FX Daily Strategy: Asia, April 10th

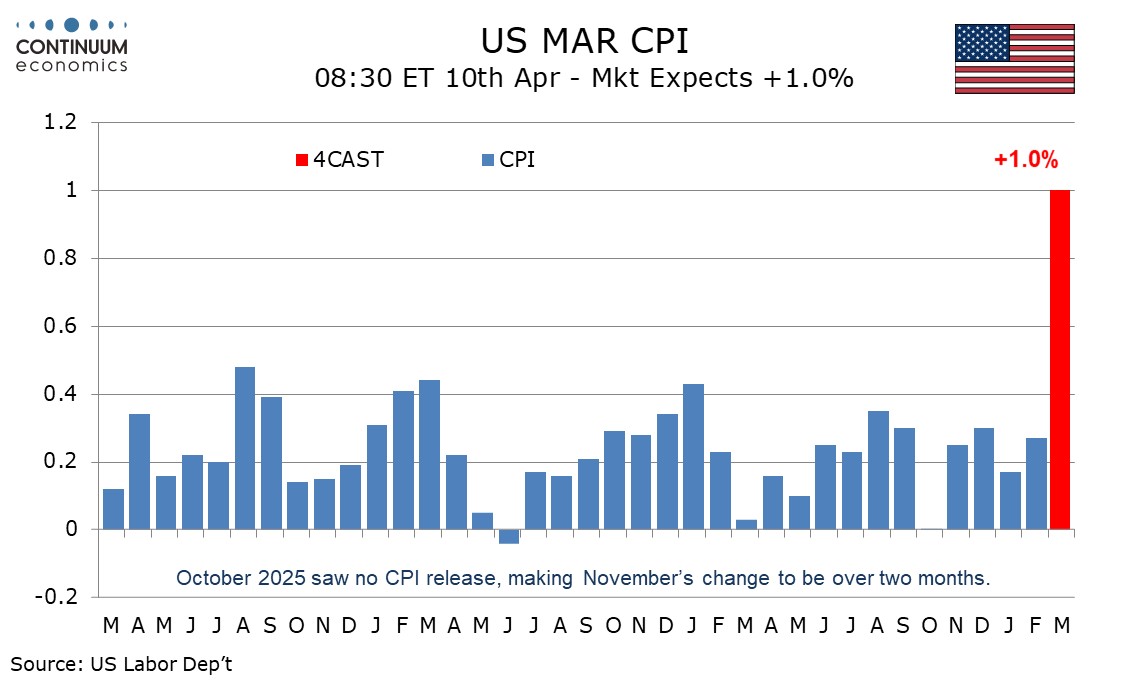

U.S. March Core CPI similar to February

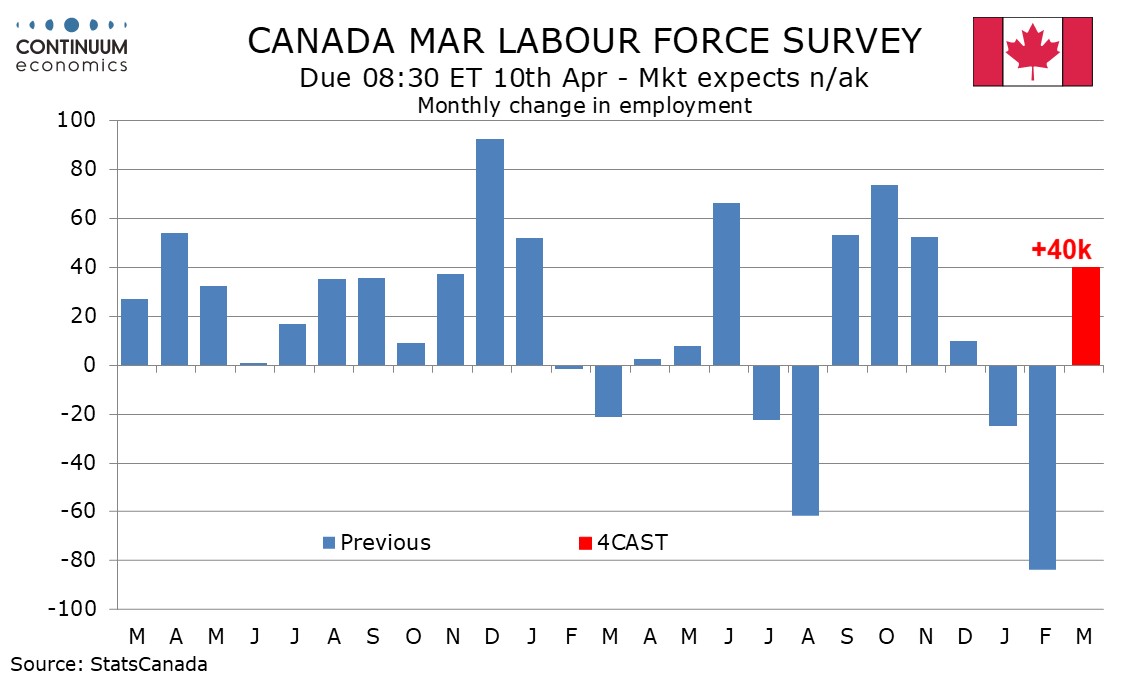

Canada March Employment Highly volatile

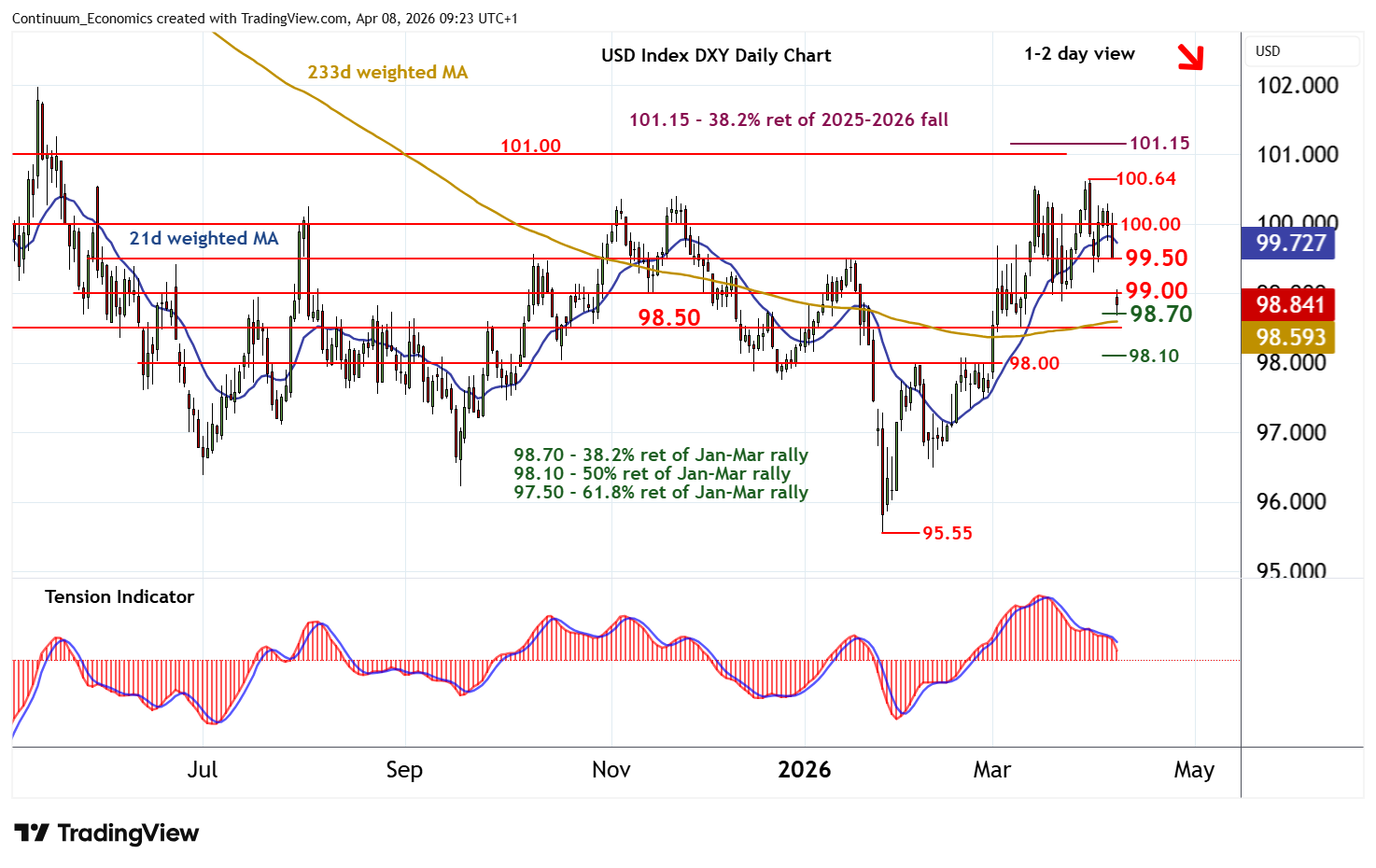

DXY Extending March losses

We expect March CPI to surge by 1.0% overall, which would be the strongest rise since June 2022, seen in the aftermath of the Russian invasion of Ukraine. However we expect only a moderate increase ex food and energy, of 0.22% before rounding, which would match that seen in February. Even with some restraint from seasonal adjustments, gasoline prices look sure to see a sharp surge, which will explain nearly all of a 12.5% increase in energy, with most other components of the energy breakdown likely to seen only modest changes. We expect a moderate 0.3% increase in food, but there are upside risks going forward with the closure of the Strait of Hormuz disrupting fertilizer supplies.

Ex food and energy data has been showing a loss of momentum in recent months, with trend now looking close to 0.2% per month and even January at 0.3% not showing as strong a new year bounce as did most recent years. However PPI, some of which impacts core PCE prices, has been showing some acceleration even before the energy shock.

