FX Daily Strategy: Asia, March 24th

Will Trump TACO

Going to Be Swaying DXY

U.S. March S&P PMIs Likely Meaningless for Market

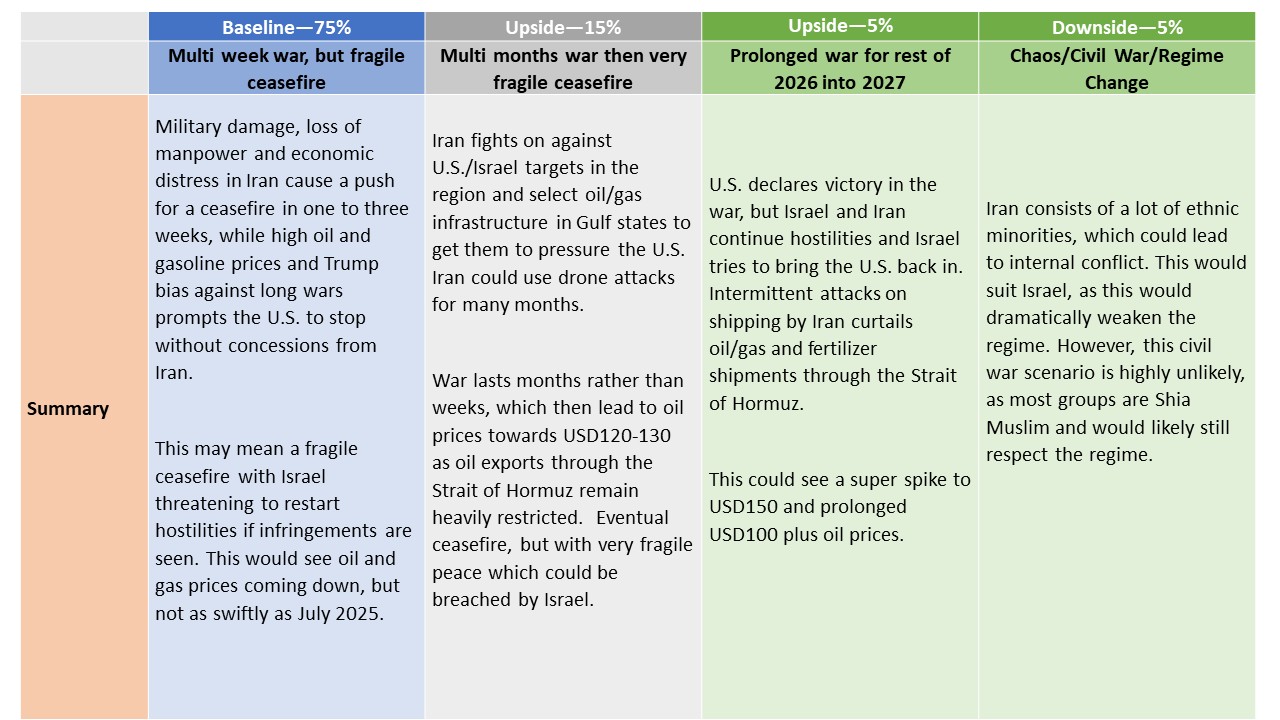

Our central scenario (75%) remains a multi-week war in Iran. Trump loathing of long wars and high gasoline prices prompts U.S. to declare victory before end of March. Israel and Iran would most likely agree an effective ceasefire. The ceasefire would be fragile, however, as it would likely not involve concessions from Iran’s new hard-line leader, while potential Israeli hostilities could breach the ceasefire. We would see WTI at USD80-85 by April and USD70-75 by June. The main alternative scenario is a multi-month war (15%), which could squeeze oil prices up to USD120-130.

The key question here remains whether Trump will "TACO" or not. Trump's threat of destroying Iranian electricity plant will likely bring scotch earth for Gulf Allies. Such is unlikely to be desirable for Trump and his Gulf Allies as we already heard from Qatar that they openly suggesting the war needs to stop after suffering massive damage. It remains uncertain whether Trump is willing to sacrifice allies and U.S. asset to achieve his expected results.

