FX Weekly Strategy: Asia, March 2nd-6th

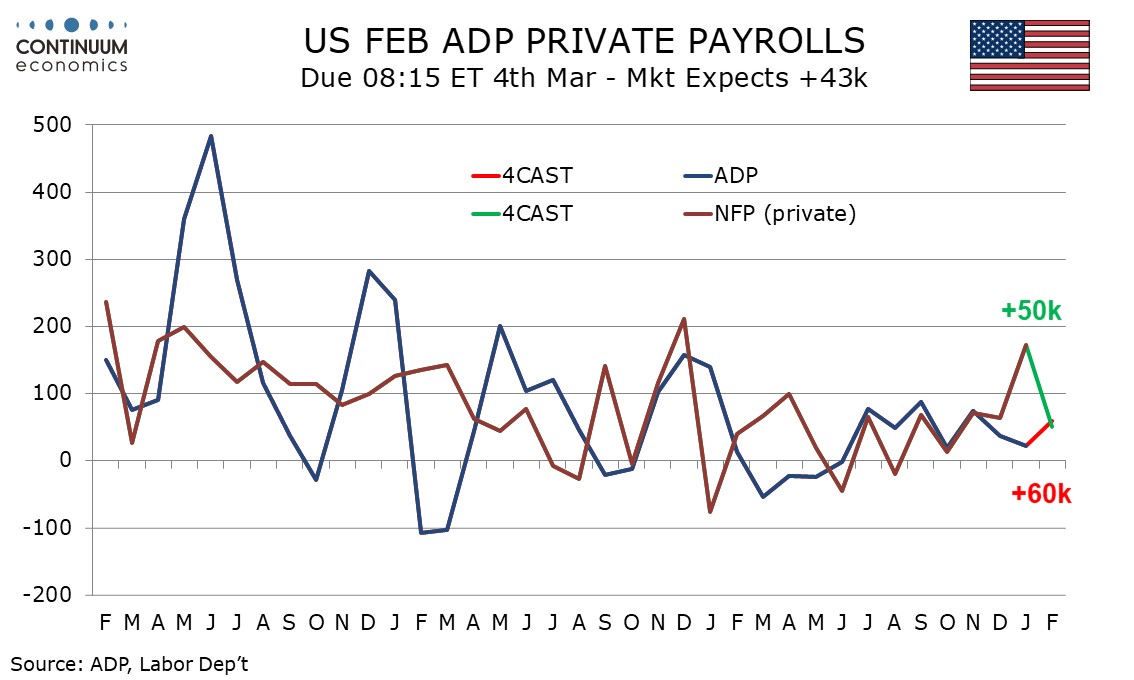

U.S. February ADP Employment to pick up

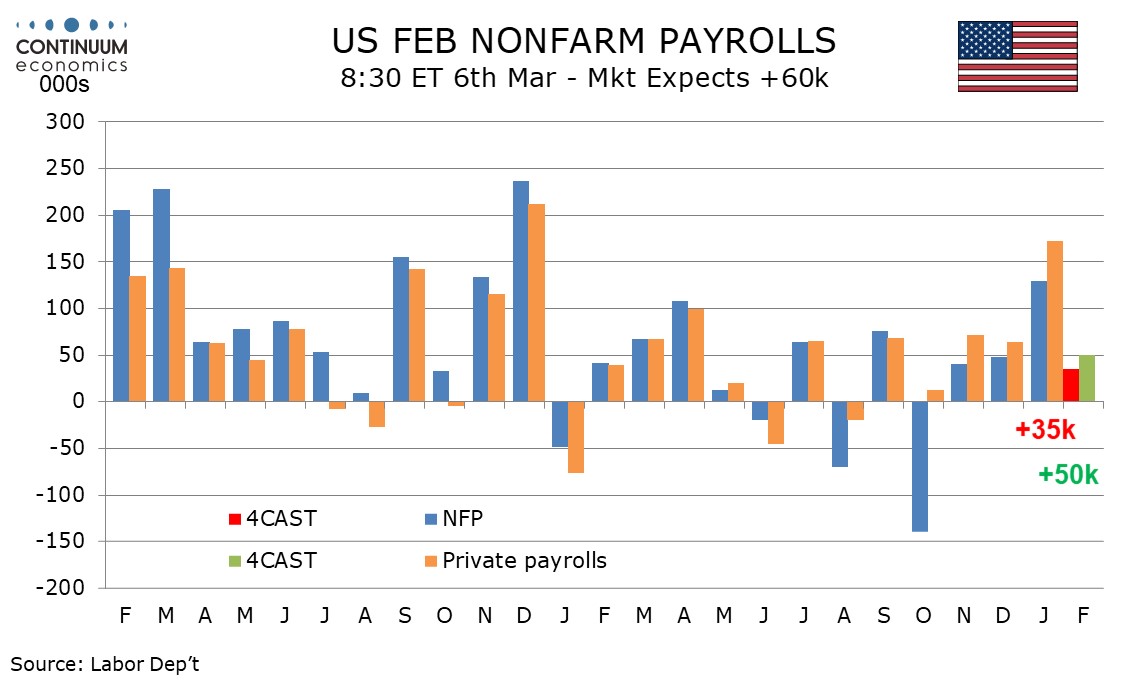

U.S. February Non-Farm Payrolls Not as strong as January

And Other U.S. Data

ECB Too Focused on Services Inflation

We expect a 60k increase in February’s ADP estimate for private sector employment, which would be a significant pick up from January’s 22k, which dramatically underperformed a 172k increase in January’s private sector non-farm payroll. We expect February’s ADP report to marginally outperform a 50k increase in private sector non-farm payrolls, while we expect overall non-farm payrolls to increase by only 35k. Bad weather in late January and early February may impact payrolls more than the ADP data, which tends to be less weather-sensitive than payrolls. Weekly ADP data shows a 4-week average of 12.75k in the for weeks to February 7. The 4-week average may pick up in the week to February 14, given a fall in initial, claims in that week, the survey week for the monthly report. That would be consistent with a monthly ADP gain of 60k.

We expect February’s non-farm payroll to rise by 35k overall and by 50k in the private sector, both four month lows and significantly slower than January’s above trend respective gains of 130k and 172k. We expect unemployment to edge up to 4.4% from 4.3%, reversing a January dip, and average hourly earnings to rise by 0.3%, in line with trend. January’s strength was led by health care, which increased by 123.5k, and a significant slowing is likely in February, though the sector is still likely to fully explain February’s payroll gain, and most of that in the private sector. Revisions tend to be negative and January data may be revised lower, though probably only by around 25k, leaving the month still well above the late 2024 trend.

January’s data was supported by strongly positive seasonal adjustments, which turn negative in February. January’s data was also surveyed before some bad weather in late January, which would weigh on February data, though initial claims were back to normal in February’s payroll survey week after a bounce during the cold weather spell. A clearly negative payroll looks unlikely.

