FX Daily Strategy: Europe, March 13th

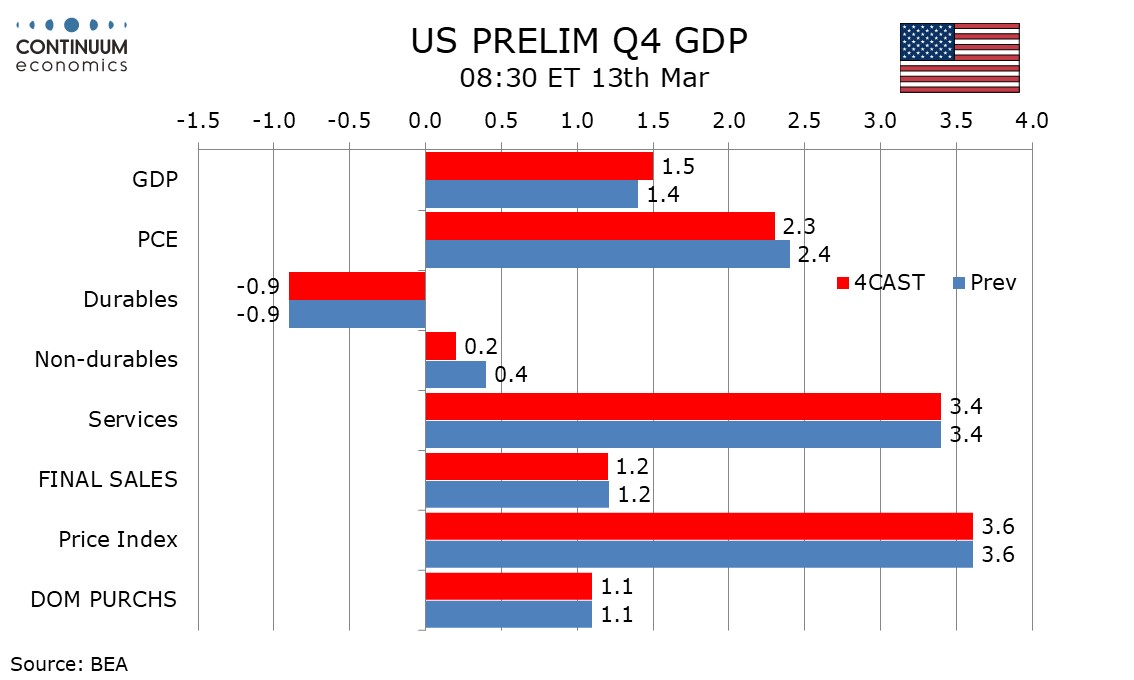

U.S. Preliminary Q4 GDP Marginally stronger on housing

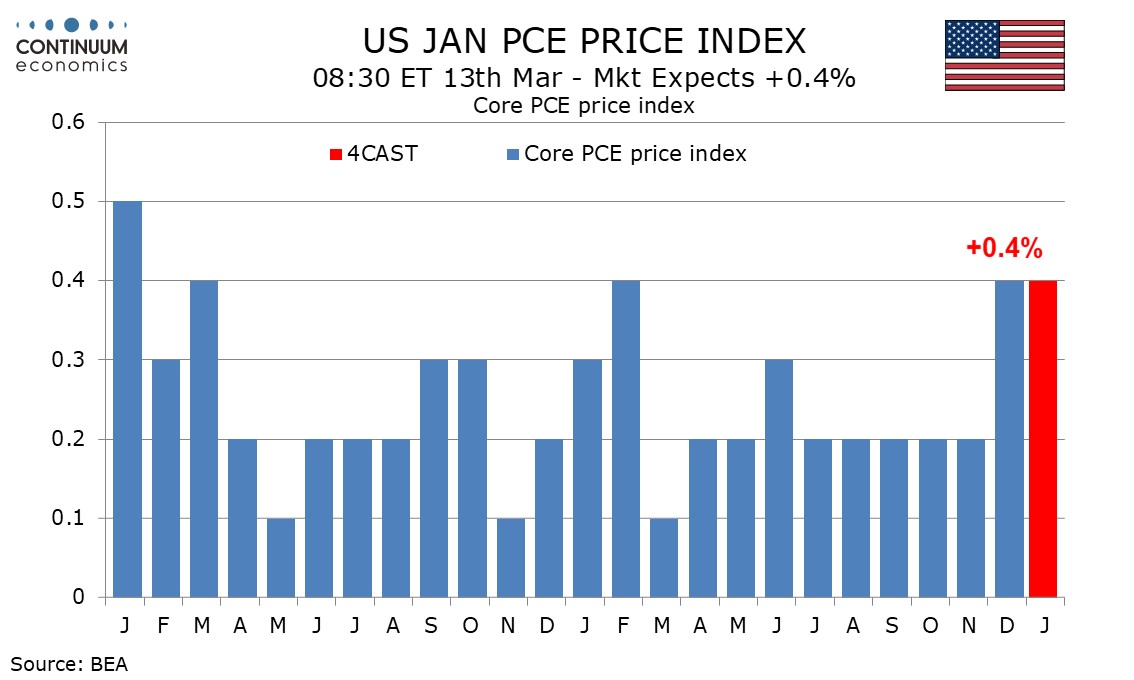

And Core PCE Prices to outperform CPI

UK GDP Getting Better?

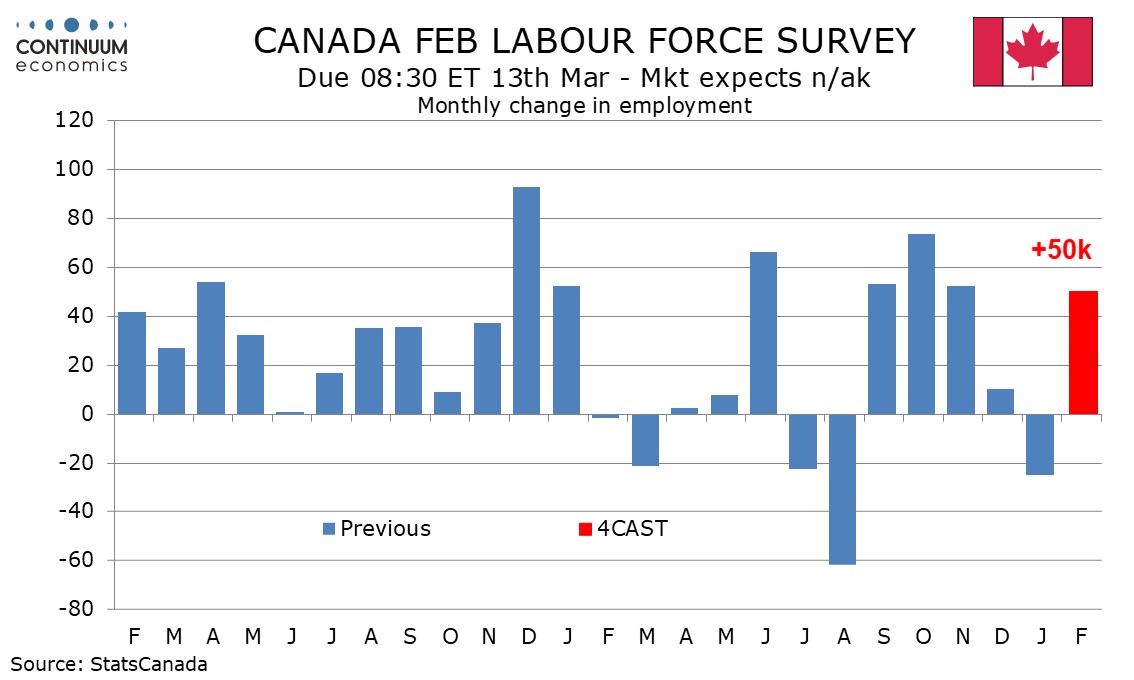

Canada February Employment due for a rebound in Ontario

We expect a marginal upward revision to Q4 GDP to 1.5% in the preliminary (second) estimate from 1.4% in the advance (first) release, led by an upward revision to housing investment to a 1.7% rise from a 1.5% decline. The upward revision to housing investment is implied by November and December construction spending data, which was released after the advance GDP data. This will outweigh implied marginal downward revisions to non-residential construction, both private and public, and retail sales. While we expect the USD revision to both final sales and final sales to domestic buyers to match that seen for GDP, the annualized percentage changes to the former two are likely to be unrevised, at 1.2% and 1.1% respectively. We do however expect final sales to private domestic buyers to be revised up to 2.5% from 2.4%. Government was restrained by the shutdown.

We expect January to see a strong core PCE price index increase of 0.4%, matching the rise seen in December. We expect personal income to increase by 0.6%, unusually outpacing personal spending, which we expect to rise by 0.4% for a third straight month. CPI increased by 0.2% in January with a 0.3% increase ex food and energy. However given that the PCE price components of the PPI were strong in January, we expect the PCE price index to outperform the CPI, rising by 0.3% overall, and 0.4% ex food and energy. This would see the yr/yr pace for overall PCE prices slip to 2.8% from 2.9% though the core rate would increase to 3.1% from 3.0%, reaching its highest pace since March 2024.

