FX Daily Strategy: APAC, March 26th

UK CPI and fiscal statement the focus

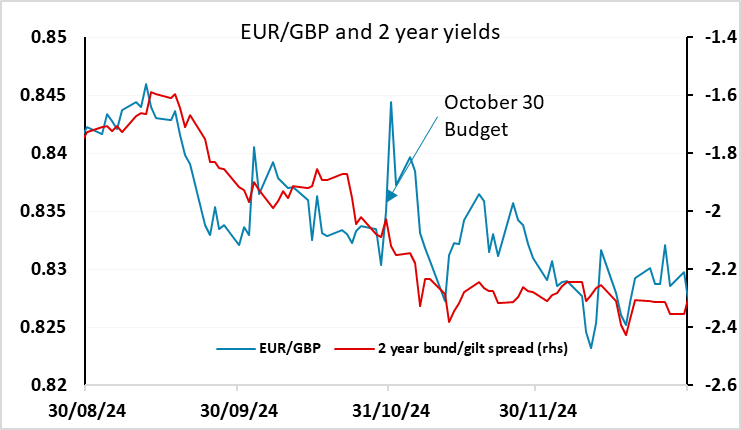

GBP risks mainly on the downside

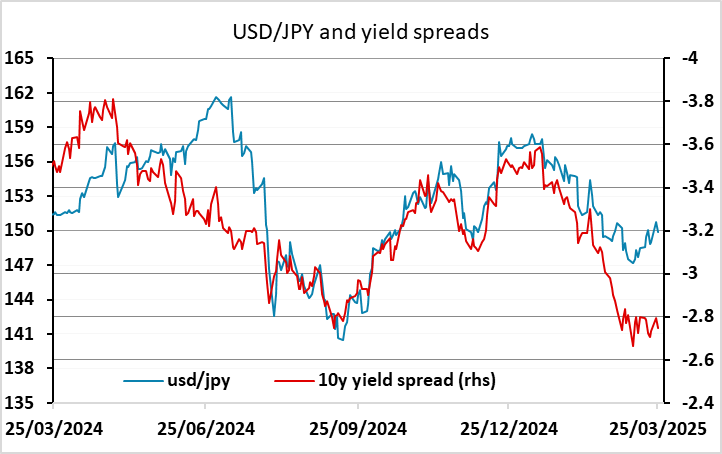

USD likely to remains under pressure against the JPY

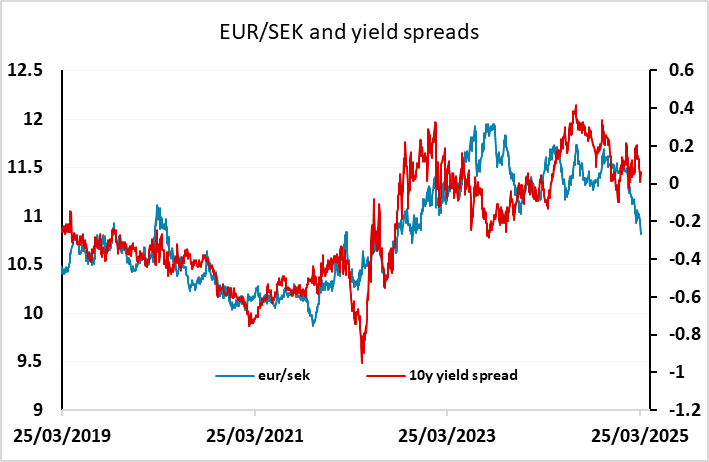

Swedish data needs to be strong to justify recent SEK strength

UK CPI and fiscal statement the focus

GBP risks mainly on the downside

USD likely to remains under pressure against the JPY

Swedish data needs to be strong to justify recent SEK strength

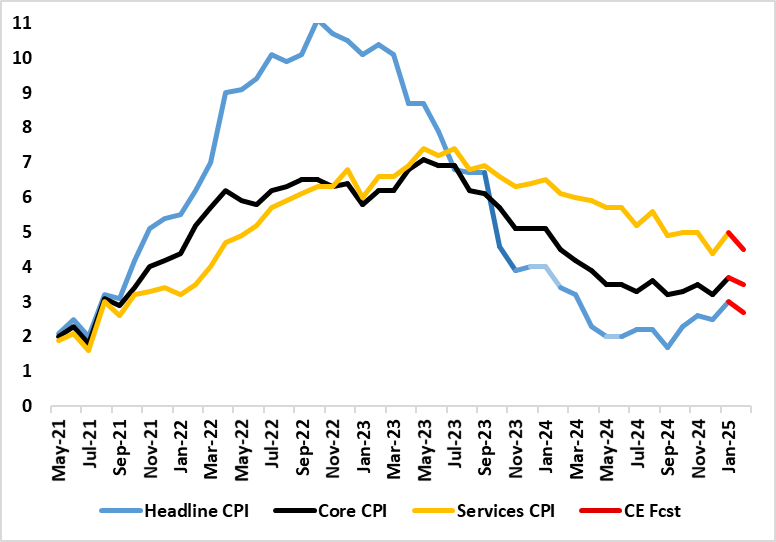

February Inflation Slips Back?

