SARB Kept the Key Rate Stable at 6.75% Due to Inflationary Risks

Bottom Line: South African Reserve Bank (SARB) kept the policy rate unchanged at 6.75% during the MPC on March 26 due to inflationary risks. We anticipate that a weakening rand, driven by higher oil prices and surging food costs to the war in Iran, will likely push inflation over 4% in Q2/Q3, and SARB will likely halt key rate stable in H1 2026 due to upside risks to inflation.

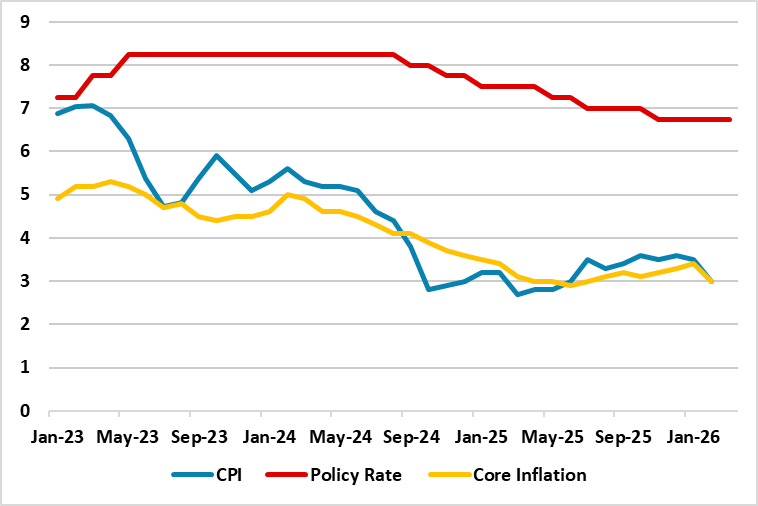

Figure 1: Policy Rate (%), CPI and Core Inflation (YoY, % Change), January 2023 – March 2026

Source: Continuum Economics

SARB’s MPC convened on March 26 announcing the second key rate decision of 2026, and kept key rate stable at 6.75% due to inflationary risks related to Iran war. All members of the MPC voted to keep the rate unchanged.

SARB made important changes in its forecasts on March 26. SARB now anticipates that the headline inflation to accelerate to around 4% soon, with fuel inflation of more than 18% in Q2. SARB also revised its policy outlook, now projecting only one rate cut instead of two previously, while assessing two possible Iran conflict scenarios, a short-term two-month scenario and a prolonged one-year scenario, both implying the need for higher interest rates.

SARB governor Kganyago said on March 26 that "Since our last meeting, the key event has been the outbreak of conflict in the Middle East. Prices for commodities like oil, gas and fertiliser have moved sharply higher. (…) We are just a few weeks into this shock, and conditions remain extremely uncertain. At this stage, it is obvious that global inflation will be higher in the near term, while growth will probably suffer from supply-chain disruptions and rising costs. But the longer-term outlook is less clear."

Despite annual inflation edged down to 3.0% y/y in February, the lowest since June 2025, driven by slowdown in prices of transportation and food and non-alcoholic beverages (NAB) and the inflation stayed within the SARB's 1 percentage point tolerance band of 3% target supported by no power cuts (loadshedding), stronger Rand (ZAR), lower oil prices in February; we also anticipate that a weakening rand, driven by higher oil prices and surging food costs due to the war in Iran, will likely push inflation over 4% in Q2/Q3. We expect convergence to the 3% target will be slower than initially projected. While we think inflation to ease in late Q3/Q4 as the Iran conflict potentially subsides, but this recovery will take time. (Note: We foresee average inflation will hit 3.8% and 3.5% in 2026 and 2027, respectively).

We believe SARB will likely halt its cutting cycle H1. SARB could consider reducing the rates in H2 2026, which will depend on the inflation trajectory, though this is not our baseline scenario since SARB will likely act cautious against any expected inflation uptick taking the new inflation target into consideration. Our end-year key rate predictions remain at 6.75% and 6.25% for 2026 and 2027, respectively. SARB will likely continue cuts in 2027 once the Iran conflict loses momentum, most of the geopolitical risk premium dissipates and oil prices decline with market dynamics.