FX Daily Strategy: Asia, April 28th

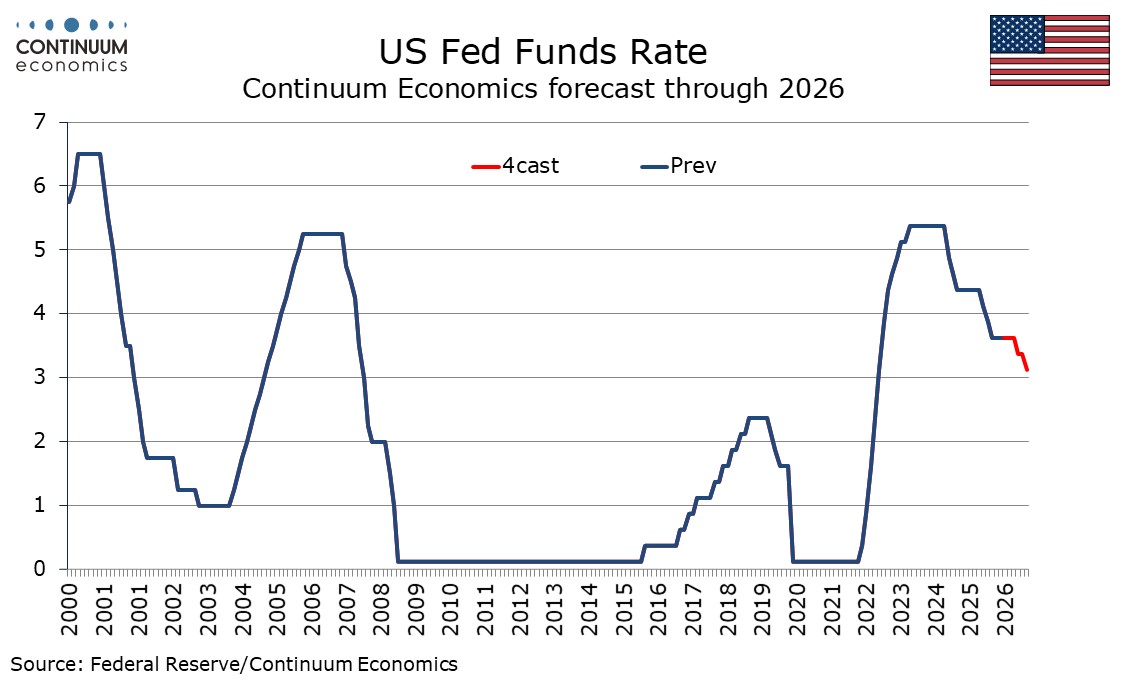

Uncertainty keeping the Fed on hold

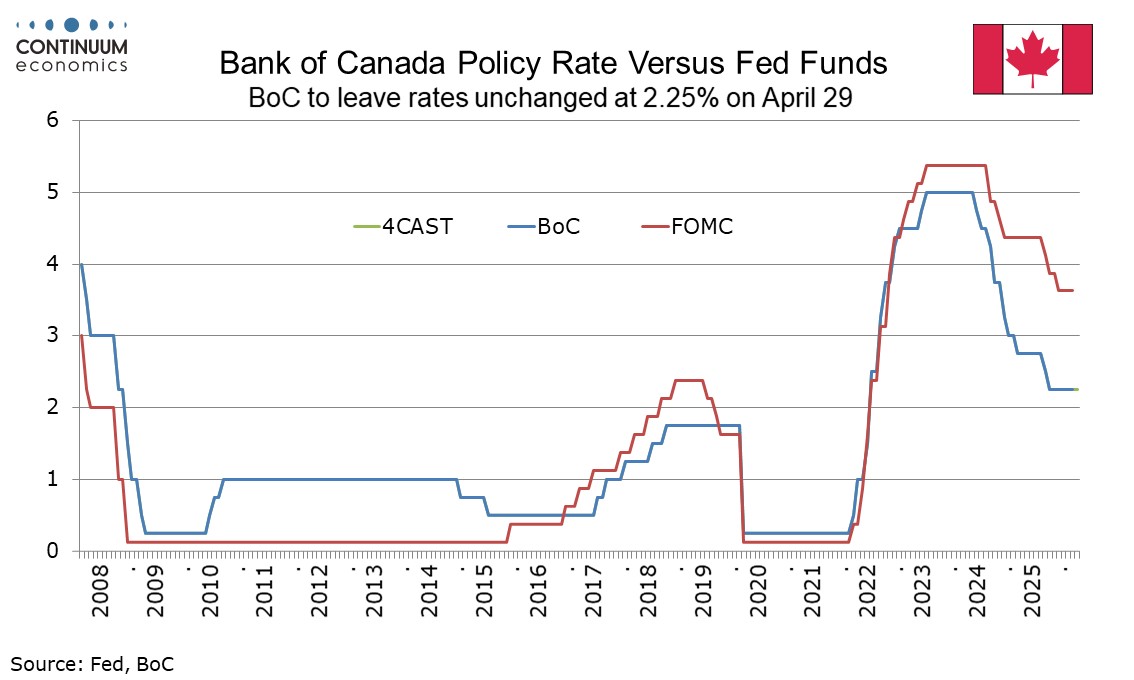

Bank of Canada No hawkish shift from energy price shock

A Slate of U.S. Data

The FOMC meets on April 29 and there is little risk of a change in rates from the current target range of 3.5-3.75%. High uncertainty, both on the geopolitical situation and the future of the Fed, suggests there will be little forward guidance, and the dots will not be updated until the next meeting on June 17. If there is a shift in tone it is more likely to be in a hawkish direction, but few appear to be considering a near term tightening, and we still expect the next move is more likely to be an ease.

There does not appear to be any pressing need for the FOMC to alter its statement from the last one on March 16, which saw the economy expanding at a solid pace. Q1 GDP data due on April 30 is likely to confirm this (we expect a 2.6% annualized increase). The statement went on to say that job gains have remained low and the unemployment rate has been little changed in recent months. That also remains the case, but a stronger March non-farm payroll suggests any fine tuning to the view will be positive. Inflation was described as somewhat elevated. With core PCE prices looking firm in Q1 (we expect a 4.1% annualized increase) and energy prices having surged, the Fed may say a little more on inflation this time.

The Bank of Canada meets on April 29 and looks set to leave rates unchanged at 2.25%. A quarterly Monetary Policy Report is due but given uncertainty the BoC may deliver a range of scenarios rather than an updated forecast. Despite the upside risks to overall inflation, recent subdued economic activity and core inflation data suggests the BoC will not delver a more hawkish tone.

In its last Monetary Policy Report in January the BoC looked for 1.8% annualized GDP growth in Q1. The statement at the last meeting on March 18 suggested near term growth would be weaker than expected in January, though we do not expect a sharp underperformance of the BoC’s forecast. Q4 GDP at -0.6% annualized was weaker than a flat BoC projection but the BoC in March noted this was largely on an inventory drawdown. The March statement also noted weak January and February employment data, which was followed by only a marginal correction higher in March. We expect the BoC will look for a subdued Q2 GDP gain of around 1.0% but its January forecast of 1.4% Q4/Q4 does not appear to require a significant downgrade. The growth implications of the energy shock are mixed for Canada, with the energy sector likely to see a boost.

