Iran/U.S.: A New War or Escalating to Deescalate?

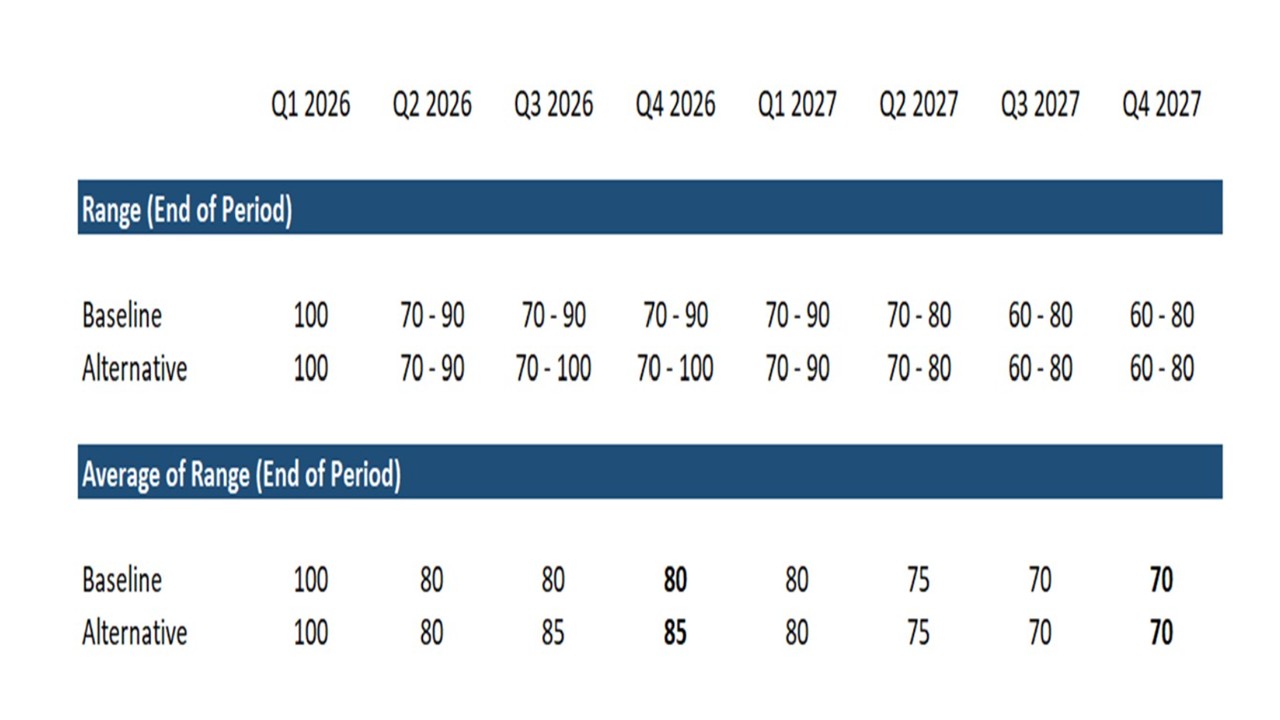

· Our baseline remains that the MOU will hold and that the Strait of Hormuz will reopen. Iran can be pressured economically by the U.S. naval blockade being re-established. Additionally, President Trump loves to escalate to de-escalate to get a deal. This is a 60% probability scenario, with WTI forecast at USD80 by end 2026. Our alternative scenario is that the Strait continues to close intermittently and WTI by end 2026 at USD85.