Source: ONS, Continuum Economics

The UK should be the main focus on Wednesday, with UK CPI data and the spring fiscal statement. January’s CPI numbers showed a marked bounce back up, with the 0.5 ppt rise taking it to a 10-month high of 3.0%, this being above consensus and BoE thinking. Notably services jumped from 4.4% to 5.0%, actually below expectations, having been driven higher by a swing in airfares and the rise in school fees, but with further upward pressure evident in rents too. We think some of this services noise will reverse in February and despite the impact of higher alcohol duties and fuel prices headline CPI inflation may slip back to 2.7% or a notch higher – i.e. the BoE projection of 2.8%, but either way below the consensus estimate of 2.9%. This should be mildly GBP negative, increasing the chance of a May BoE rate cut, which is currently priced at only around a 45% chance.

Even so, the government fiscal update due at 10GMT may have more market impact. The recent history of UK fiscal announcements has not tended to be initially GBP positive. The current government’s first Budget last autumn saw EUR/GBP spike more than a figure higher even though gilt yields also rose on the day, although the GBP losses were soon reversed. The Truss Budget in 2022 saw a much larger GBP decline, partly due to some technical gilt market issues. However, both sell offs reflected market concern about the UK fiscal position. This time around Chancellor Reeves will have to cope with lower growth estimates, higher defence spending and higher deb interest. Some spending cuts have already been announced, but there may need to be some more if GBP is to escape the announcement unscathed. Bigger picture, we still see EUR/GBP risks to the upside, as we see larger BoE rate cuts than are currently priced in, and GBP is trading at expensive levels in real terms. So we would favour a EUR/GBP move back above 0.84 if there is no action to deal with the deteriorating outlook for public finances.

In the US there is durable goods orders data, but these seem unlikely to significantly affect expectations for the economy. At this stage, most of the US data has remained quite solid, and there was also some optimism on Monday that the Trump tariff increases might be less damaging than feared. But the weak Conference Board consumer confidence index released on Tuesday, hitting the lowest level since the pandemic, maintains the concern that Trump’s policies may weaken the economy via the impact on confidence. The equity market remains priced for a strong economic performance, so it still looks vulnerable to these concerns. We consequently still see USD/JPY as very vulnerable here. Current yield spreads already suggest scope for substantial declines, which may materialise more quickly in the event of any equity sell off.

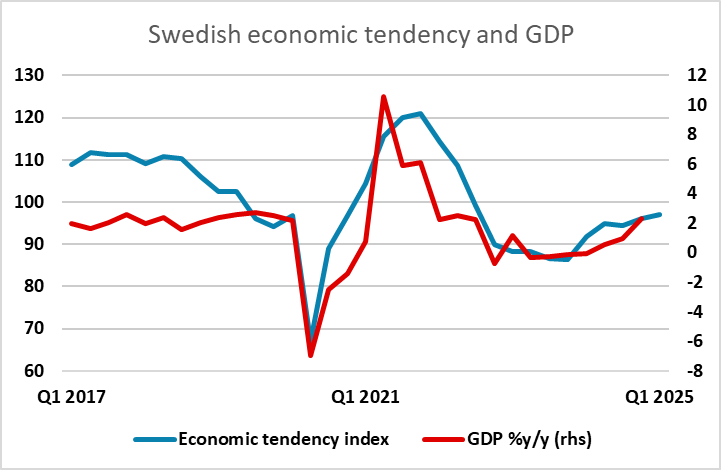

As well as the UK data we have Swedish confidence data and the economic tendency survey in Europe. This has been improving of late, and Swedish GDP growth picked up steadily through 2024 in line with the improvement in the economic tendency index. The SEK tends to be something of a barometer of confidence in the European economy as a whole, and the SEK has been strengthening in recent weeks beyond the level suggested by yield spreads on the back of rising expectations of European growth based on higher defence spending and hopes of a Ukraine ceasefire. But the SEK has already come a long way, and it will need some very strong numbers to support further gains from here.