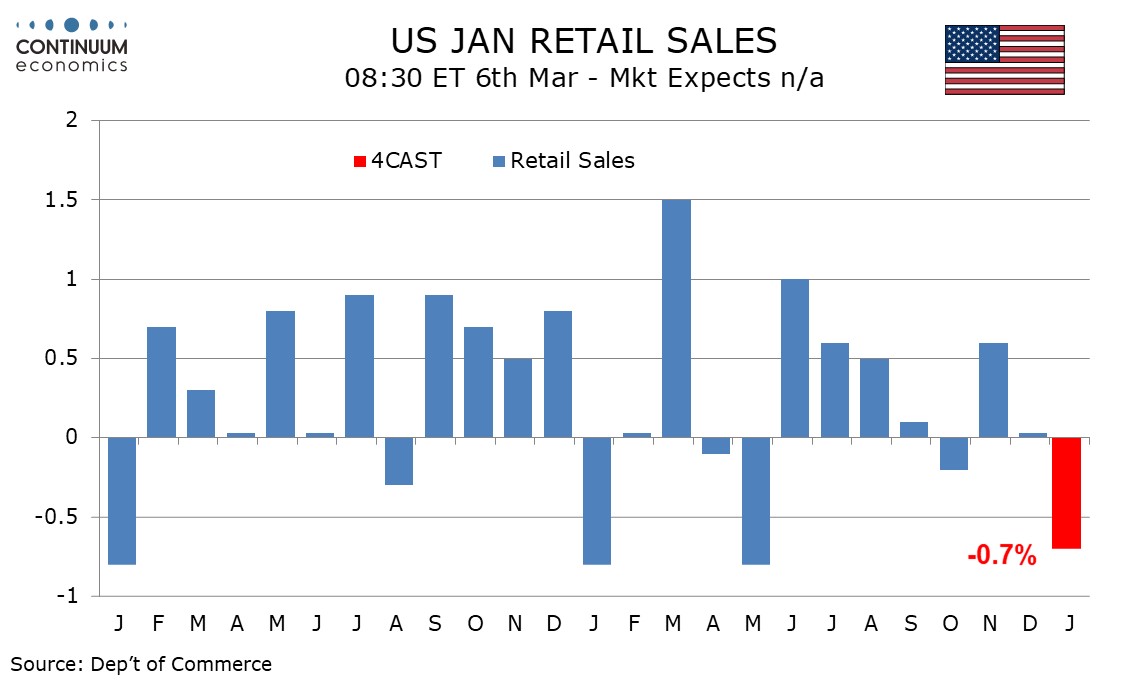

We expect retail sales to see a weak month in January, falling by 0.7% overall, with declines of 0.4% ex auto and 0.2% ex auto and gasoline. Bad weather late in the month will contribute to the decline. Industry data shows a significant dip in auto sales while CPI showed a decline in gasoline prices in January. Weather is not the only downside risk. Consumer spending ran well ahead of near flat real disposable income in both Q3 and Q4, suggesting that a loss of momentum in December retail sales may continue in January.

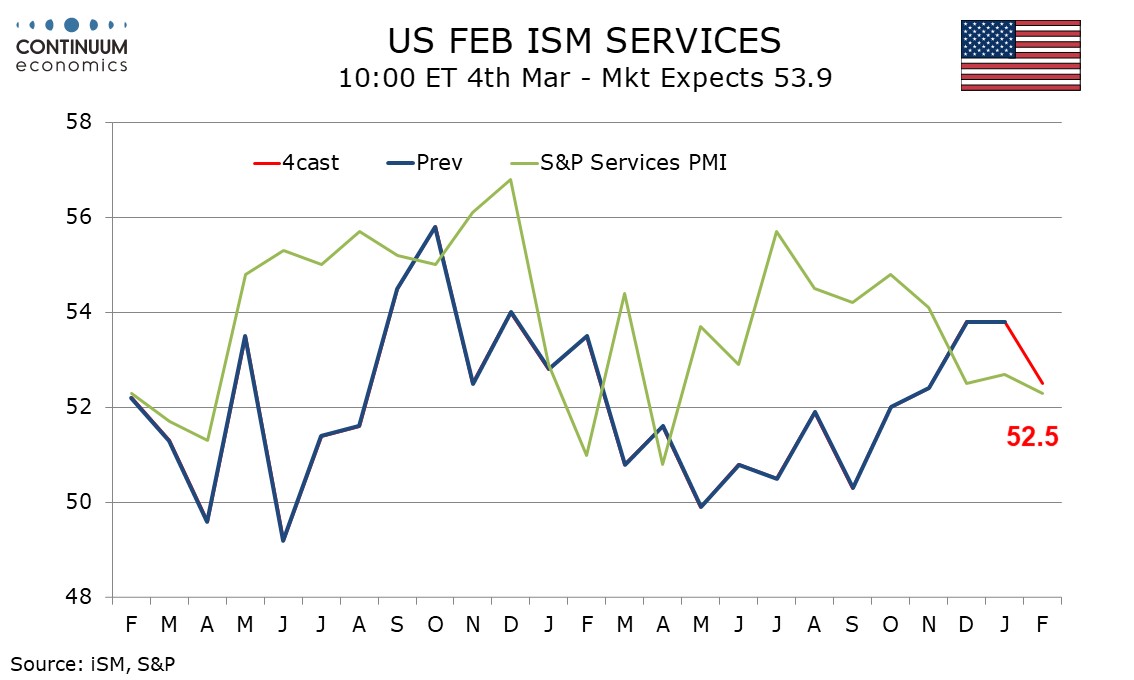

We expect February’s ISM services index to slip to 52.5 after two straight months at 53.8. This would still be stronger than each month from March through November of 2025. It would also be slightly stronger than a February S and P services index of 52.3, that was the weakest since April 2025. Regional Fed services sector surveys from the Philly, Richmond, Dallas and Kansas City Feds, as well as the Empire State, were all weaker and negative in February. We expect January’s detail to show business activity and deliveries making significant corrections from improved January readings and more modest slowing in new orders and employment to complete the breakdown of the composite.

