FX Daily Strategy: N America, October 31st

BoJ meeting a key focus – some hawkish aspect needed to halt JPY decline

Longer term JPY buyers should see current levels as attractive

Eurozone CPI data should help consolidate EUR recovery

US data likely to be ignored ahead of employment report and election

BoJ meeting a key focus – some hawkish aspect needed to halt JPY decline

Longer term JPY buyers should see current levels as attractive

Eurozone CPI data should help consolidate EUR recovery

US data likely to be ignored ahead of employment report and election

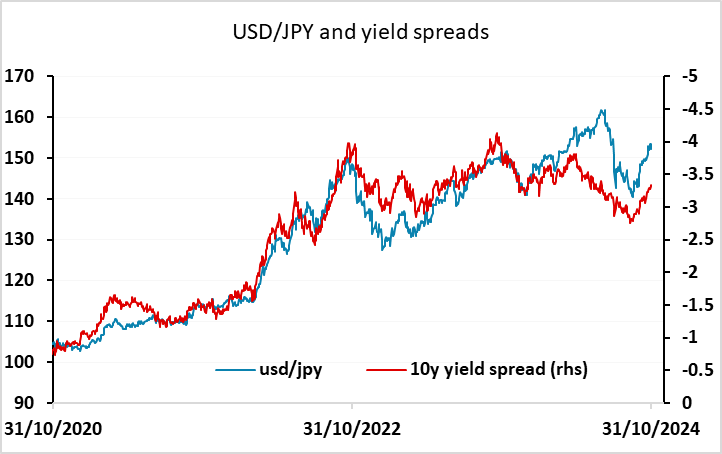

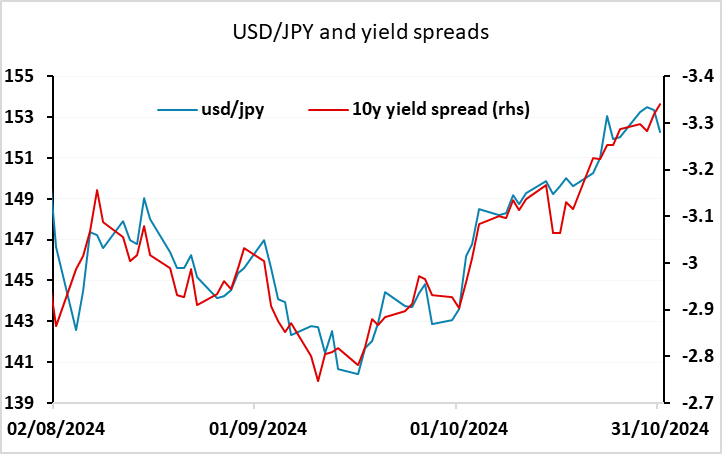

The JPY has firmed modestly on the back of the BoJ meeting and Ueda’s press conference. While there was no change to rates and no clear promise of a rate hike in December, Ueda did leave that possibility open if the US economy continued to show resilience. He indicated that wages and prices in Japan were moving up in line with expectations and were consistent with the monetary tightening cycle they anticipated, without setting any timeline. This suggests that the JPY should perform well in either scenario. If the US economy performs well, it will allow the BoJ to raise rates. If it doesn’t, US yields and equities are likely to decline and equity risk premia are likely to rise, all of which will be favourable for the JPY. The latter scenario would be more likely to trigger sharp JPY gains, but the former should provide the JPY with support as the market prices in earlier BoJ tightening. As it stands, the market is only pricing 7bps of tightening for December, and if the US, Japanese and world economy shows strength, there is potential for a 25bp hike.

For now, USD/JPY is unlikely to fall far – the short term yield spread correlation suggests we may see a recovery back to yesterday’s highs, although longer term correlations still suggest downside risks. Obviously, there will be sensitivity to tomorrow’s employment report and next week’s US election. While CFTC data doesn’t indicate significant positioning, we would expect the short term market to be short JPY after the 10 figure USD/JPY rise in October, so there is some risk of position squaring favouring the JPY into the end of month.

