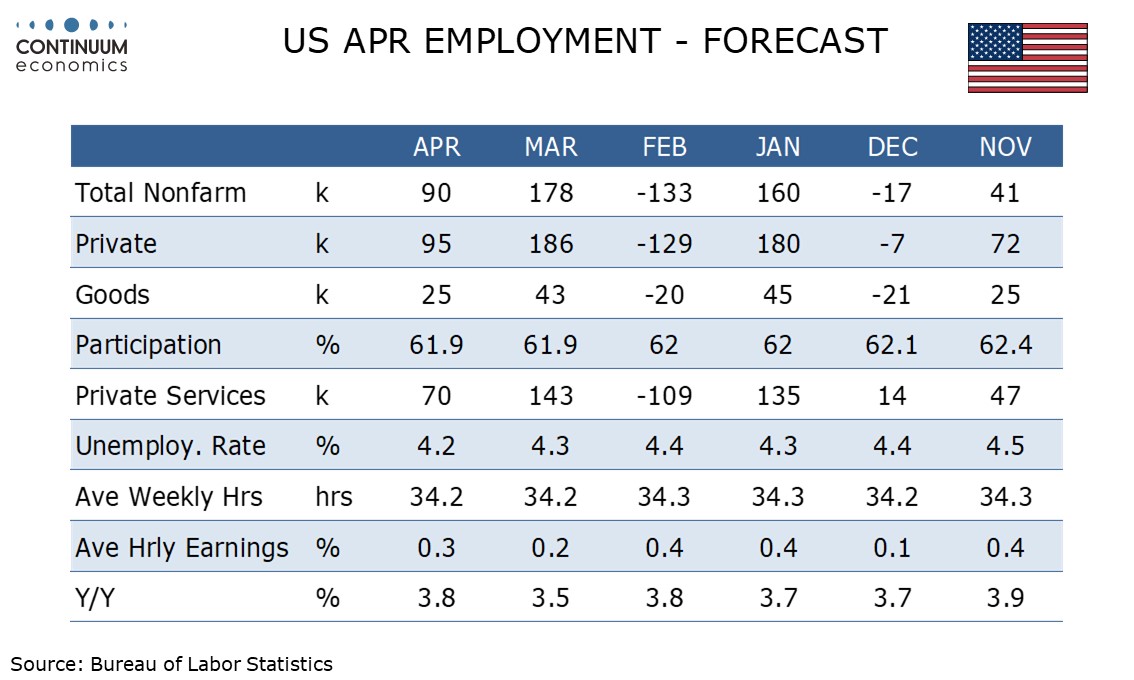

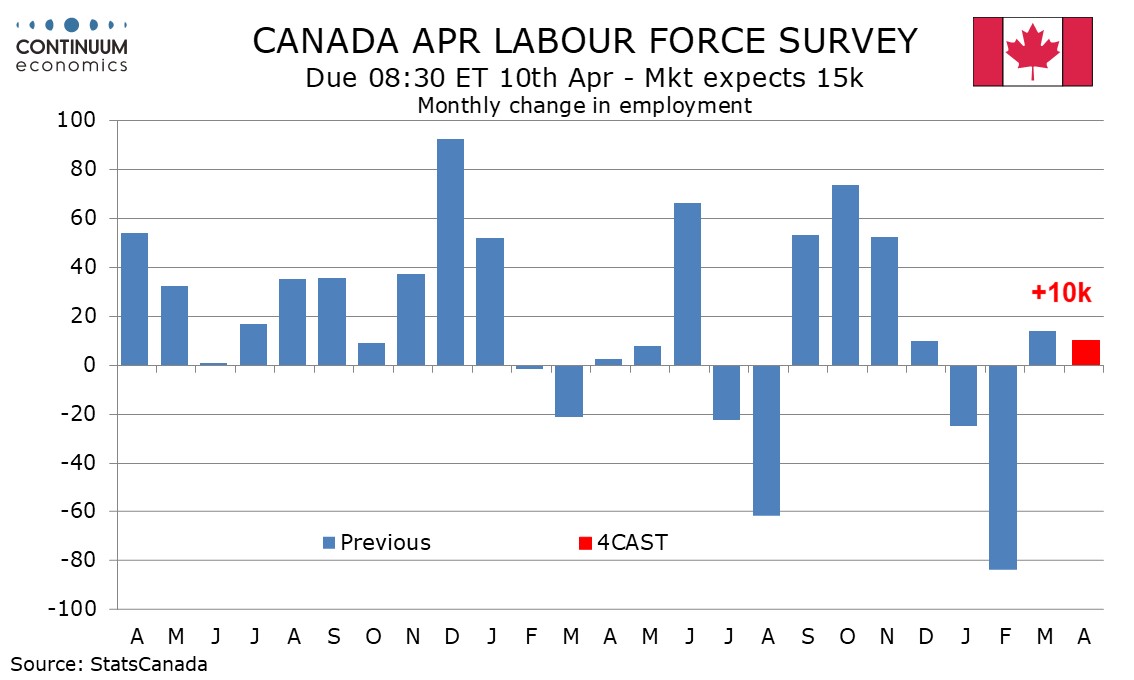

We expect April’s US non-farm payroll to rise by 90k overall and by 95k in the private sector, less strong than in March but implying some improvement in trend. We expect unemployment to slip to 4.2% from 4.3% and an in line with trend 0.3% increase in average hourly earnings. We expect Canadian employment to increase by 10k in March, a second straight modest rise to follow a gain of 14.1k in March, still not close to erasing the steep loss of 83.9k in February which extended a substantial 24.8k decline in January. We expect a 6.7% unemployment rate for a third straight month.

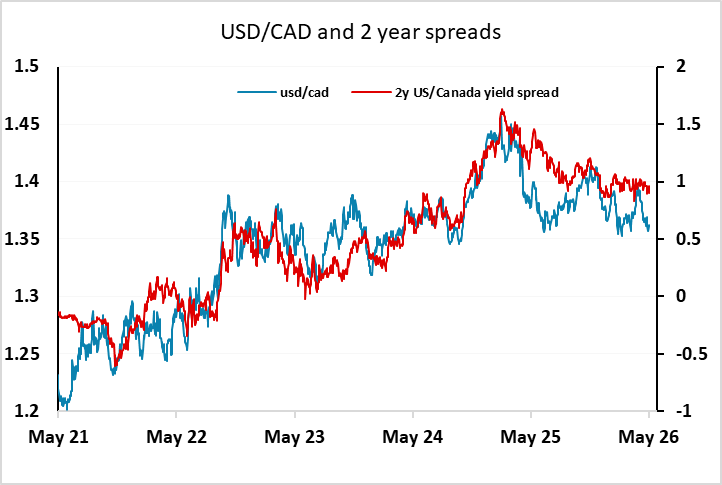

While our forecast for US employment is slightly above consensus, it’s not enough to suggests a significant market reaction. Other labour market indicators, notably the weekly claims data, already indicate that the labour market remains reasonably solid, and it would take a substantial deviation from consensus to significantly change the market’s view that the economy and the labour market remain solid, if not particularly vibrant. Nevertheless, we would see the risks for the US numbers as being on the strong side and the USD upside, perhaps particularly against the CAD as the modest increase we anticipate doesn’t compensate for the weakness seen earlier in the year.

