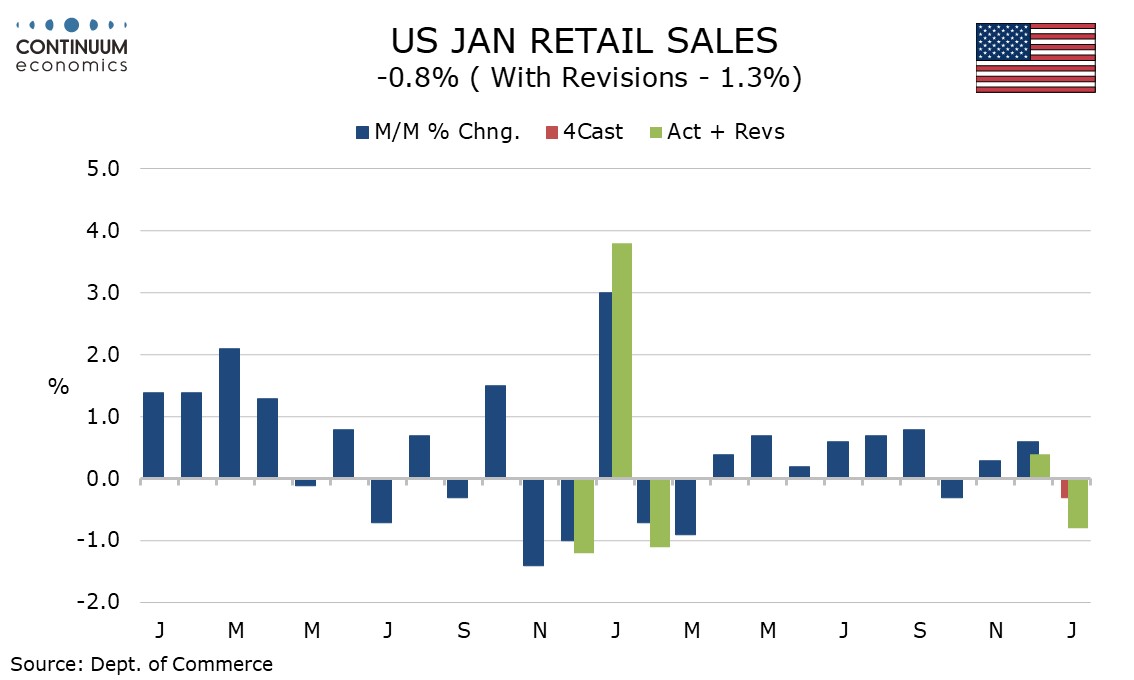

U.S. January Retail Sales See a Significant Dip to Start the New Year

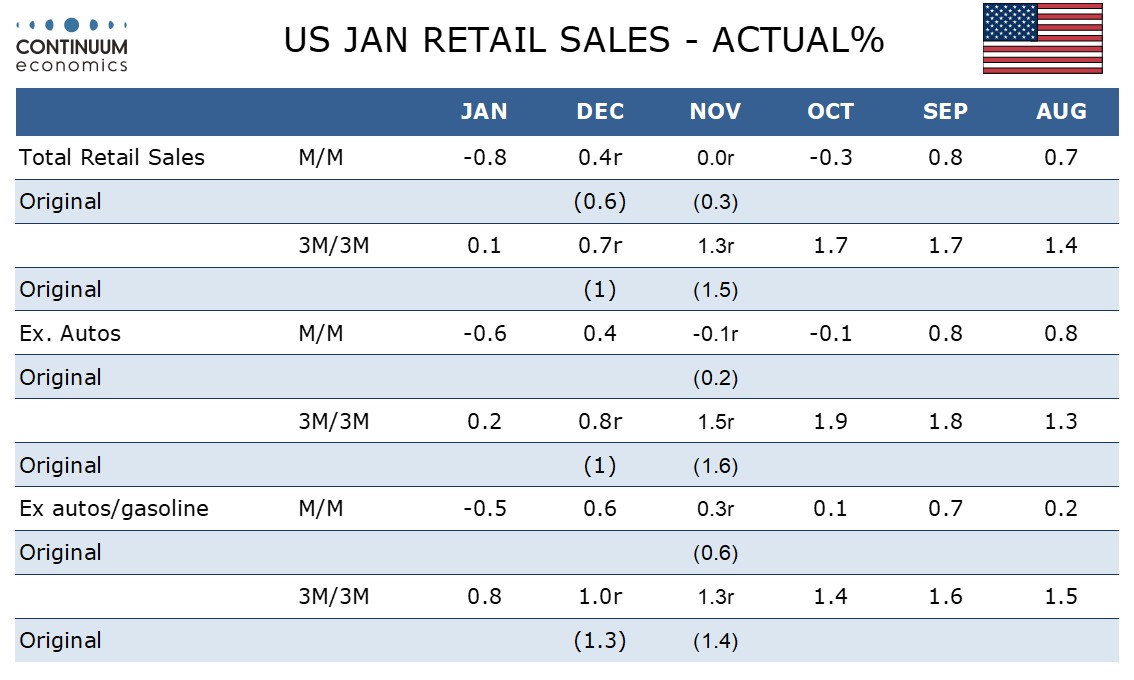

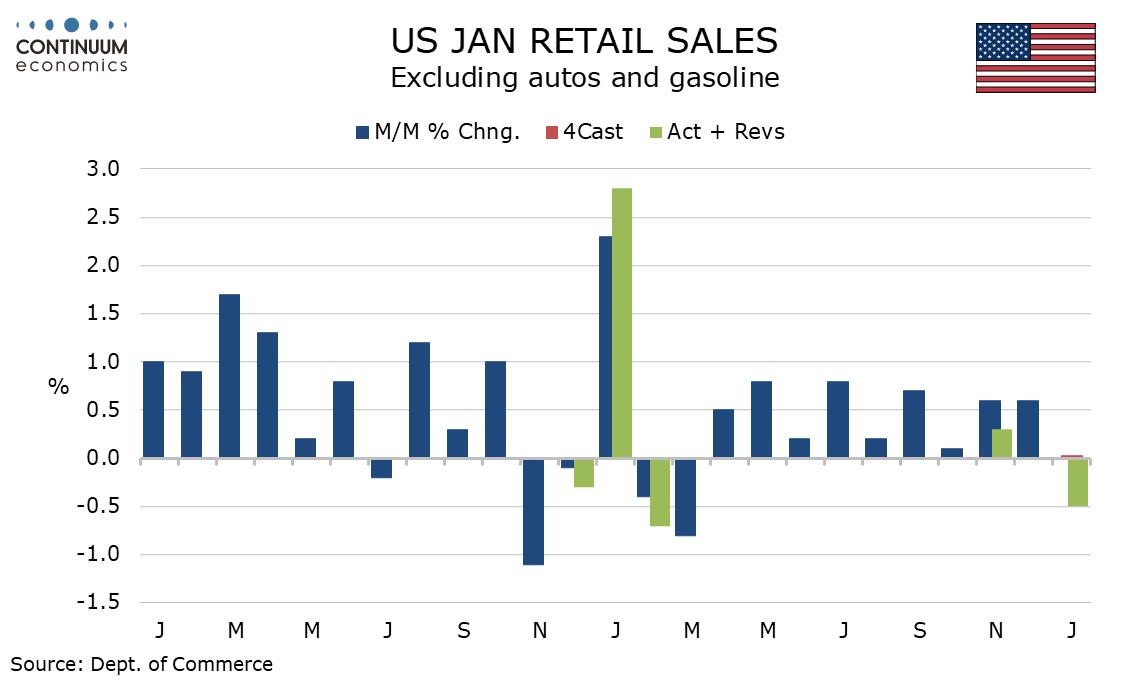

US retail sales have made a weaker than expected start to Q1, falling by 0.8% overall, 0.6% ex autos and 0.5% ex autos and gasoline. One weak month after a strong Q4 (though Q4 did see downward revisions with this report) does not make a trend however, and January’s weakness may be in part weather-induced.

December retail sales were revised down to a 0.4% increase from 0.6% and November was revised to unchanged from +0.3%, so the data is significantly weaker than expected net of revisions.

