FX Daily Strategy: Asia, March 11th

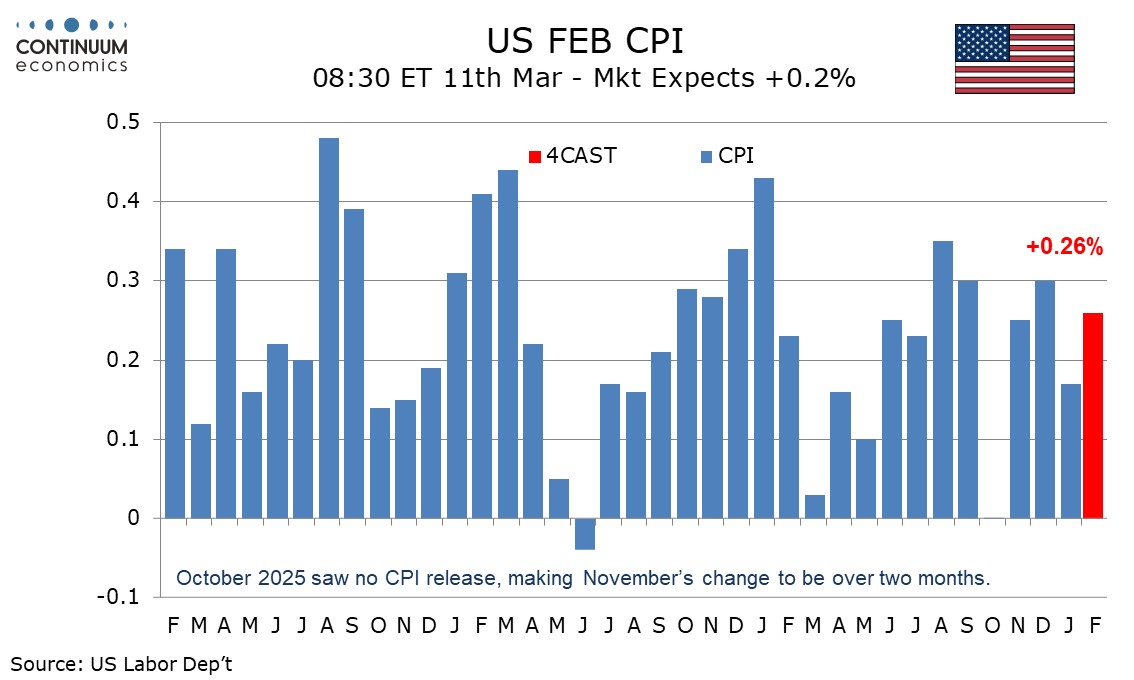

U.S. February CPI A moderate gain

Japan PPI Unlikely to Sway JPY

DXY Poised for further gains

We expect February’s CPI to increase by 0.3%, with a 0.2% increase ex food and energy. Before rounding we expect the gains will be similar, with the overall CPI rounded up from 0.26% and the core rounded down from 0.24%. CPI has slowed, but it is too soon for the Fed to declare victory. Gasoline prices fully reversed a January decline before seasonal adjustment, but after seasonal adjustment only a partial correction is likely. Gasoline prices look set for a stronger bounce in March in response to the situation in the Middle East. We expect food to remain subdued with a second straight rise of 0.2%. PPI food prices have lost momentum in recent months.

January’s core CPI increase of 0.3% was the strongest since August and with January having a tendency for volatility as new year pricing decisions are made, we would be surprised if February was quite as strong. Still, it is too early to declare inflation defeated with PCE prices having unusually exceeded the CPI in Q4 and core PPI having seen a strong gain in January. We do not expect a very soft February core CPI.

Japanese PPI will be released on Wednesday and should continue to show an uptrend. However, that does not mean direct support as PPI has been a poor translator to CPI. The input pressure is steady and could be in BoJ's mind, when they consider the overall inflationary picture.

