FX Daily Strategy: N America, March 27th

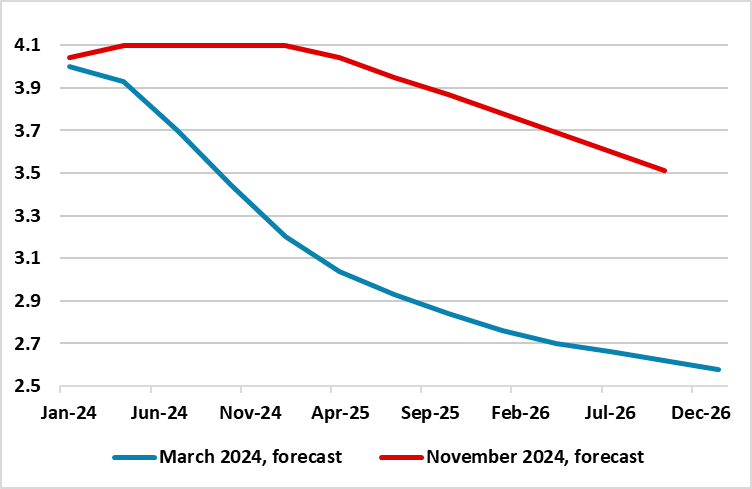

No policy change at Riksbank meeting, but big decline in forecast rate path.