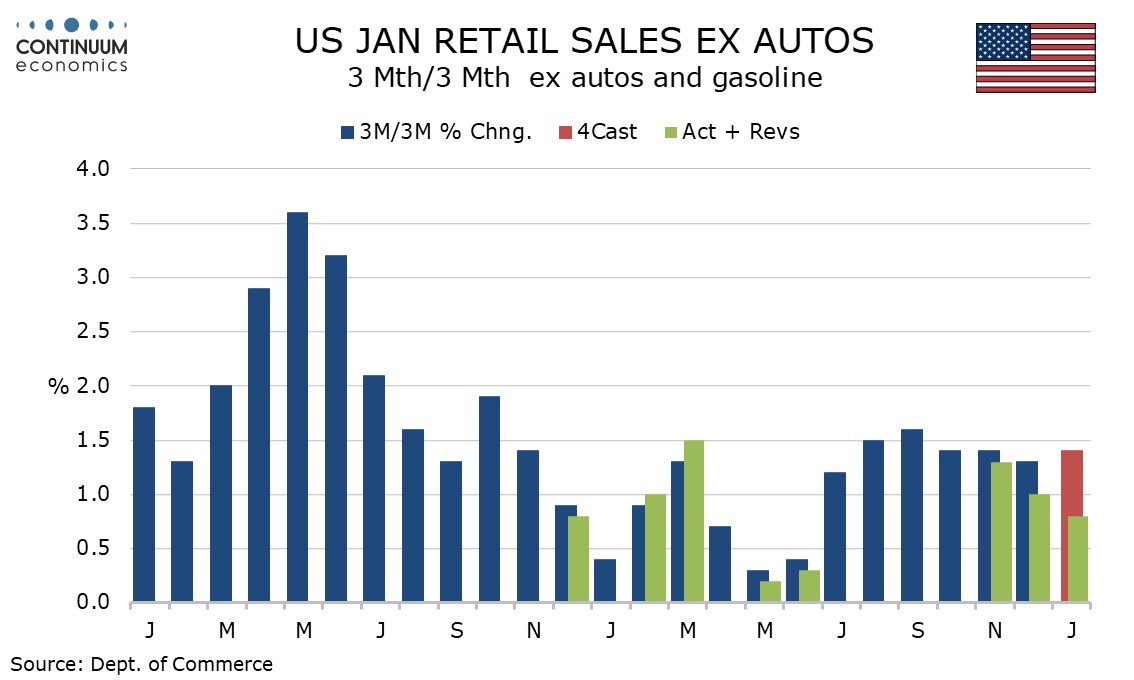

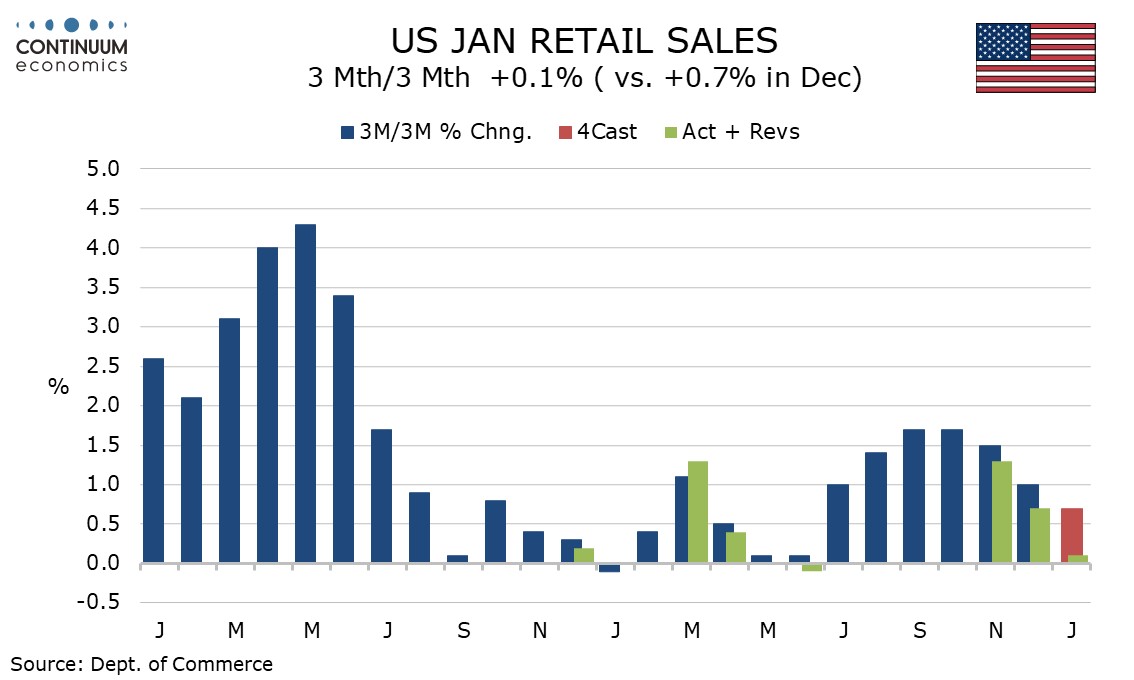

3m/3m data has weakened significantly to increases of 0.1% overall and 0.2% ex autos (not annualized) but the ex-auto and gasoline pace is still solid, if a little slower, at 0.8% 3m/3m.