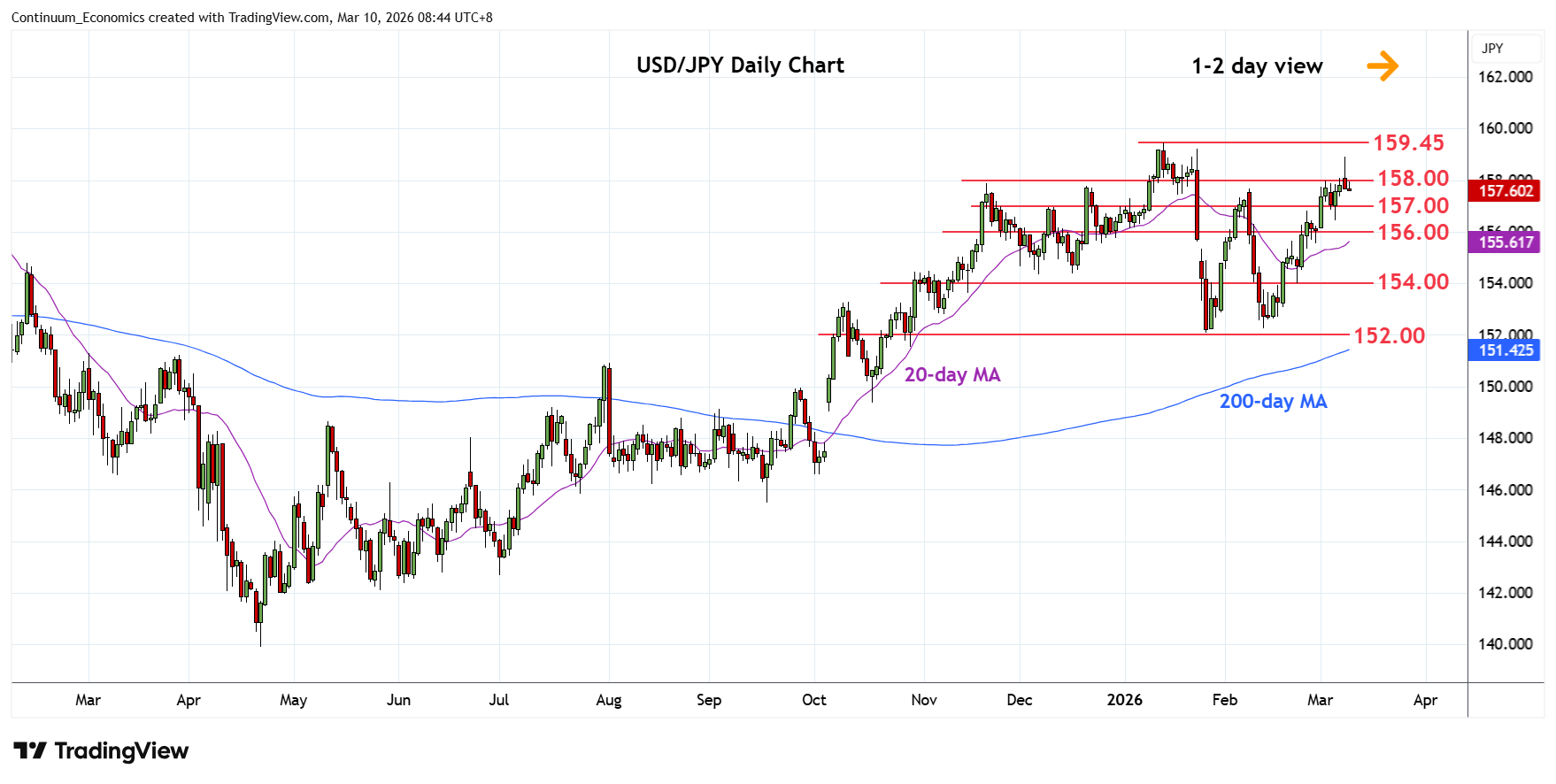

On the chart, USD/JPY has met with selling pressure beneath the 159.00 level and subsequent close below the 158.00 resistance fades the upside pressure as prices unwind overbought intraday studies. Daily studies are stretched as well and suggest scope for deeper pullback to retrace strong gains from the 152.27 February low and see room to support at the 157.00/156.45 area. Meanwhile, resistance is lowered to the 158.00 congestion which should cap and sustain rejection from the 158.90 high. Break needed to clear the way for retest of the 159.23/159.45, January highs.

Despite Trump being optimistic about the progress of Iran war, the geopolitical tension is unlikely to resolve anytime soon with Iranian choking the Strait of Hormuz. The oil market is on its edge with the black gold exploded higher to begin the week, indicating physical stress in the market. All of which will support the USD on haven bids.

On the chart, choppy trade around congestion support at 99.00 has given way to a sharp run higher to resistance at 99.50, where mixed/positive intraday studies are prompting short-term reactions. Daily readings are turning higher once again and broader weekly charts are positive, highlighting room for further strength in the coming sessions. A break above 99.50 will target the 99.68 current year high of 30 March. A further close above here will improve sentiment and extend late-January gains initially to congestion around 100.00. Meanwhile, any immediate tests beneath 99.00 should be limited in renewed buying interest/consolidation above congestion around 98.50.