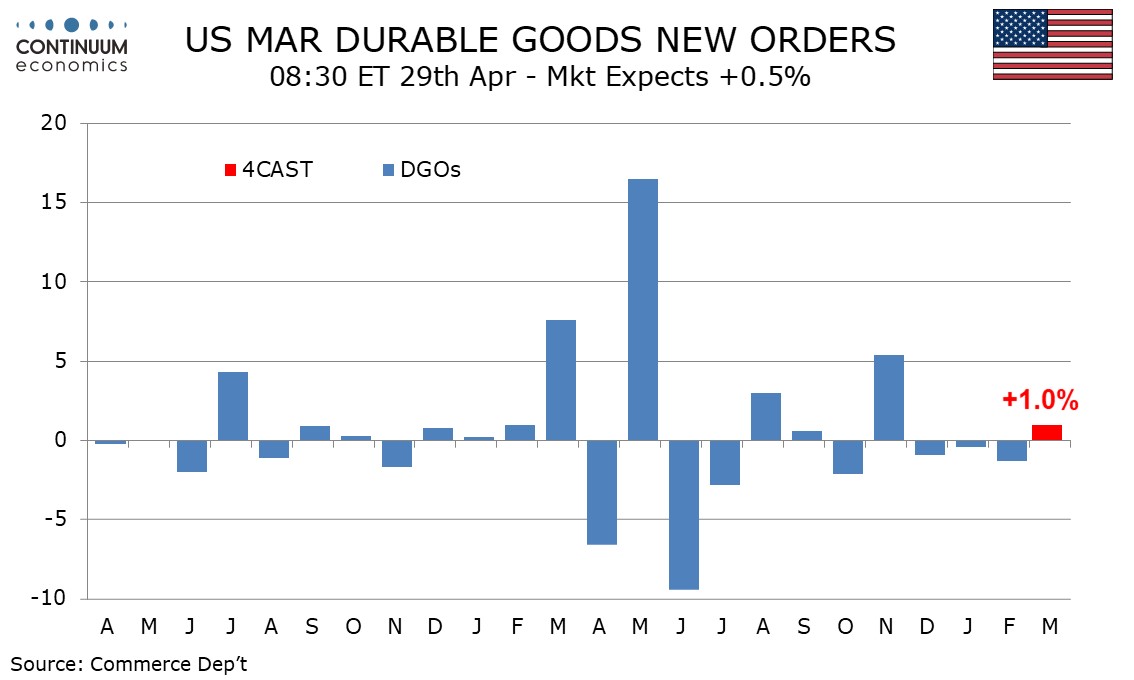

We expect March durable goods orders to increase by 1.0% overall, with a 0.4% increase ex transport, with most of the transport increase coming in defense. Ex transport trend will remain positive, but a 0.4% increase would be slightly below recent trend. We expect a 0.5% increase ex defense. There are upside risks in defense after two straight declines and the outbreak of war in the Middle East. Transport has a large overlap with defense. Boeing data suggests only a marginal rise in civil aircraft, often a source of volatility while autos are at risk of a correction from a strong February gain.

