FX Daily Strategy: Asia, March 6th

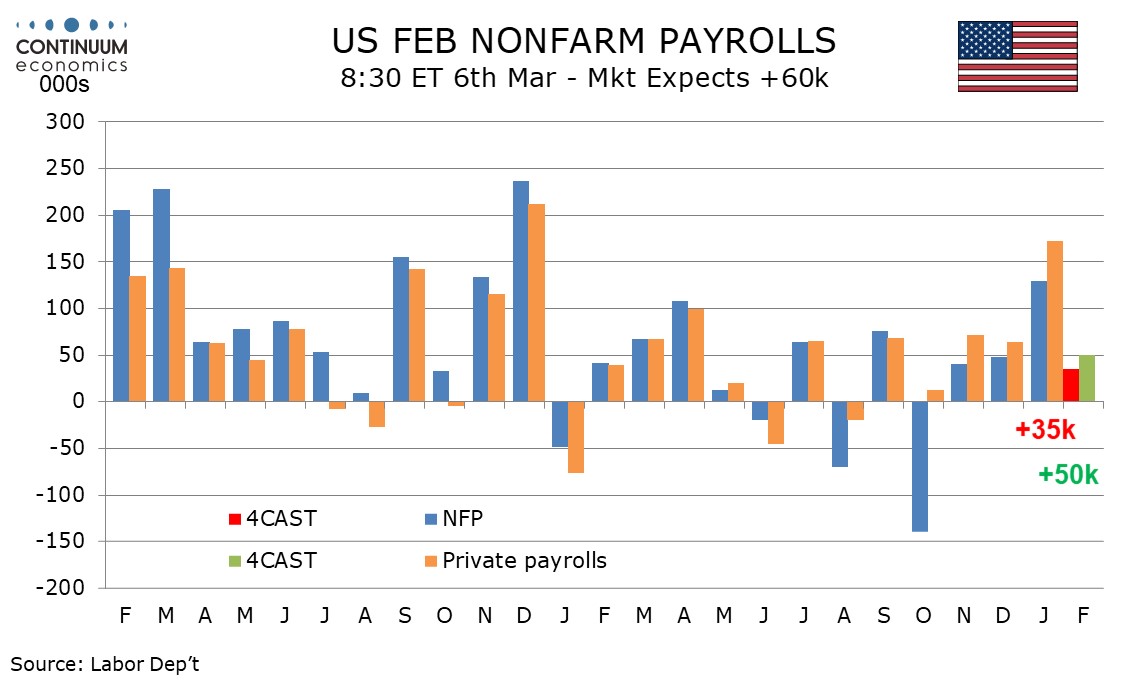

U.S. February Non-Farm Payrolls Not as strong as January

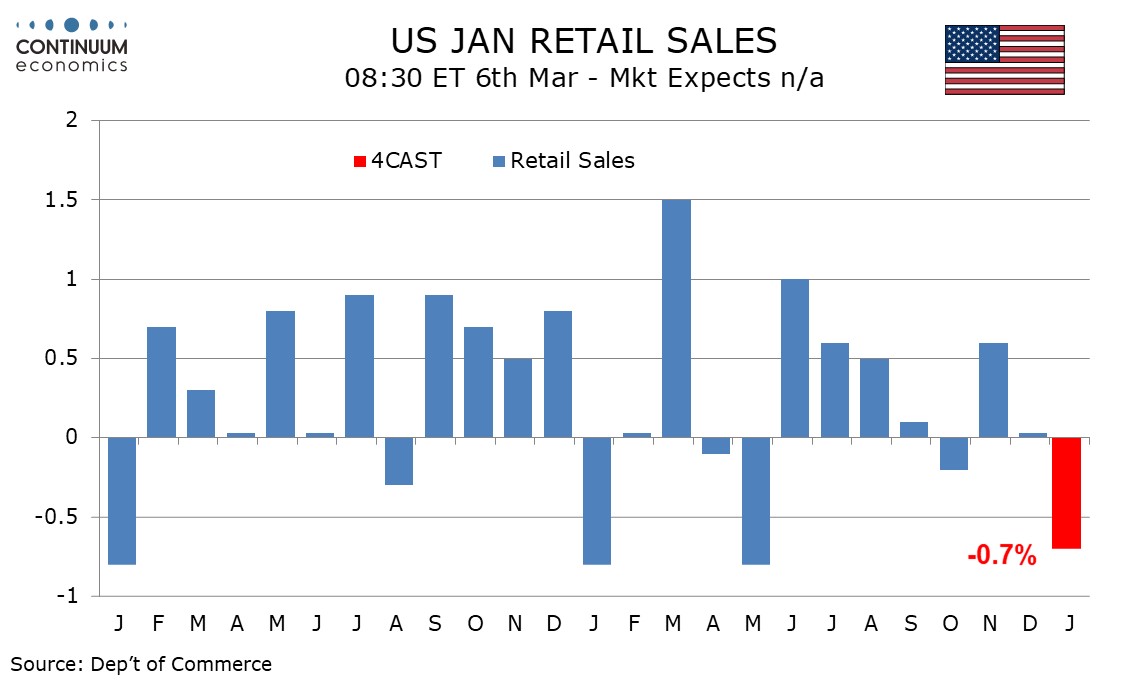

U.S. Retail Sales More to downside risk

Markets and the Iran War

We expect February’s non-farm payroll to rise by 35k overall and by 50k in the private sector, both four month lows and significantly slower than January’s above trend respective gains of 130k and 172k. We expect unemployment to edge up to 4.4% from 4.3%, reversing a January dip, and average hourly earnings to rise by 0.3%, in line with trend. January’s strength was led by health care, which increased by 123.5k, and a significant slowing is likely in February, though the sector is still likely to fully explain February’s payroll gain, and most of that in the private sector. Revisions tend to be negative and January data may be revised lower, though probably only by around 25k, leaving the month still well above the late 2024 trend.