However, in all likelihood the data will have a modest and short term effect, with Middle East developments having more potential to impact the market. The strength of risk sensitive assets and currencies this week and the softness of the USD suggests that a limited agreement to end hostilities is now close to being priced in, although this would leave the main issues of the Iranian nuclear programme and the Straits of Hormuz access unresolved pending further negotiations. There is therefore a skew towards USD upside and risk downside on Middle East news, as the most likely risk positive outcome is essentially priced in.

Otherwise there is important Japanese wage data for March due first thing. The February data showed some strength, with wage growth moving above CPI inflation for the first time in a while. Further evidence along these lines would support the case for a 25bp June rate hike from the BoJ, which is currently around 65% priced in, and would add to the upward pressure on the JPY provided by recent FX intervention.

Japan March Labor Cash Earning missed estimate but is still showing a 2.7% y/y growth. While it is disappointing, the trajectory continue to points toward stronger than average wage growth. The results of wage negotiation may not be fully applied yet but one must also be aware of potential slowing, in case business fear margin squeeze from energy shock to withheld strong wage hikes.

GBP will also be in focus with potential for some impact from the results of Thursday’s local elections on national politics. There is also a speech from BoE governor Bailey. It’s hard to see much upside for GBP from the political side, and with EUR/GBP close to the lows of the year near 0.86, we favour the upside.