CBR Cuts Key Rate by 50 Bps to 15% Despite Risks

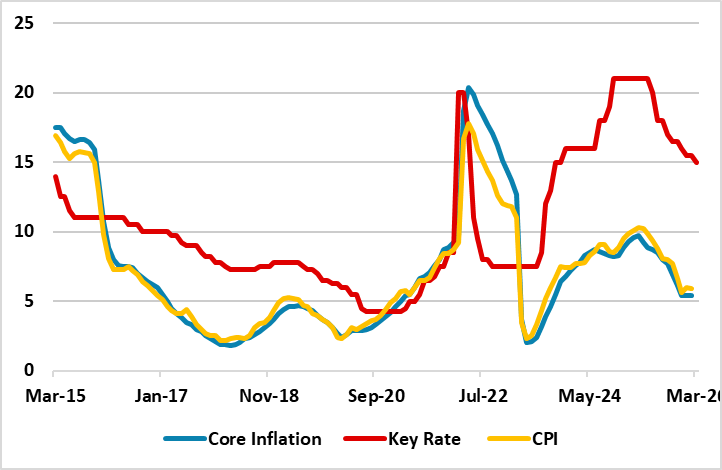

Bottom Line: Despite adverse global developments and proinflationary risks, the Central Bank of Russia (CBR) reduced the policy rate by 50 bps to 15% on March 20 likely to stimulate the economy as it comes under increasing strain from high borrowing costs. CBR noted in its written statement that it may not extend the cutting cycle due to higher energy prices following the outbreak of war in the Middle East. Our year-end target for the 2026 key rate remains 13%.

Figure 1: CPI, Core Inflation (YoY, % Change) and Policy Rate (%), January 2015 – March 2026

Source: Continuum Economics

Despite mounting inflationary risks and elevated inflation expectations coupled with adverse global developments, the Central Bank of Russia (CBR) reduced the policy rate for a second straight meeting by 50 bps to 15% on March 20 likely to stimulate the economy as it comes under increasing strain from high borrowing costs.

CBR noted in its written statement that it may reduce borrowing costs further as the economy approaches a balanced growth path depending on the sustainability of the inflation slowdown. Additionally, CBR governor Nabiullina said on March 20 that the resulting effect of Iran conflict on the Russian economy will depend on the duration and scale of these geopolitical events, noting that higher prices on crude oil and other exports from Russia would support the ruble. “In the long run, the situation in the Middle East might adversely affect both global demand and investment growth prospects, accelerate inflation in economies importing energy commodities, and disrupt supply chains,” Nabiullina warned.

We believe high domestic gas and oil production will curtail domestic energy prices in contrast to global energy prices. Higher global oil prices in Q2/Q3 and temporary sanctions relief due to the Iran conflict could boost Russia crude exports help relieve fiscal pressures, and stimulate growth. (Note: Higher oil revenues may facilitate expanded military spending, potentially triggering demand-pull inflation. Conversely, they could moderately decelerate inflation via the FX channel, although the impact of sanctions would likely limit this effect. We expect the net result to be a secondary rather than a dominant factor).

The regulator mentioned in its statement on March 20 that it expects annual inflation to fall to 4.5-5.5% in 2026 and to reach its 4% target next year. (Note: Our projection for average headline inflation in 2026 remains at 5.9% in our March outlook). We believe achieving 4.5-5.5% target band in 2026 will be challenging since the disinflationary process will take longer than the CBR anticipates due to the persistent impact of sanctions, continued high levels of military spending, energy shocks and tightening labor market conditions. Consequently, we expect monetary policy to remain restrictive for an extended period. Our year-end target for the 2026 key rate remains 13%. High real yields will be necessary to manage stubborn inflation and we anticipate these inflationary headwinds will persist for the duration of the war in Ukraine and Iran conflict.