January’s data was supported by strongly positive seasonal adjustments, which turn negative in February. January’s data was also surveyed before some bad weather in late January, which would weigh on February data, though initial claims were back to normal in February’s payroll survey week after a bounce during the cold weather spell. A clearly negative payroll looks unlikely.

We expect retail sales to see a weak month in January, falling by 0.7% overall, with declines of 0.4% ex auto and 0.2% ex auto and gasoline. Bad weather late in the month will contribute to the decline. Industry data shows a significant dip in auto sales while CPI showed a decline in gasoline prices in January. Weather is not the only downside risk. Consumer spending ran well ahead of near flat real disposable income in both Q3 and Q4, suggesting that a loss of momentum in December retail sales may continue in January.

Retail sales in January are often sensitive to weather, falling by 0.8% in January of 2025 and 2024 but surging by 4.4% in January of 2023 when weather was unusually mild, before correcting in subsequent months. A 0.2% decline ex auto and gasoline would be the weakest since a 0.5% fall in January 2025. 3 month/3 month data would be the weakest since early 2024, overall, ex autos and ex autos and gasoline.

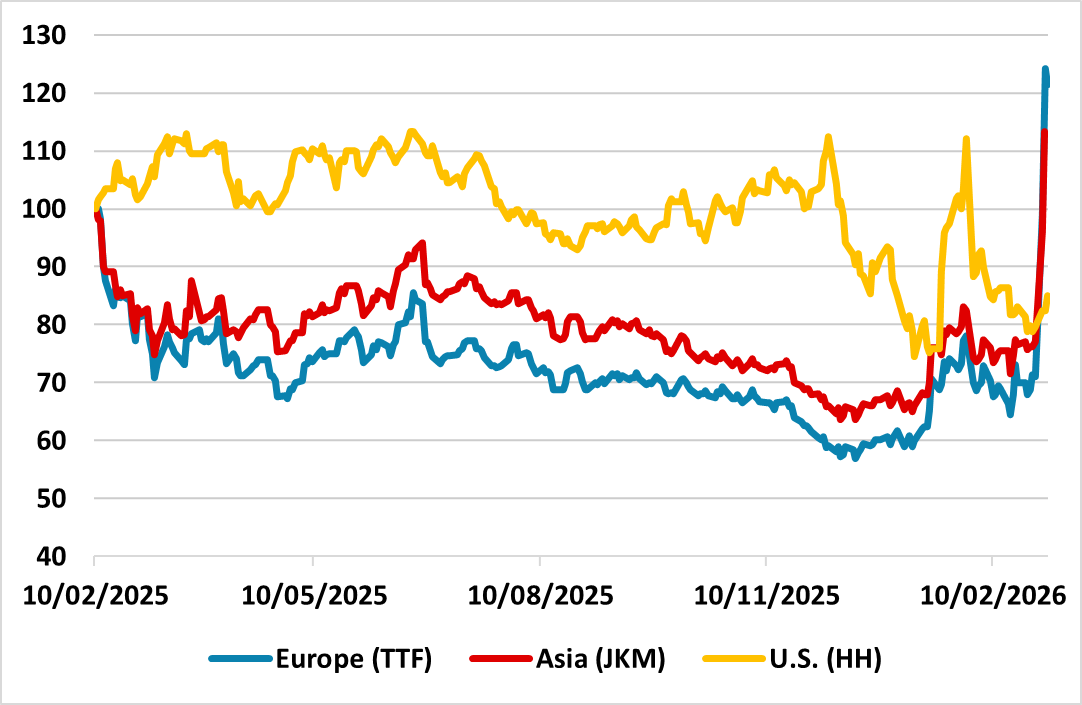

Figure: Global Gas Prices (Feb 2025 = 100)

The Trump administration’s objective appears to be pivoting from regime change to hurting Iran ballistic missile capabilities, which argues for a 2-4 week war rather than a prolonged war. However, the most intense missile battles will likely occur in the next one week and markets are hyper sensitive to oil or gas production or export facilities being hit and how long they will stop production/exports. Uncertainty also exists whether enough Gulf countries interceptor missiles exist for Iran drones. Risk off has not finished yet.

The economic impact for the global economy depends both on the length of the war (plus associated effective closure of straits of Hormoz) and any lasting damage to oil/gas production and export facilities. The Trump administration’s objective appears to be pivoting from regime change to hurting Iran ballistic missile capabilities and doing a deal with a transformed regime, which argues for a 2-4 week war rather than a prolonged war. Trump offer of U.S. backed reasonable tanker insurance and navel escorts through the straits of Hormuz suggest some economic pain is starting to impact the Trump administration. However, the most intense missile battles will likely occur in the next one week between Iran and Israel/U.S. and Gulf countries and markets are hyper sensitive to production or export facilities being hit and how long they will stop production/exports. More focus exists currently on Qatar LNG production stoppage, that has caused a much more significant jump in gas than oil prices. More oil or gas production damage could accelerate the equity market selloff. Meanwhile, the inflation pain is more directed towards Europe and Asia currently (Figure), as the U.S. is self-sufficient in gas production and the rise in Henry Hub gas prices has been much less. The added uncertainty is that though Iran missiles may only last another week, the less lethal drone stockpile could be larger and outlive Gulf countries interceptor missile defences. Risk off has not finished yet.