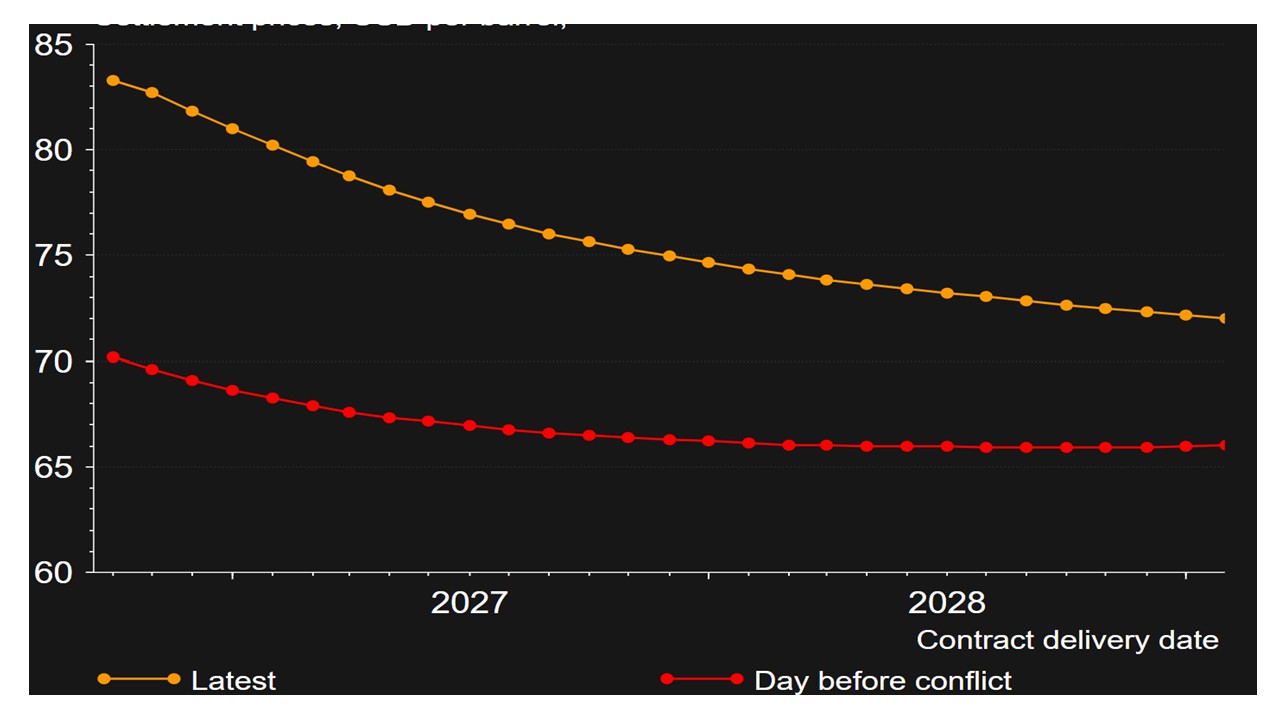

Figure 1: Brent Futures Curve Start of Conflict versus July 14 (USD)

Source: Datastream

After three days of tit for tat Iranian and U.S. strikes, the June MOU is on shaky ground. The U.S. is restarting the naval blockade and potentially charging a 20% protection fee for shipping. This has boosted oil prices, with the near futures contract up since late-June and the whole future curve above pre-war levels still (Figure 1). This is a dilemma for DM central banks, as hopes that the MOU deal would bring down energy prices further proves far from certain.

Our baseline remains that the MOU will hold and that the Straits of Hormuz will reopen. Iran can be pressured economically by the U.S. naval blockade being re-established. Additionally, President Trump loves to escalate to de-escalate to get a deal, while the Republicans are under pressure before the mid-term elections for the Iran war worsening cost of living problems – gasoline could be heading back above USD4, with the latest bounce in oil prices. It is also noticeable so far that Iran attacks in the region have been focused on U.S. military bases and have not extended to hitting energy infrastructure. We still attach a 60% probability to the Straits of Hormuz reopening again (here), though this is unlikely to get back to pre-war shipping movements until the 60 day deal is extended and made semi-permanent. In Figure 2, we assume only partial reopening of the Straits of Hormuz, plus some temporary inventory rebuild, to keep oil prices elevated through end 2026.

Figure 2: Oil Price Scenarios (USD)

Source: Continuum Economics

Our alternative scenario (40% probability) is that the closure of the Strait of Hormuz extends beyond a couple of days and/or reoccurs in the coming months. Iran leadership appears split over the MOU with the U.S., with hardliners wanting to ensure that a southern route around Oman is not established and this was the cause of the recent escalation. Additionally, the fog of war could mean a military escalation. In the 1987-88 tanker wars, Iran hit a U.S. warship and prompted the U.S. to escalate by hitting Iran including oil fields.

Global financial markets and central banks will watch the situation closely, but assume that the baseline is for a partial reopening of the Strait of Hormuz. This could keep the ECB sounding hawkish at the July 23 ECB meeting, though we remain of the view that the decline in energy prices from the peak means that the June ECB hike is a one off. The Fed’s newly reduced forward guidance means that the market will continue to fear a rate hike in the autumn, but not in the September meeting. Even so, Fed Warsh will be watched closely today for any guidance.