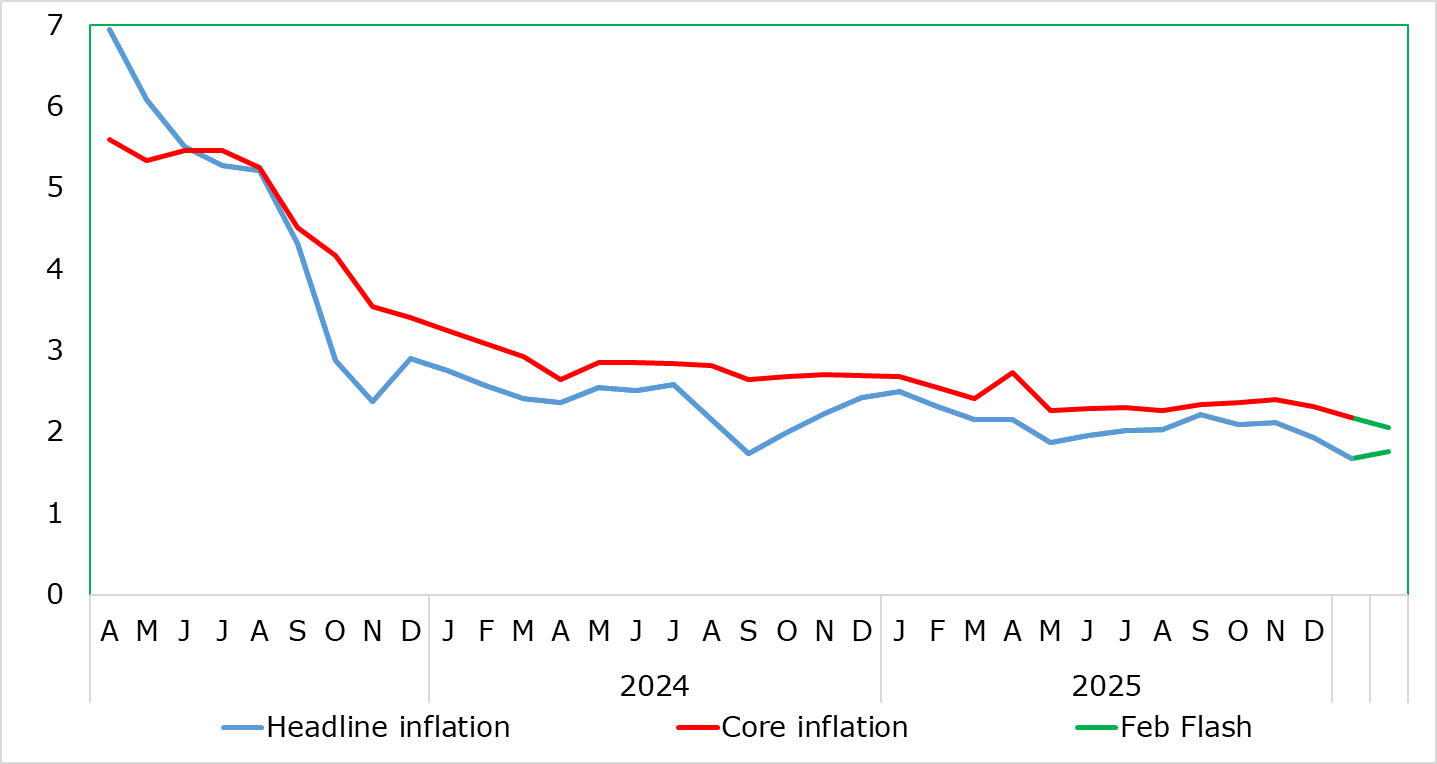

Figure: Headline and Core Converge?

