FX Daily Strategy: APAC, October 30th

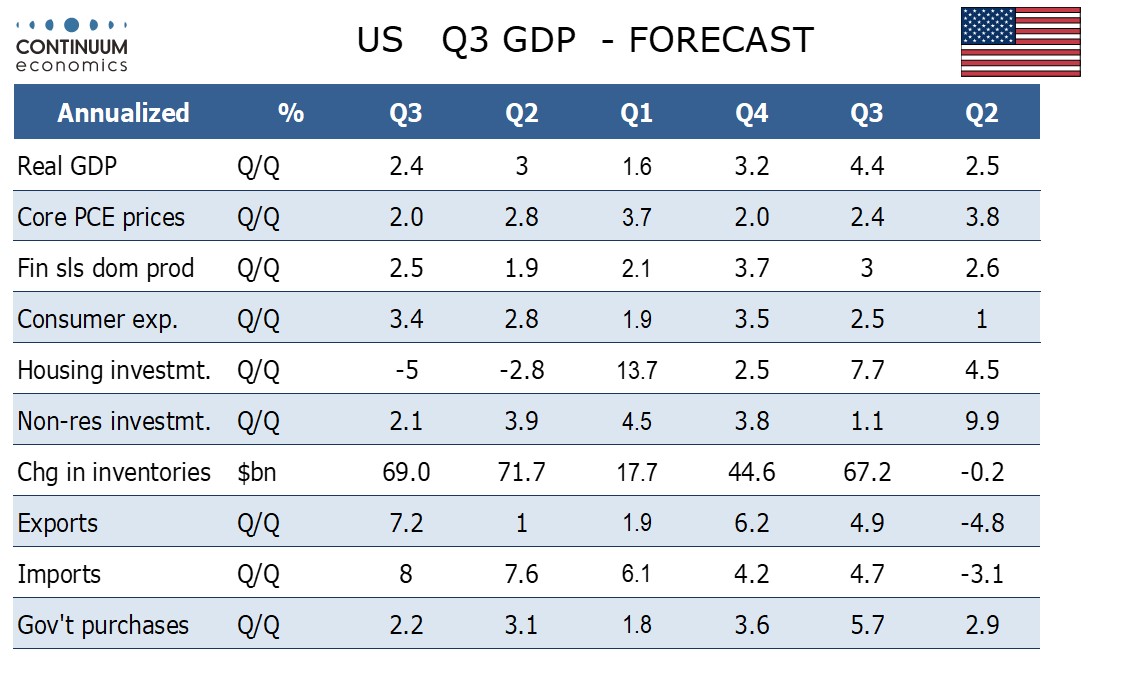

US GDP may weigh on the USD after recent gains

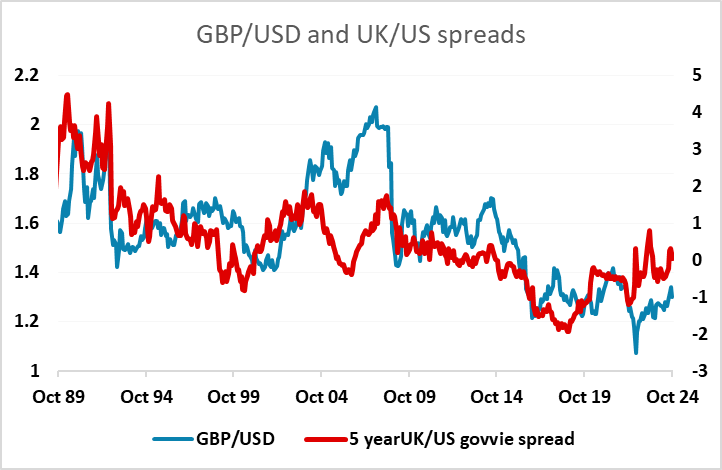

GBP might benefit from UK budget

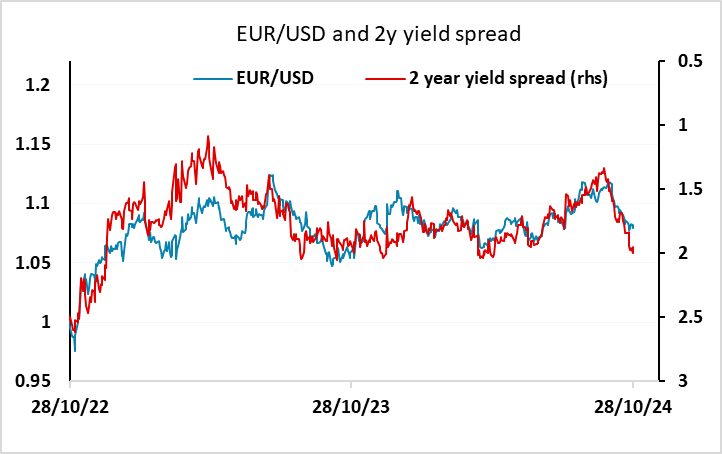

EUR downside risks on GDP

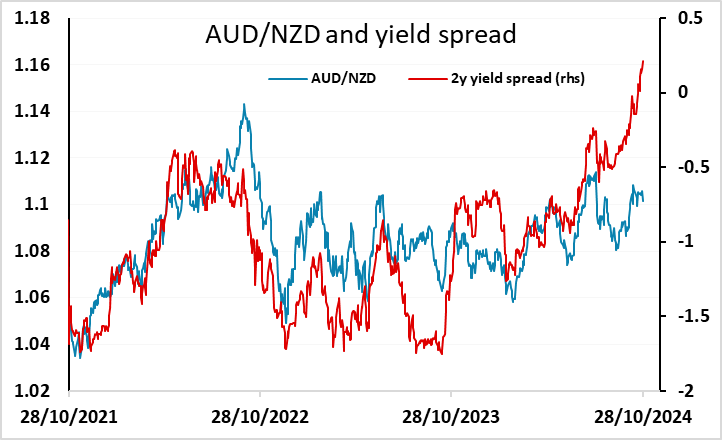

AUD looks undervalued, particularly versus NZD

US GDP may weigh on the USD after recent gains

GBP might benefit from UK budget

EUR downside risks on GDP

AUD looks undervalued, particularly versus NZD

After a quiet start to the week, Wednesday has a plethora of data releases, with then highlight being the US Q3 GDP data, as well as the UK budget statement. We expect a 2.4% annualized increase in US Q3 GDP, slower than Q2’s 3.0% but still maintaining solid momentum. Q3’s gain will be led by consumer spending, with a slowing in core PCE prices to an on-target 2.0% annualized after gains of 2.8% in Q2 and 3.7% in Q1. Our forecast is on the soft side of market expectations, with consensus at 3.0%b annualised, so there might be some USD negative impact, especially since the short term market is long USD after the gains of the last few weeks. USD/JPY positioning is likely to be the most vulnerable given the JPY’s recent weakness.

For the UK the key event is the Budget and Spending Review. With speculation that the Chancellor faces a £ 40 bln funding gap which will be addressed largely through tax rises, it seems as if the UK economy faces a larger fiscal tightening than was planned under the previous government. However, it seems likely that the Budget measures will actually be less restrictive as the government looks set to change the fiscal rules to allow more investment. This should therefore