FX Daily Strategy: Asia, March 10th

Japan GDP May Help the JPY a tad

Else, Geopolitical Tension Drives the DXY

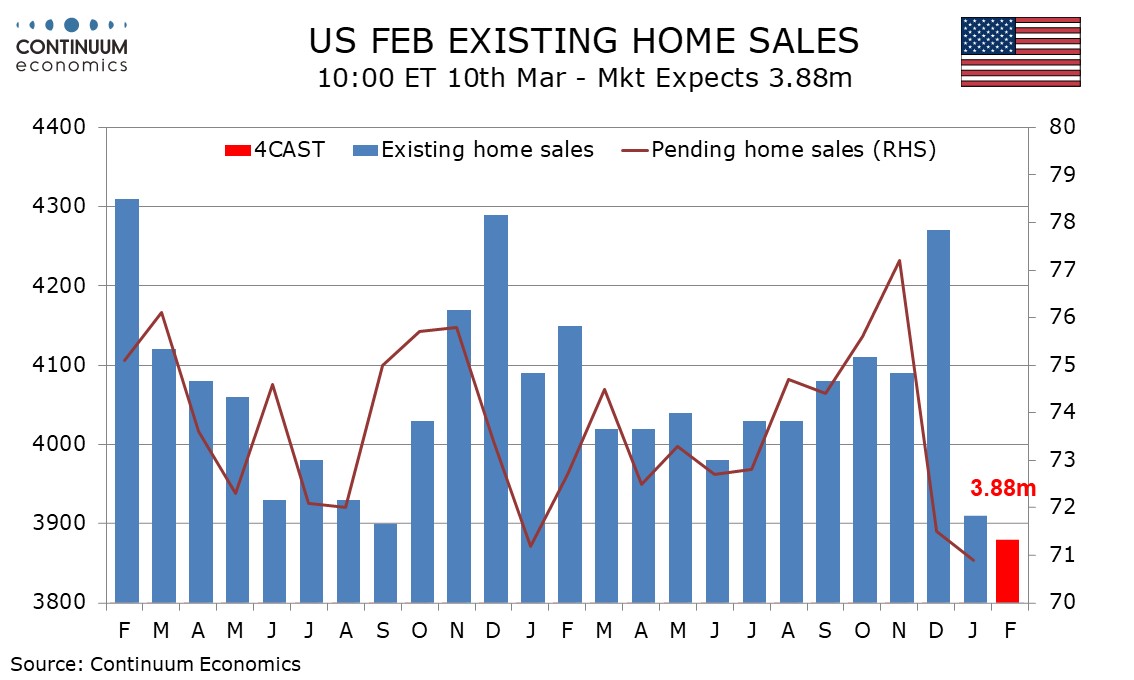

U.S. February Existing Home Sales Extending decline

The official Q4 GDP will be released on Tuesday's Asia session. Preliminary data has barely kept Japan in expansion and the official data could easy drag the figure into contraction if the revision is negative. So far, there has not been major revision in Q4 Japanese data in terms of spending while wage growth is revised slightly higher. There is a good chance the official release could see Japanese GDP further into expansion. A strong read could support the JPY a tad as it will not drag BoJ when they hike.