Having dropped to 1.7% in the January data, thereby matching expectations and the short-lived Sep 24 outcome, it is possible that the headline HICP rate may not be any lower through this year and into next. Indeed, we see the headline rate edging up to 1.8% in the February flash mainly due to energy. But the core could drop another notch from January’s 2.2%, that being the lowest in over five years and hinting at a clear undershoot of the ECB’s Q1 2026 projection. Partly this reflects a further slowing in services inflation, but also even weaker non-energy goods prices (NEIG). To a large extent, this expected fall in the latter reflect softer import prices. But while inflation is not much of an issue for the ECB given its proximity to target, more weakness in services allied to possibly NEIG inflation may cause fresh concern at the ECB is (as we forecast) it soon results in core inflation undershooting target.

As of the January numbers updated today, several methodological changes take effect in the HICP. Over and beyond the usual annual reweighting of the components, the index will also now be compiled according to the new classification. What is clear is that with (hitherto relatively resilient) services now having seen an increase in its weighting in the last four years this has acted to push up recorded overall inflation. Admittedly, this reweighting has not prevented the fall in services inflation in the last few months, instead reflecting weak demand paring back the ability of companies to raise prices, particularly those typically made at the start of each year!

Regardless, the diehard hawks at the ECB remain focused on the recent rise, or at least apparent resilience, in services inflation - this despite still target-consistent outcomes in more short-term seasonally adjusted m/m data (Figure 2). Even so, hawkish thinking seems to have reverberated within the ECB and seemingly prompted the upward revisions made in December to the 2026 HICP outlook. Regardless, over and beyond a justified more amenable reassessment of services inflation, we think the hawks will have to come to terms with other component of core inflation, namely non-energy industrial goods (Figure 2) which accounts for one third of core HICP (services the other 2/3.

For the week ahead

USA

The US data highlight is February’s non-farm payroll on Friday, where after a stronger January we expect a slower 35k increase, 50k in the private sector. We expect unemployment to rise to 4.4% from 4.3%, with an on trend 0.3% increase in average hourly earnings. We expect a slight outperformance from Wednesday’s ADP survey of February private sector employment, with a rise of 60k. On Thursday weekly initial claims data could be lifted by bad weather, while Q4 productivity and costs are also due.

Another significant release is January retail sales, due on Friday alongside the non-farm payroll. We expect a decline of 0.7%, with ex auto sales down by 0.4%, in part due to bad weather late in the month. February’s ISM reports are also due. We expect Monday’s manufacturing index to slip to 50.5 from January’s sharply improved 52.6, and Wednesday’s services index to slip to 52.5 from 53.8. Minor data due in the week include February auto sales on Tuesday, January import prices on Thursday, and on Friday December business inventories and January consumer credit. Fed’s Williams and Kashkari speak on Tuesday and the Fed’s Beige Book is due on Wednesday. Fed’s Hammack speaks on Friday.

CANADA

Bank of Canada Governor Macklem will speak on Wednesday while Deputy Governor Kozicki speaks on Monday. It is a quiet week for Canadian data. S and P PMIs for February are due, manufacturing on Monday and Services on Wednesday, while February’s Ivey manufacturing PMI is due on Friday. Q4 productivity is due on Wednesday.

UK

Coming alongside final PMI data, earlier in the week (Mon, Wed), Monday also sees money and credit data from the BoE. Thursday sees both the construction PMI and the BoE also releasing its Decision Makers’ Panel survey and the following day sees a labor market survey from REC. Tuesday sees Chancellor Reeves give her Spring Fiscal statement which will contain updated forecasts from the OBR but with the latter not providing any update on the likelihood of meeting fiscal targets

Eurozone

Data wise sees February HICP (Wed) which may see a 0.1 ppt rise to 1.8% on a headline basis, driven higher largely by energy but with the core possibly easing a notch. There are also PPI data (Wed)and retail sales (Thu) as well detailed Q4 GDP data (Fri) and perhaps the key release of the week being the labor market report (Wed) which have been losing momentum of late despite volatile business survey suggestions. In regard to the latter final PMI data (Mon, Wed) may offer little new with perhaps more interest in what are still weak construction PMI numbers (Thu). Otherwise there is an array of ECB Council speakers through the week.

Rest of Western Europe

Sweden sees what are likely to be more friendly CPI data, this time for February and where base effects may pare back the CPIF targeted measure. Switzerland too sees CPI data with headline likely to stay around 0.1% y/y. In Norway the Norges Bank has a monetary policy conference (Mon) which will involve a discussion on inflation targeting.