reinforce the Office for Budget Responsibility’s already relatively upbeat growth outlook. However, the impact on GBP is hard to predict. We tend to favour the upside because GBP retain some risk premium from the 2022 Truss budget, with GBP trading lower than the historic correlation with yield spreads would suggest ever since (despite some recovery). If the budget is seen as responsible but also offering the chance of growth recovery in the longer run, the pound might react positively.

Before the US data there is provisional CPI data in Europe from Spain and Germany, and also provisional Q3 GDP data from the Eurozone. At best, the EZ economy is diverging ever more clearly as Germany falters while Spain prospers. However, the risks are that the whole of the EZ is weakening. Indeed, in contrast to ECB and consensus thinking of a second successive quarter of 0.2% q/q GDP growth, we see a clear risk that the EZ economy failed to grow in Q3. This would suggest downside risk for the EUR, which is already at risk due to the movement of yield spreads in the USD’s favour. Thus far, support at 1.0750 has held, but spreads suggest downside risks and weak GDP data could push the EUR over the edge. The risks for the CPI data may be on the upside for Germany due to energy-related base effects, but the GDP data is likely to be more of a focus.

Ahead of all this there is Australian CPI. The AUD looks extremely cheap relative to recent yield spread moves, both against the USD and the NZD. The weakness against the USD may relate to sentiment over the election and worries about tariffs on China, but it is harder to justify the weakness against the NZD on this basis. Whatever the CPI data is, AUD/NZD looks cheap.