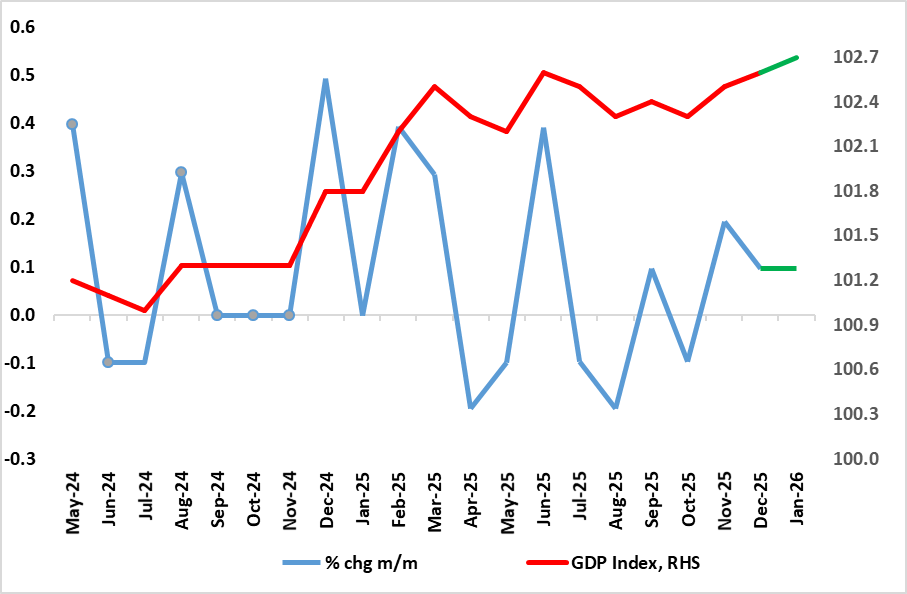

Figure: GDP Growth Better But Hardly Strong?

Belatedly, some good news; the UK economy grew for a second successive month in December, something not seen for almost a year. Even more encouragingly, it may very well enjoy a further rise in the looming January data, thereby providing the best three-month showing in two years. But as is familiar with recent UK real economy data, there is a negative flip side with the positive growth rates still feeble so that the economy grew by 0.1% q/q in Q4, less than consensus and BoE thinking but matching the feeble gain of the previous quarter. Moreover, any improvement in activity and sentiment will, of course, be hit by events in the Middle East, implying that even if a base effect induced pick-up in GDP growth to 0.2% this quarter does occur, it will be fleeting. Even without the Middle East impact we were suggesting a sub-consensus 2026 GDP picture of 0.8% which now has even greater downside risks attached.

Activity in December was impaired by fresh weakness in manufacturing, utilities and construction. The data seemingly reinforced the demand worries of what now seems to be an emerging majority on the MPC; six members of the MPC appear worried about the disinflationary impact from a weak economy - four of whom actually voted for a 25bp cut at last month’s meeting.

Indeed, even given a modest further January rise, this would merely take the level of GDP to a bare notch above where it was in June. That January rise is likely to be based around already-released better retail sales data, albeit offset by what may be more (vehicle-based) manufacturing weakness and possible marked drop in the housing market.

We expect Canadian employment to increase by 50k in February, more than fully reversing a 24.8k decline in January to keep trend modestly positive. However we expect an even stronger rebound in the labor force from a decline in January to lift the unemployment rate to 6.6% from 6.5%, while remaining below December’s 6.8%. January’s 24.8k decline in employment was more than fully explained by a 66.5k decline in Ontario. January also saw a fall of 119k in the labor force, which was more than fully explained by a decline of 136k in Ontario. That January’s slippage was more than fully explained by Ontario hints at temporary factors, probably weather, which will be corrected in February, though there are risks of continued negative weather distortions in February.

We expect February’s employment gain to come fully in part time work, correcting from two straight declines, while full time work pauses after two straight strong gains. Job gains are likely to be led by components that slipped in January, notably manufacturing, education and retail/wholesale. We expect February’s labor force to increase by 100k, which would lift the unemployment rate to 6.6% from 6.5%, though before rounding the rue would be close to 0.2%, to almost 6.65% from 6.46%. The participation rate would rise to 65.3% from 65.0%. We expect the average hourly wage of permanent employees to correct higher to 3.5% yr/yr from 3.3% in January, still below December’s 3.7%.