JP

Quite a quiet calendar for Japan next week. Starting the week with unemployment rate on Tuesday, followed by other tier two data on Thursday. Neither would have a significant impact towards the JPY nor forecast revision.

AU

The Q4 GDP will be released on Wednesday and is expected to remain in positive territory. There is also trade data on Thursday, PMIs on Tuesday and private inflation survey on Monday.

NZ

No important releases next week for NZ.

Recap of the week

U.S. and Iran

"New" Tariffs From Trump

This Week's Fed Speakers

Tokyo CPI Dips Further Below 2%

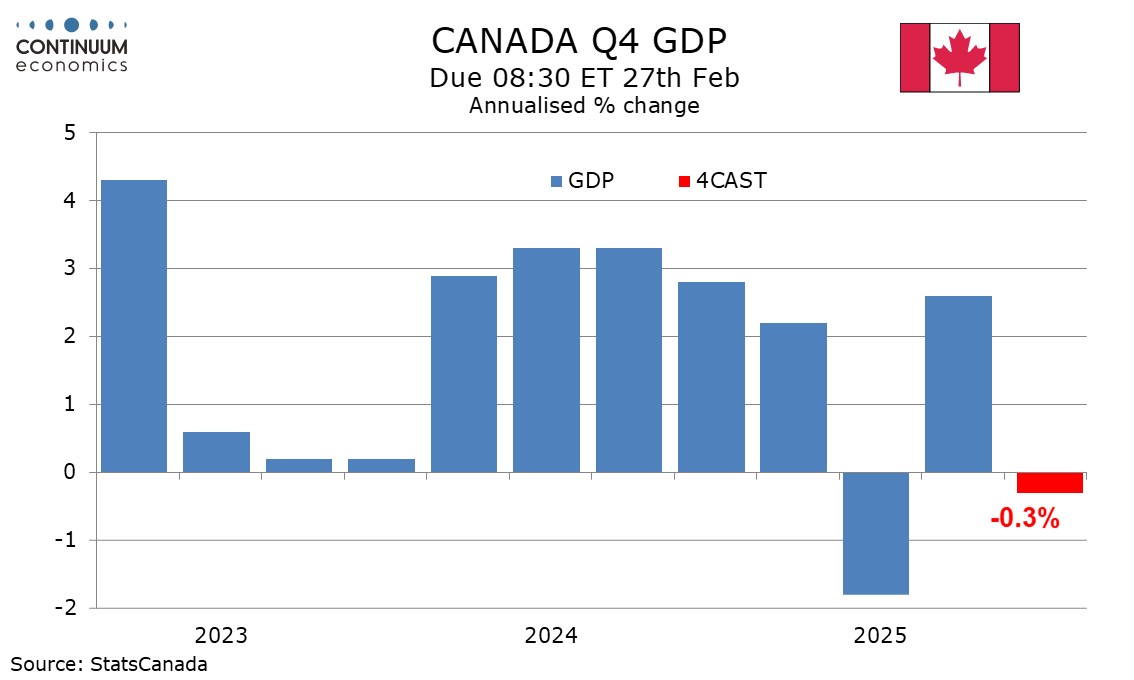

Canada Q4 GDP a modest correction

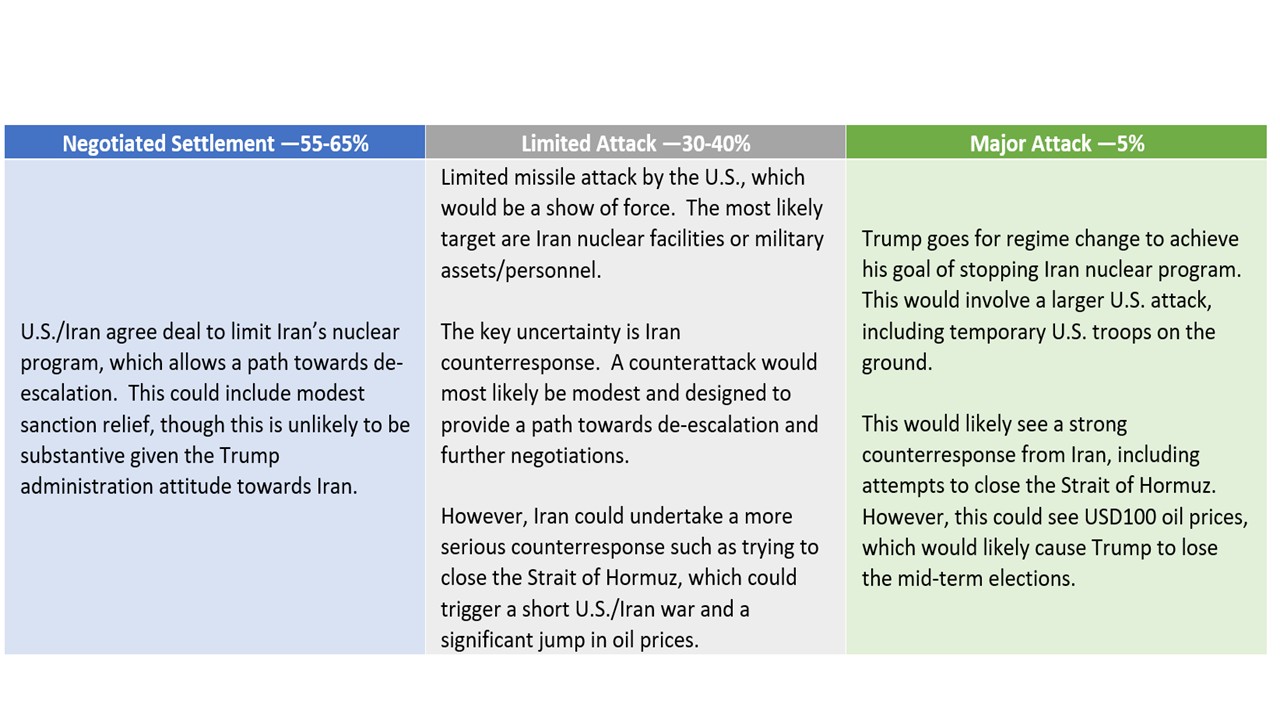

Iran authorities appear reluctant to meet the Trump administration’s demand to stop nuclear fuel production for potential weapons. This increases the odds of a limited attack by the U.S. on Iran to 30-40% (Figure), which could occur as soon as this weekend. The most likely Iran counterattack would once again be designed to allow a path towards de-escalation and then better negotiations. However, modest odds exist of Iran trying to close the Strait of Hormuz, which could spike oil prices up to USD100.

The U.S. armada off Iran is designed as a show of force, but Iran has not caved in during the negotiations. Iran authorities appear reluctant to meet the Trump administration’s demand to stop nuclear fuel production for potential weapons. This increases the odds of a limited attack by the U.S. on Iran to 30-40% (Figure 1), which could occur as soon as this weekend. Negotiators are trying to get the two sides to agree on a face saving compromise that Iran could still undertake nuclear