FX Daily Strategy: Asia, May 13th

Australia Wage Growth Unlikely Trigger another RBA Hike

Aussie Still Supported above 0.7200

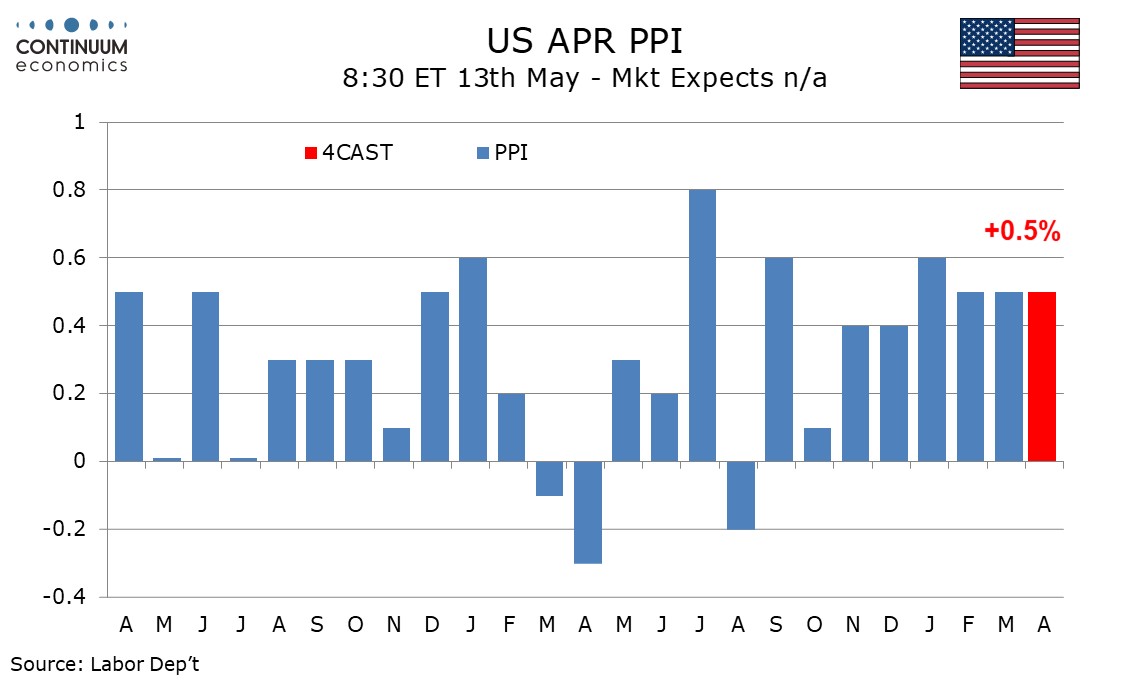

U.S. April PPI Core rates to pick up

The Q1 Australian Wage growth is unlikely to persuade the RBA to hike four meeting in a row. Widely expected to be above 3% y/y, the growth represents the solid Australian labor market. However, given the recent moderation of labor market, there will unlikely be any upside surprise for the figure. The energy shock, may in fact, slows wage growth in coming quarter if business margin is squeezed heavily before government subsidy arriving.

The RBA has hiked three times in a row and a fourth require significant inflationary pressure. It will most likely come from the prolonged physical disruption of Strait of Hormuz, rather than strong domestic demand and wage growth.

On the chart, the pair is still supported above the .7200 level to keep pressure on the upside and see scope for retest of .7278/80, current year high and June 2022 high. Break here will see room for extension of the gains from the April 2025 year low to target resistance at the .7300/.7400 congestion. However, overbought daily studies and a rising wedge pattern caution corrective pullback. Break of the 7200 level ease the upside pressure and see room for pullback the strong support at .7135/.7100 higher lows, which is expected to underpin.

We expect PPI to rise by 0.5% overall in April for a third straight month. We expect the lift from energy to be less sharp than in March, but the core rates to pick up from below trend March gains, ex food and energy to 0.3% from 0.1%, and ex food, energy and trade to 0.4% from 0.2%. The core rates would be similar to February’s when ex food and energy rose by 0.3% and ex food, energy and trade rose by 0.5%, and less strong than in January, when respective gains of 0.8% and 0.5% were seen. We expect a 4.0% increase in energy after a rise of 8.4% in March and food to rebound by 0.6% after a 0.3% decline in March.

We expect goods ex food and energy to rise by 0.3% after March’s 4-month low of 0.2%, but this series has probably peaked as the impact of tariffs starts to fade. We expect services to rise by 0.3% after a flat March, with continued strength in transport and utilities, which rose by 1.3% in March, but a third straight moderate decline in trade, extending a correction from strong gains in December and January. Other services are likely to pick up after a below trend 0.1% increase in March.