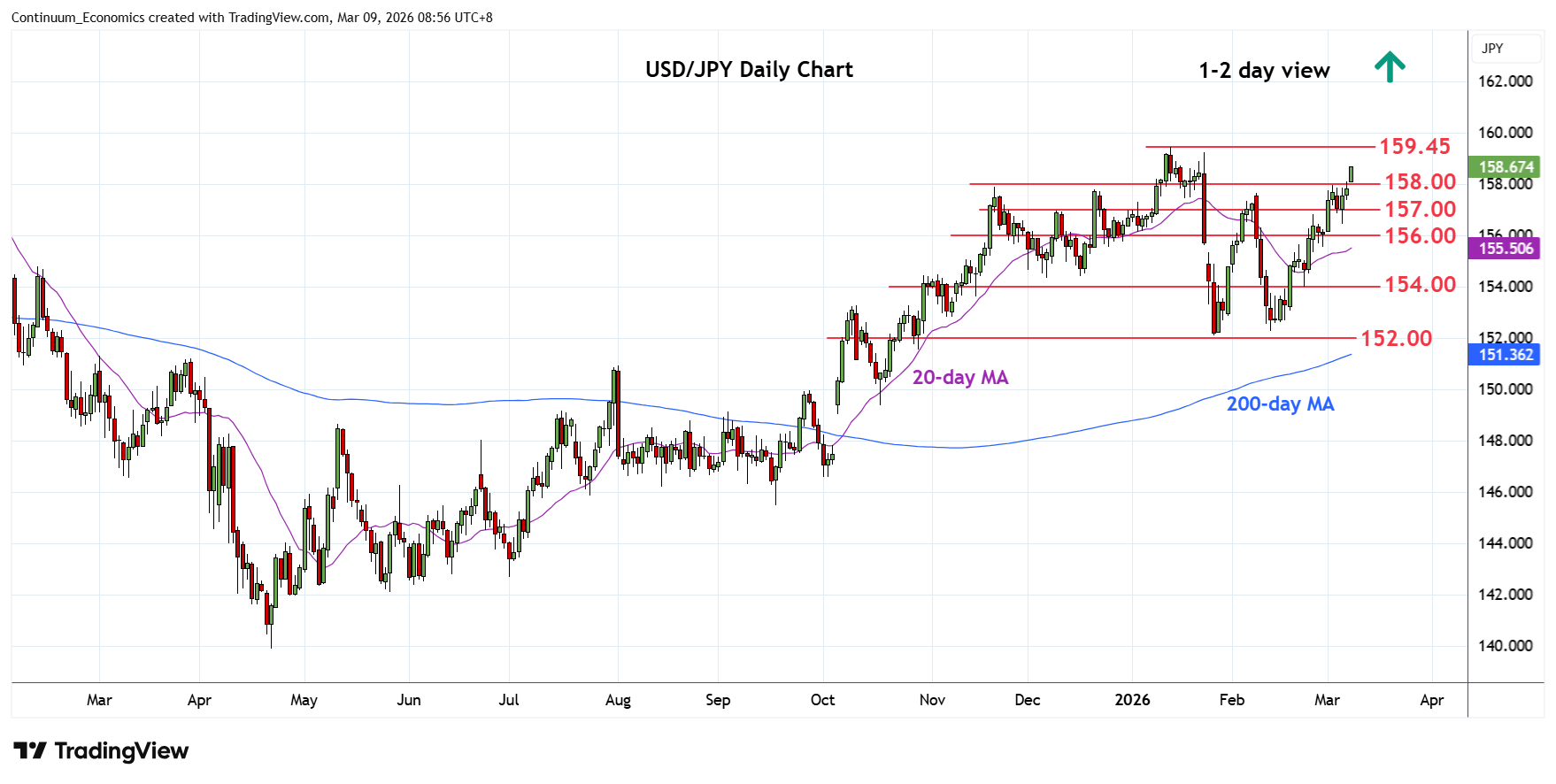

On the chart, the pair gapped up at the opening above the 158.00 level see prices extending gains from the 152.10 January low. Nearby see scope to target the 159.00 level but focus has turned to the 159.23/159.45, January highs. Break above these cannot be ruled out but the overbought daily and weekly chart caution corrective pullback with support starting at the 158.00/157.66 congestion and February high. Below this area will fade the upside pressure and open up room for deeper corrective pullback to the 157.00 level and 156.45/156.00 congestion area.

Geopolitics will remain in the spotlight. Both the U.S. and Iran have little signs of giving up and does not seem to de-escalate anytime soon. The key here is the physical disruption of around 20m barrel of oil flowing out of the Strait of Hormuz, which triggered an explosive rally in oil. If such is not resolved soon, the inflationary pressure will build up globally and indirectly lead to falling equities, which in turn lead to USD bids for haven purpose.

On the chart, choppy trade around congestion support at 99.00 has given way to a sharp run higher to resistance at 99.50, where mixed/positive intraday studies are prompting short-term reactions. Daily readings are turning higher once again and broader weekly charts are positive, highlighting room for further strength in the coming sessions. A break above 99.50 will target the 99.68 current year high of 30 March. A further close above here will improve sentiment and extend late-January gains initially to congestion around 100.00. Meanwhile, any immediate tests beneath 99.00 should be limited in renewed buying interest/consolidation above congestion around 98.50.

We expect February existing home sales to fall by 0.8% to extend a sharp 8.4% January decline, to a level of 3.88m, which would be the lowest since October 2010. This would follow a 0.8% decline in January pending home sales, which extended a sharp 7.4% December decline. The NAHB homebuilders’ index, which had been trending higher through December, slipped in January and February. Fading hopes for near term Fed easing may have contributed to the slippage. Bad weather may be a factor restraining February sales, particularly in the Northeast. We expect February to see declines in three of the four regions, the exception being the West which has scope for a correction from a particularly steep January decline.