research for medical purposes, but it is unclear whether a breakthrough will occur. (Note: Regional actors, including Turkiye and Qatar, remain concerned by the escalating tensions and continue to advocate for a formal negotiation process). The other restraining factor on Trump is that an attack could cause a jump in oil prices, which causes U.S. voter backlash given that cost of living is the number one concern before the November mid-term elections.

Figure: Cumulative Tariff Revenue (USD Blns)

The 6-3 vote by the Supreme court and full ruling against reciprocal tariffs means that the Trump administration will likely resort to other tariffs for negotiating leverage. However, the Trump administration will also pressure to codify existing trade framework deals that have been concluded with most major trading partners excluding China. The ruling could also weaken Trump’s USMCA renegotiations.

Politically this is a big disappointment for the Trump administration and Trump has already voiced his outrage. The Trump playbook will follow through with threats of replacement tariffs; anger and also distraction (e.g. dialing up Iran and/or Cuba tensions). Additionally, it appears that the prospect of a tariff refund could have to be shelved and Congress is unlikely to be in a mood to undertake new tax cuts without rebuilt tariff revenue given the fiscal situation.

The headline Tokyo CPI for February stays low at 1.6%. Ex fresh food is also below target range at 1.8% while ex fresh food and energy arrived at 2.5%. While it eases the pressure for the BoJ to hike immediately, it is worth noting a big part of moderation comes from base effect and latest round of energy stimulus.

