Norges Bank Preview (Nov 6): On Hold but Another Cut Flagged By End-Year

After what was to some a surprise move in September, in which the Norges Bank cut is policy rate by a further 25 bp to 4.0%, we see no change at Nov 6 verdict. After all, there will be no fresh forecasts, albeit with the Board likely to reinforce existing hints of a further 25 bp move at the Dec 18 decision. That December meeting will have both new forecasts and data for the Board to peruse, not least inflation and lending numbers, the latter possibly becoming a worry given the fresh slowing in corporate credit growth (Figure 1). But with inflation dynamics ever more friendly (Figure 2), we still think that the Norges Bank is being too cautious and that (on the basis of its own calculations), policy will be very restrictive through the projected timeframe out to 2028 and where we wonder why inflation only just approaches the 2% target by the end of that period.

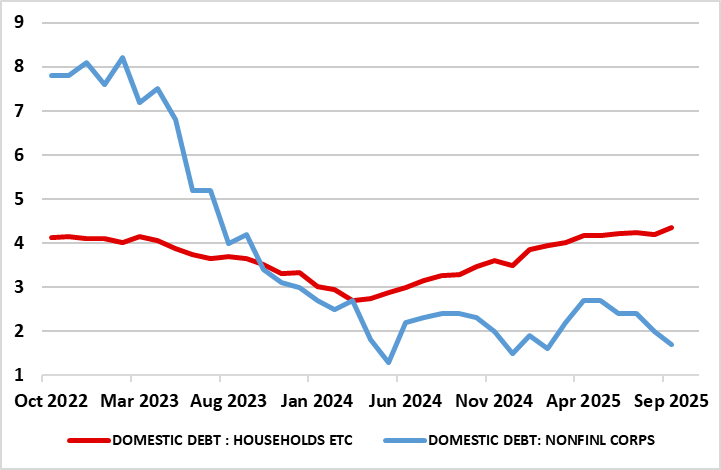

Figure 1: Corporate Credit Growth Slowing Afresh

Source: Stats Norway, % chg y/y

We remain a little less confident about the extent of easing into 2026 but after another 25 bp cut likely in December we then envisage further such moves every quarter through next year. That would still leave the policy rate roughly in the middle of the neutral rate range estimated by the Norges Bank. In other words, the Norges Bank will be merely taking its foot of the brake, rather than pressing on the accelerator. But inflation worries continue to dominate Norges Bank thinking, this possibly accentuated by the small cumulative upgrade to the real economy outlook and an ensuing reduction in the anticipated scale of an output gap see last time around.

While still a full ppt above target, targeted (CPI-ATE) inflation is being boosted by stubborn services inflation, this partly offsetting ever softer goods and imported inflation, the latter coming in spite of the weak Krona backdrop that continues to influence Board thinking excessively – albeit the latter having steadied, if not bounced of late. The hawkish line still being pursued by the Norges Bank still only helps bring inflation in its view back to target only 3 years hence, at least according to its updated MPR. As for last rate cut, which was apparently no formality, the Board may have been swayed by signs of a softer labor market in spite of a (justified) GDP upgrade given recent data) but where we doubt that there is much evidence to suggest an ensuing and clear reassessment of the still likely negative output gap.

Indeed, the economy (both real and nominal) has been strong so far this year. Admittedly the cumulative jump in GDP of around 1.8% does reflect a few volatile factors, namely swings in fisheries and power supply as well as easier fiscal policy. But the strength also comes alongside some signs of a possible stronger potential growth backdrop, this hinted at by both seemingly better productivity data and a further rise in activity, meaning that overall utilization may actually not be too far away from normal if not showing spare capacity. But there are some more worrying signs emerging, especially in regard to corporate credit – both demand and supply. Actual data show that in contrast to household credit, growth on the corporate side is waning afresh and where the Norges Bank’s recent bank lending survey note that banks report a slight decline in non-financial corporate credit demand in the last quarter. Demand was weaker than expected in Q2, and banks expect no change in Q4.

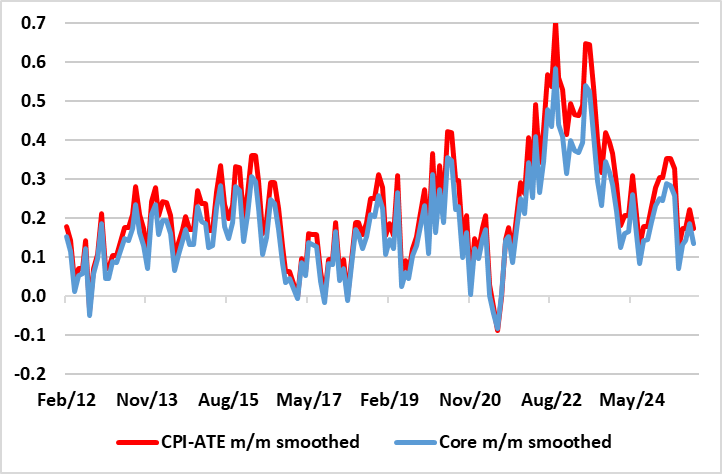

Figure 2: CPI Dynamics More Friendly in Adjusted Short-Run Perspective

Source: Stats Norway, CE, smoothed is 3 mth mov avg

Thus, as for inflation, we think that the Norges Bank is still being too cautious, even though we would not disagree materially with its upgraded 2.0% and 1.5% mainland GDP projections for the year and next. In fact, we would contend that an emerging and earlier output gap is partly responsible for the marked fall in inflation seen of late – admittedly unwinding the overshoot of the early part of 2025. Notably, although seemingly suggesting price persistence, September data showed that despite targeted inflation (CPI-ATE) only falling a notch at 3.1%, chiming with Norges Bank thinking, the details, CPIF and core inflation (ie the latter ex food) are running at rates more consistent with the 2% target on an adjusted and smoothed m/m basis (Figure 2).