DXY will be dominating the FX market, which in turn was just by Trump's decision. The greenback has been a go to haven asset for long after geopolitical tension arises and past year of risk aversion events. However, with U.S. and allies asset being targeted, market participants may rotate out of USD to other haven currencies, likely JPY.

On the chart, cautious trade around 100.00 has given way to a sharp fall, with steady selling interest reaching congestion support at 99.00 before settling into consolidation within the 99.00 - 99.50 range. Daily readings have turned down, highlighting room for continuation beneath 99.00. But rising weekly charts should limit initial scope in short-covering/consolidation towards strong support within further congestion around 98.50 and the 98.65 Fibonacci retracement. Meanwhile, resistance is lowered to congestion around 99.50. A close above here, if seen, would help to stabilise sentiment and prompt consolidation beneath further congestion around 100.00.

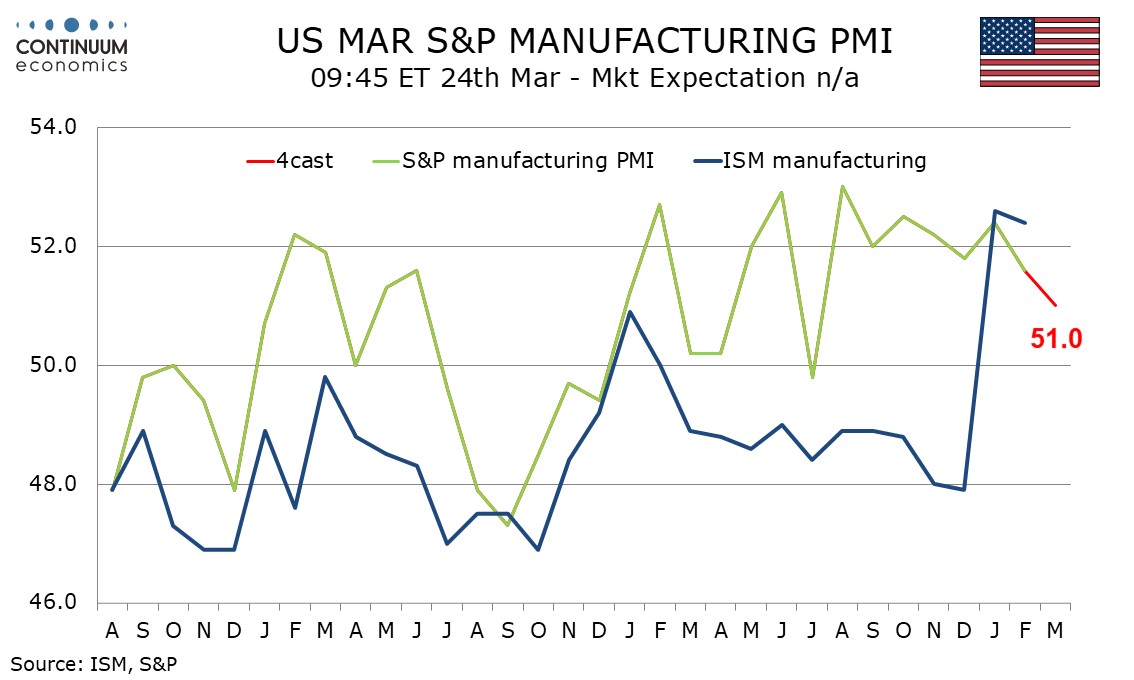

We expect slippage in March’s S&P PMIs, with manufacturing and services both falling to a marginally positive 51.0, from 51.6 and 51.7 respectively in February. The S&P manufacturing index was positive through most of 2025 but may now be peaking. The situation in the Middle East is a downside risk though signals are mixed, with the Empire State index slipping in March but the Philly Fed’s increasingly strong. January and February both saw preliminary indices weaker than the final, which also hints at downside risk for preliminary March data. The S&P services index probably sees more risk than manufacturing from the situation in the Middle East, with consumers vulnerable. However with February’s index at a 10-month low, well below the ISM services index, there may be only modest downside scope in March, and we do not expect a negative outcome.