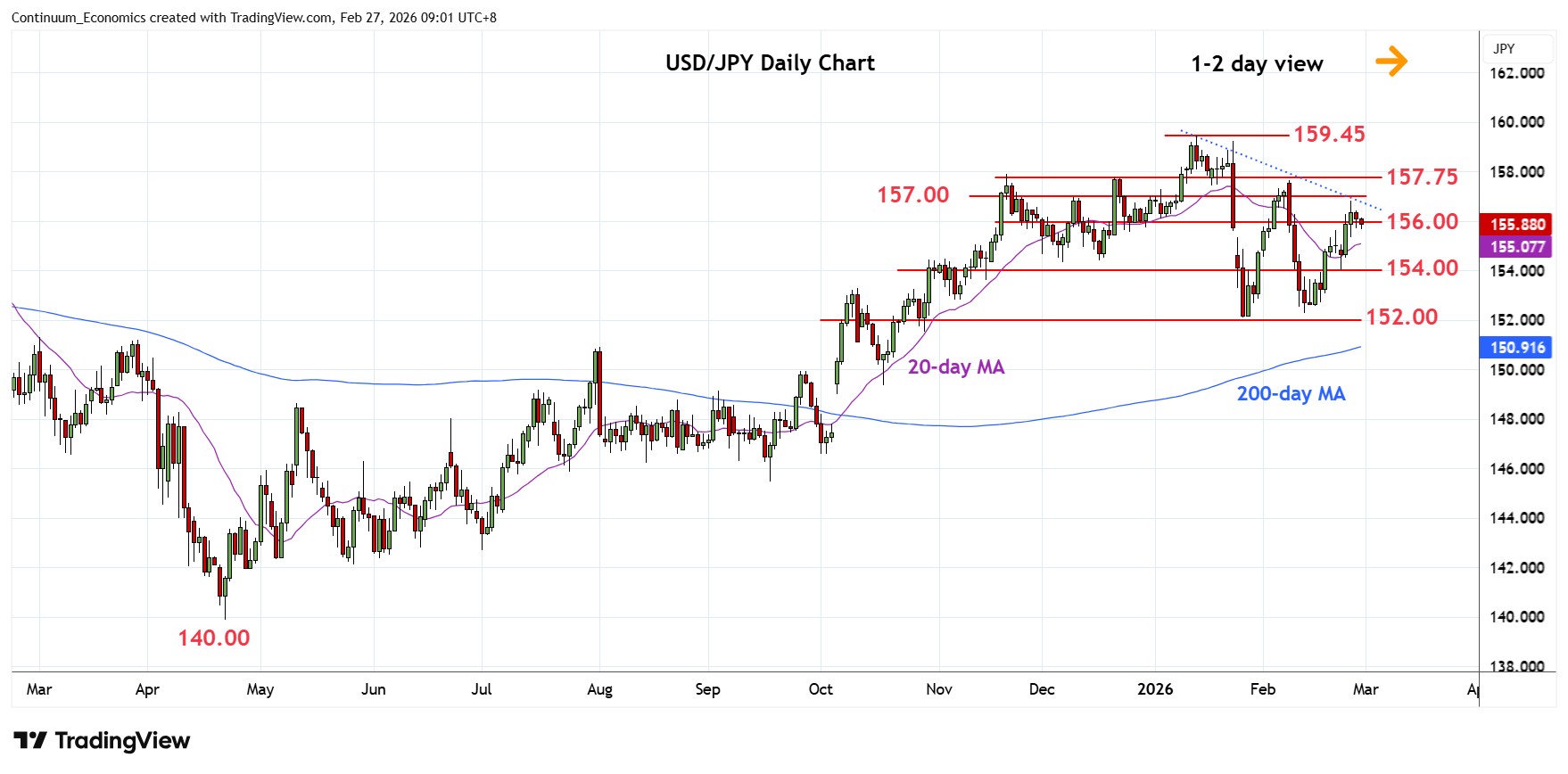

On the chart, the pair settled back to consolidate at the 156.00 level as gains met with selling pressure beneath the 157.00 resistance. Intraday and daily studies are unwinding overbought readings and suggest scope for pullback to retrace recent strong gains from the 152.27, 12 February low. Meanwhile, support remain at the 155.00 congestion and where break will fade the upside pressure and open up room for retest of the 154.00 level. Below this will return focus to the downside for retest of the 152.27 low then the 152.10, January current year low.