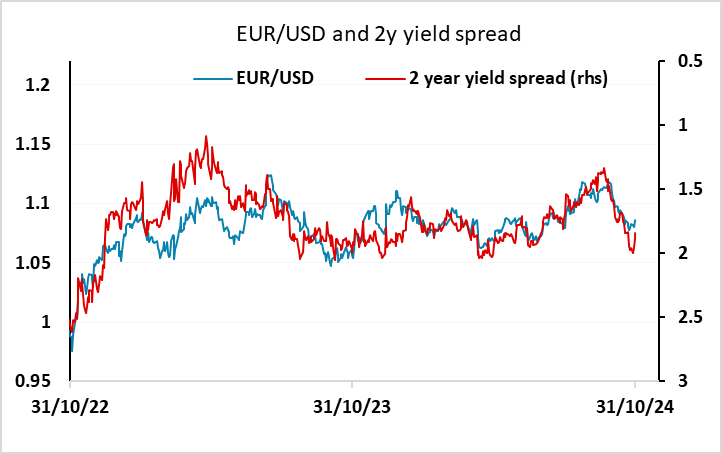

After the BoJ meeting we had the remaining preliminary CPI data from the major Eurozone countries and the Eurozone CPI itself, which were stronger than consensus. Along with the stronger Eurozone GDP data seen on Wednesday, and strong German retail sales data this morning, this helps to reduce market expectations of more rapid ECB easing. This in turn limits the EUR downside, and although yield spreads still suggest some EUR/USD downside risk, it is looking increasingly hard to make any progress below 1.08 without a significant change in market expectations for Fed policy. This of course might come on the back of the employment report, but more likely won’t be seen this side of the election.

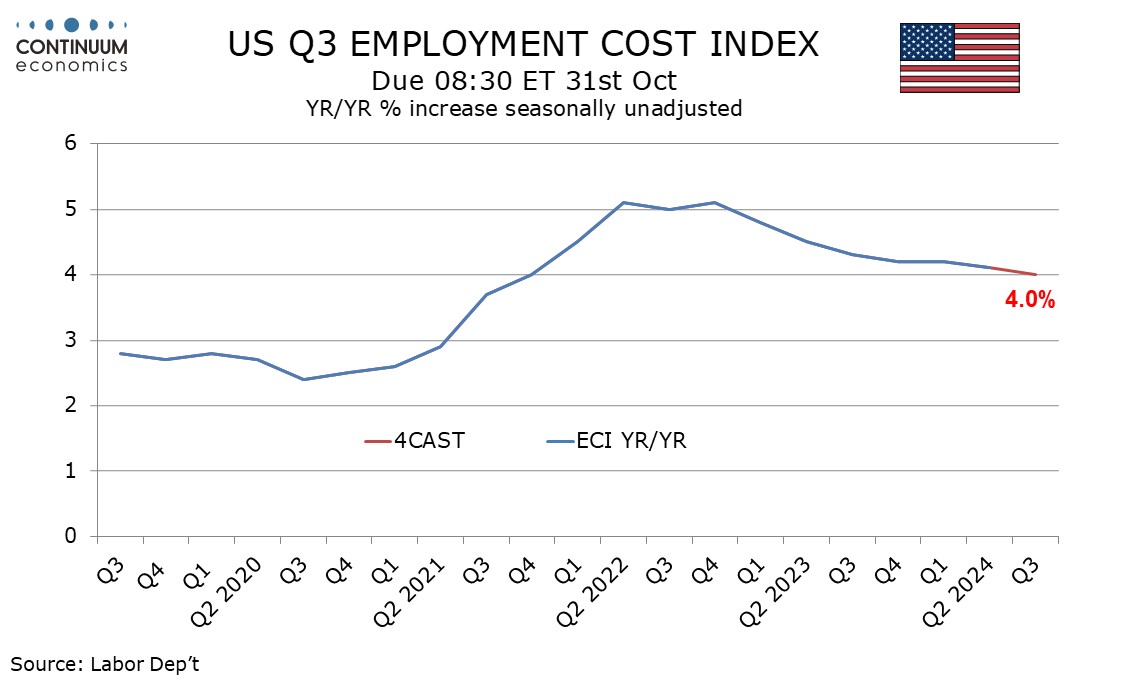

On the US side, Thursday sees the PCE price index for September and the employment cost index for Q3, both of which could be significant for Fed policy going forward. We look for the Q3 employment cost index (ECI) to increase by 0.9%, matching the gain of Q2, though with slightly firmer growth in wages and salaries offset by a slowing in benefit costs. This is in line with consensus, so probably won; trigger a significant reaction, but supports the Fed easing trajectory inasmuch as it shows the y/y rate of growth slowing to 4.0%, so if anything this may be mildly USD negative, although with the focus on the employment report and the election next week, reaction should be small.