We expect Canadian employment to increase by 40k in March, in a correction from an exceptionally large decline of 83.9k in February which may have been influenced by weather. While the data has been very volatile, underlying trend is probably still moderately positive. We expect an unemployment rate of 6.6%, down from 6.7% in February but above January’s 6.5%.

Employment data from the last nine months have seen four increases in excess of 50k, and two declines, two in excess of 50k and two slightly steeper than 20k. Only one month, a 10.1k increase in December, came in close to February’s 6-month average of 13.5k, which is probably a reasonable estimate of trend. A separate monthly payroll survey, for which data is available only to January, has a 6-month average of 9.2k, though this was lifted by a 45.6k increase in January, a month when the employment report saw a 24.8k decline.

On the chart, cautious trade has given way to a sharp pullback, with prices currently consolidating the test of support at the 98.70 Fibonacci retracement. Daily readings have turned down and overbought weekly stochastics are unwinding, highlighting room for further losses in the coming sessions. A break below 98.70 will open up congestion around 98.50, with room for continuation down to 98.00/10. However, the rising weekly Tension Indicator and positive longer-term charts should limit any initial tests of here in short-covering/consolidation. Meanwhile, resistance is lowered to congestion around 99.00. A close above here, if seen, would help to stabilise price action and prompt consolidation beneath further congestion around 99.50.