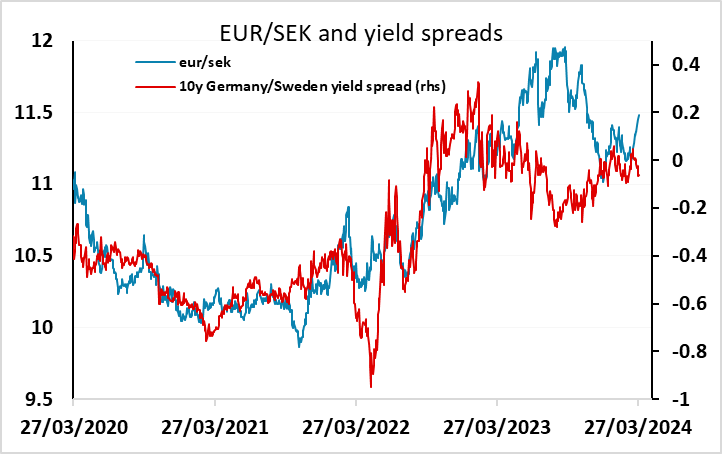

Even so, SEK risks may be on the upside

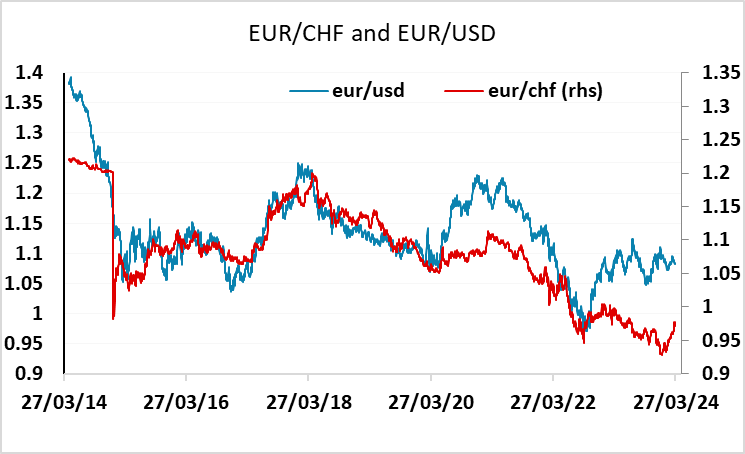

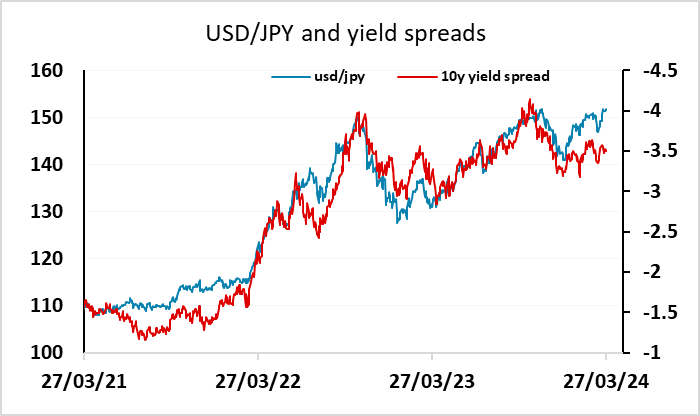

CHF the preferred funding currency as threats of JPY intervention increase

No policy change at Riksbank meeting, but big decline in forecast rate path.

Even so, SEK risks may be on the upside

CHF the preferred funding currency as threats of JPY intervention increase

Riksbank policy rate projections

The SEK had already been soft in the last few weeks, and has fallen further after the latest Riksbank meeting, in which they have made a big shift to the downside in their projected rate path. Some shift lower had been anticipated, with the market pricing in around 90bps of easing by year end, compared to no change projected in the November MPR. An easier stance had already been flagged in the February update. However, the 3.2% policy rate now projected for Q1 2025 is still slightly above the 3.1% the market was pricing in by December this year before the meeting. While there was a dip in rates immediately after the decision, the pace of cuts in the front year is now priced to be slightly slower than it was ahead of the meeting, with the policy rate priced at 3.17% in December.

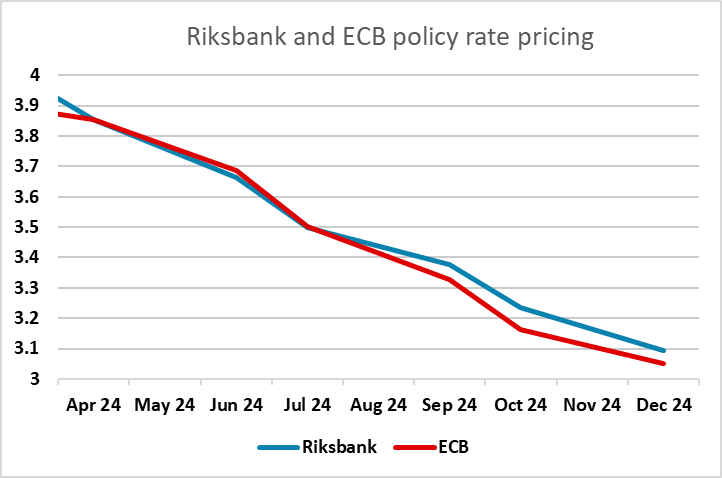

A May rate cut is still in the balance, with a cut only fully priced by June. It may depend on the performance of the SEK. The SEK has been weak in recent weeks, with EUR/SEK rising 35 figures since the March 12 low at 11.13. We have seen a modest move up after the Riksbank announcement, but we doubt there is much more upside with the upmove not correlating with the moves in yield spreads and recent Swedish data justifying a slightly more optimistic view of the economy. If EUR/SEK stays near 11.50, we doubt we will see a May cut, and that disappointment would likely push EUR/SEK lower, so risks should be on the downside for EUR/SEK.

Elsewhere, there isn’t a great deal on the calendar, although there was provisional Spanish CPI for March, the first take on Eurozone inflation. Easter holidays mean the Eurozone numbers as a whole aren’t coming until next week. Spanish inflation does sometimes provide a lead, and this month saw a relatively sharp m/m rise of 1.3% m/m in HICP, although this was essentially in line with expectations. This probably won’t have much impact on expectations of Eurozone inflation as a whole, but may limit the downside scope for EUR yields and the EUR.

The USD was modestly firm on Tuesday in generally quiet trading, and although there were no major moves, it is notable that USD/JPY broke to a new 24 year high of 151.94 overnight, despite the increasing volume of threats of intervention from the MoF and BoJ. This JPY was however not quite as soft as the CHF, which also fell back. After the SNB rate cut last week, the CHF now looks like the preferred funding currency, with JPY downside likely limited by intervention concern, and value very much suggesting there is a lot more downside for the CHF.