FX Daily Strategy: N America, July 31st

BoJ kept rates on hold as expected

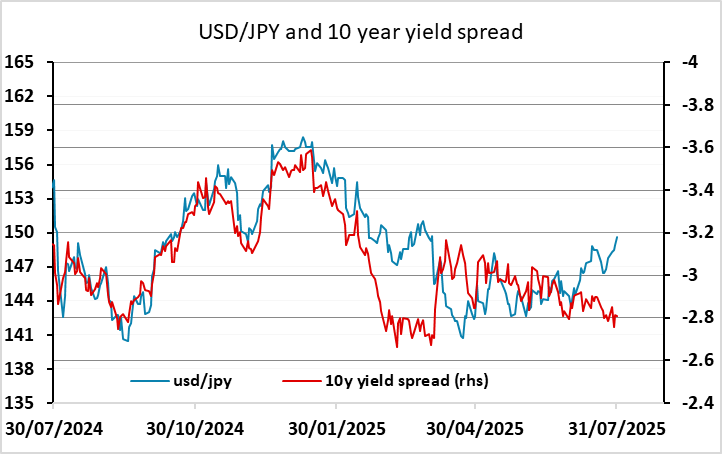

JPY upside favoured as equities edge lower

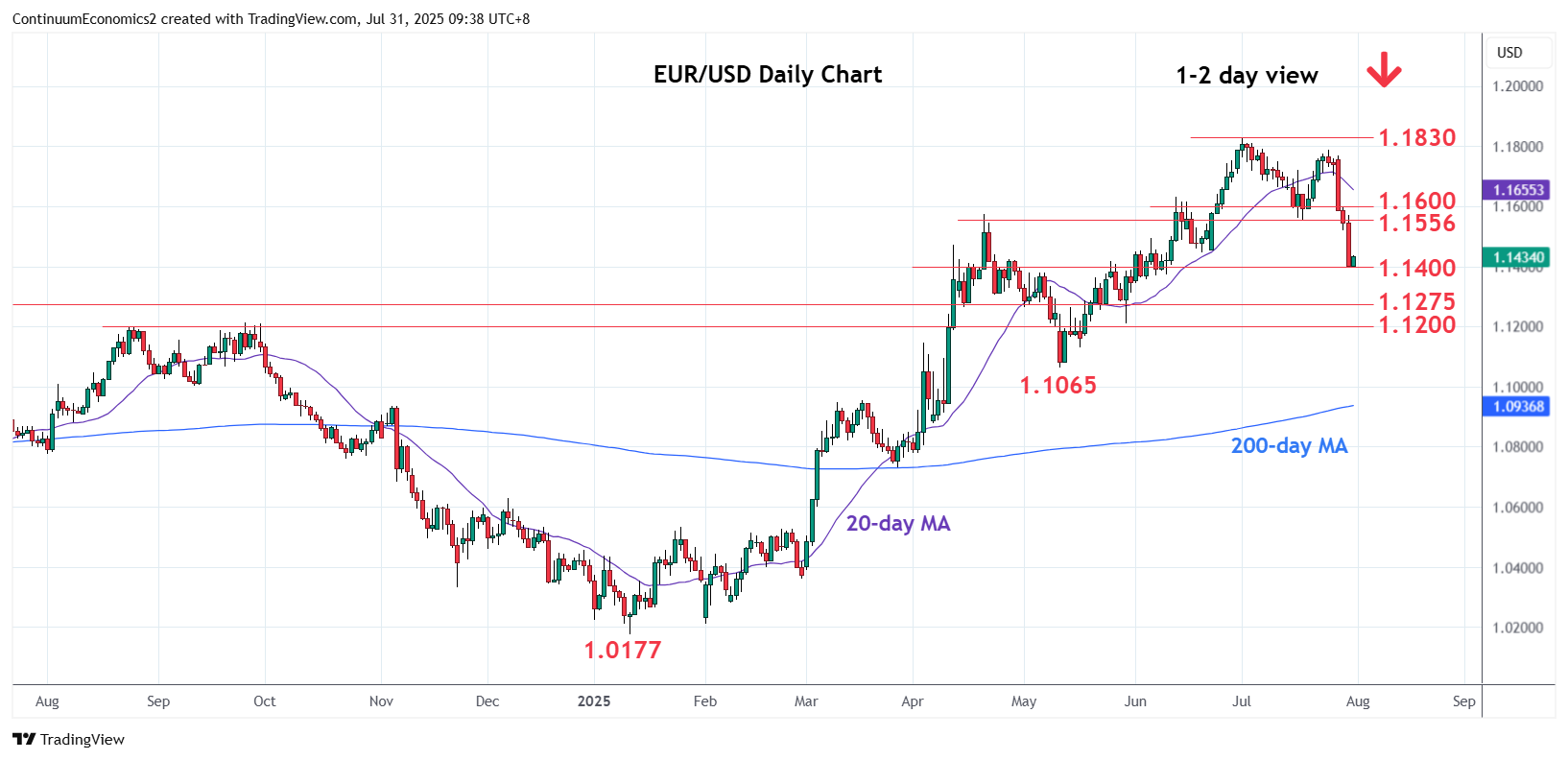

EUR still has potential to correct lower

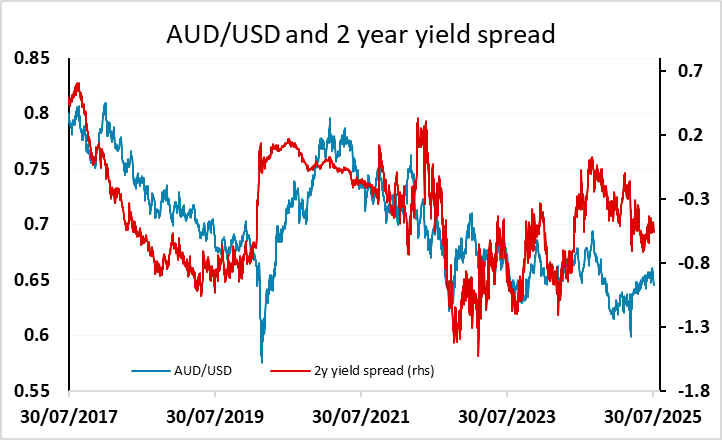

AUD weakness should fade as we approach 0.6400

BoJ kept rates on hold as expected

JPY upside favoured as equities edge lower

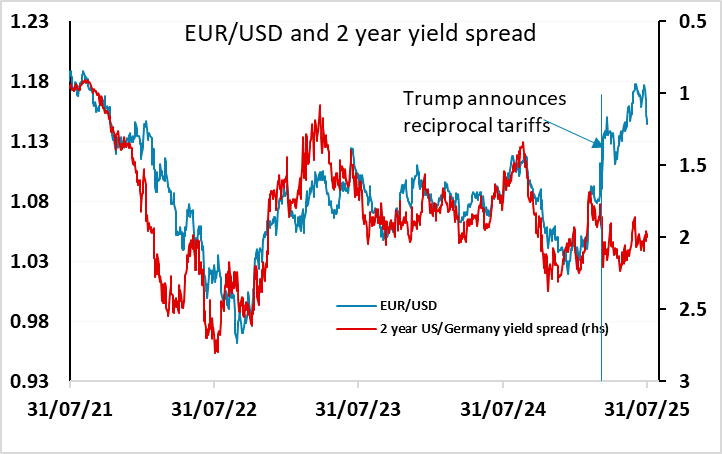

EUR still has potential to correct lower

AUD weakness should fade as we approach 0.6400

The BoJ meeting is the most significant event for Thursday. While no-one expected any change in policy, it’s clear that Ueda wants to raise rates at some point if the economy allows it, and the trade deal with then US reduces uncertainty and brings a rate hike closer. However, his comments suggests that he doesnt anticipate enough strength in real wages until near the end of the year to justify a rate hike. The JPY has risen as a result, with the market slightly reducing earlier rate hike expectations.

As it stands, USD/JPY has been rising on the back of the general USD recovery on the trade deals, but the case for USD/JPY gains is far weaker than the case for a EUR/USD decline. While the USD suffered against the EUR after the April tariff announcement, substantially underperforming the usual yield spread relationship, the USD has outperformed yield spreads against the JPY. Much of this is due to the resilience of equity markets, with the JPY still suffering on the crosses when risk premia decline. The strength of equities overnight on Meta and Microsoft results has put further pressure on the JPY.

Otherwise we have preliminary CPI data from France, Italy and Germany, which have come in slightly on the strong side of consensus. This won’t have much impact on the EUR, which has continued to struggle against the backlash from the EU/US trade deal. The positive USD reaction to the deal has to be seen in the context of the USD decline after the initial tariff announcement in April, and while many are seeing it as a reflection of the favourable terms for the US, we believe it should be seen more as a relief that the tariffs weren’t higher and should consequently not be too damaging to the US economy. There is still scope for further declines in EUR/USD retracing the gains form April, with EUR/USD starting from around 1.09 before the tariff announcement, but there should be support in the 1.1400/50 area.

The USD has been the weakest currency in the last couple of days, with the general USD recovery, the turn slightly lower in equities and the softer CPI data from Australia all weighing. Yield spread support for the AUD has diminished in recent weeks, but AUD/USD still looks good long term value and we would expect good support to emerge before the key 0.6400 level