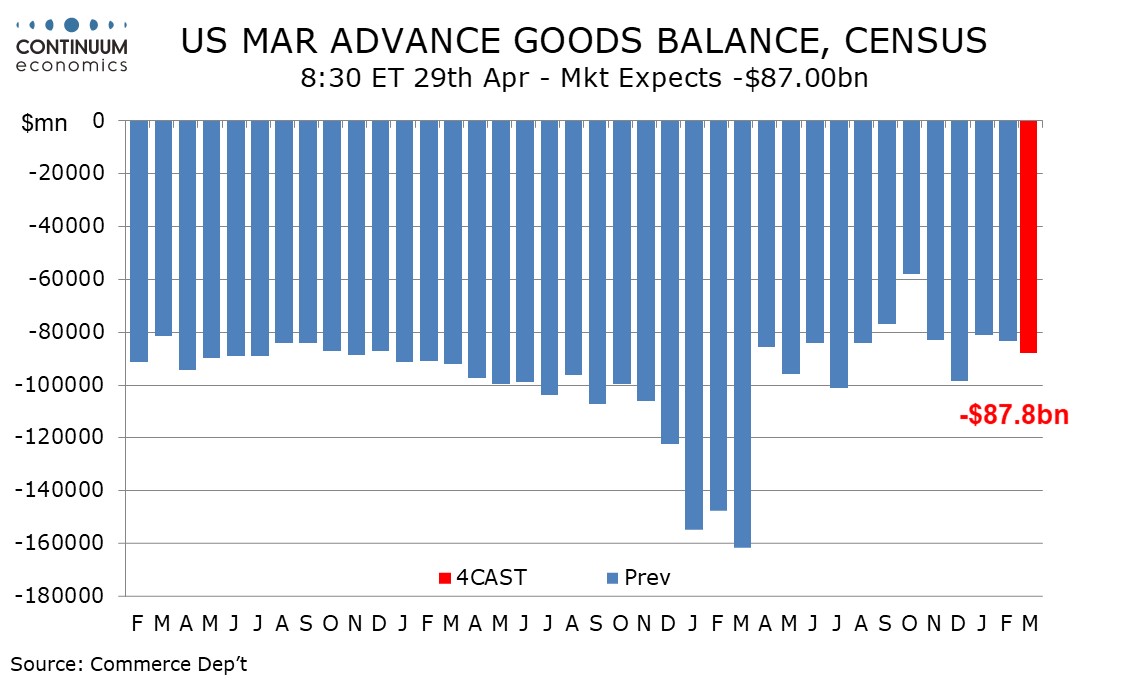

Trade data has been volatile recently and advance goods data could have an impact on Q1 GDP expectations, with GDP data due on April 30. We expect a deficit of $87.8bn, up from $83.5bn in February and $80.9bn in January. The Q1 deficit would then average $84.1bn, compared with $79.8bn in Q4, but still below where trend was before tariff policy increased the volatility of the series, marginally below $100bn per month. We expect exports to fall by 3.5% after a 5.9% February increase and imports to fall by 1.0% after a 5.1% February increase. This will be despite export prices increasing by more than imports prices.

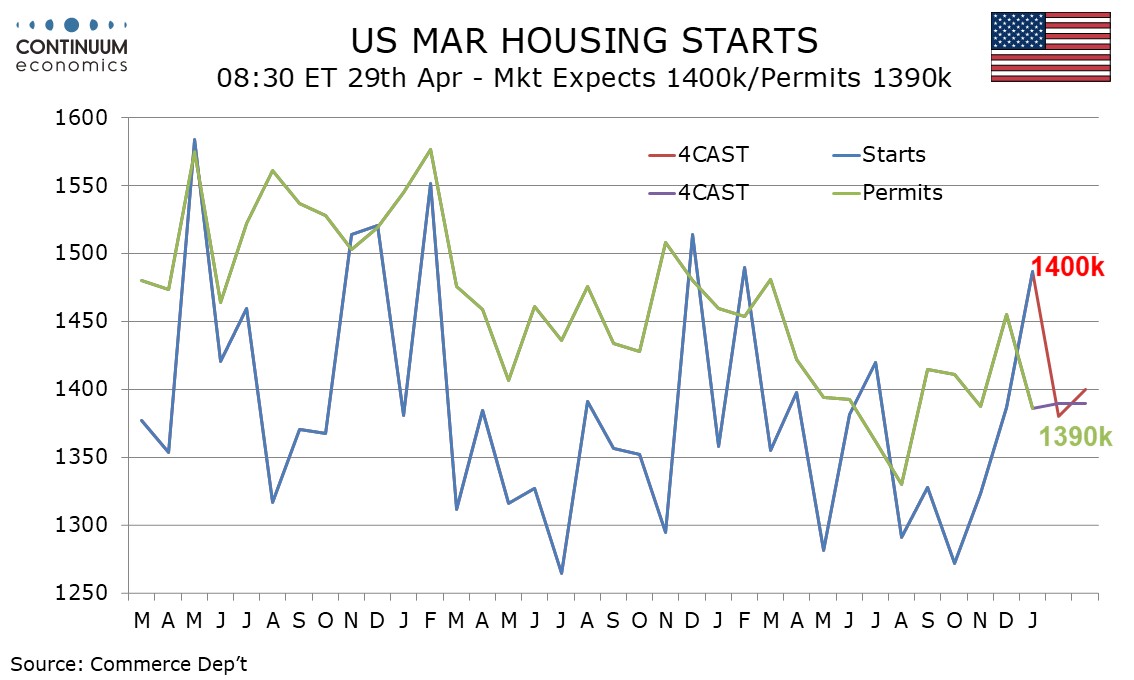

Housing starts and permits data for both February and March will be released on April 29. We expect a fairly flat housing market picture to emerge, with starts falling by 7.2% in February to 1380k after a 7.2% January increase, followed by a 1.4% rise to 1400k in March. We expect permits to rise by 0.3% in February to 1390k, and to remain at that level in March. Most housing sector indicators have little clear direction, though signs of improvement in late 2025 have faded alongside fading hopes for further near term Fed easing. Weather is likely to be more supportive in March than February so we expect starts to be firmer in that month, though weather is likely to have less impact on permits.