3m/3m data has weakened significantly to increases of 0.1% overall and 0.2% ex autos (not annualized) but the ex-auto and gasoline pace is still solid, if a little slower, at 0.8% 3m/3m.

The data will restrain what had been mostly still strong preliminary estimates for Q1 GDP. However January data should be treated cautiously. January 2023 was unusually strong when weather was unusually mild and February and March subsequently corrected lower.

The data will restrain what had been mostly still strong preliminary estimates for Q1 GDP. However January data should be treated cautiously. January 2023 was unusually strong when weather was unusually mild and February and March subsequently corrected lower.

January’s weakness is also in part price induced. Despite January CPI having been strong on services commodity prices fell by 0.3%. A 1.7% fall in gasoline sales is price-related but a similar fall in autos is as signaled by industry data that is quoted in volumes. Building materials at -4.1% were the most prominent source of weakness while heath and personal care at -1.1% was unusually weak.

January’s weakness is also in part price induced. Despite January CPI having been strong on services commodity prices fell by 0.3%. A 1.7% fall in gasoline sales is price-related but a similar fall in autos is as signaled by industry data that is quoted in volumes. Building materials at -4.1% were the most prominent source of weakness while heath and personal care at -1.1% was unusually weak.

Initial claims at 212k from 220k still signal a tight labor market though continued claims increased to 1.895m from 1.865m.

Initial claims at 212k from 220k still signal a tight labor market though continued claims increased to 1.895m from 1.865m.

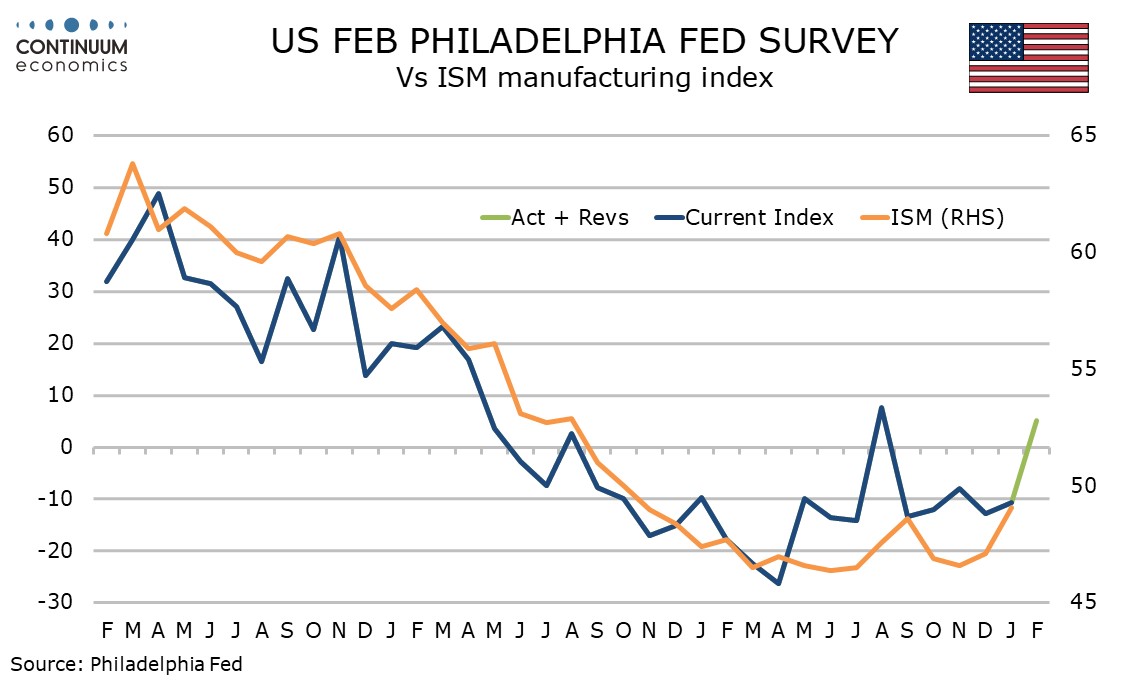

February’s manufacturing surveys from the Empire State at -2.4 from a very weak January reading of -43.7 and the Philly Fed which turned positive at 5.2 from -10.6 were both significantly improved. This follows improved national data from the ISM and S and P manufacturing surveys in January.

February’s manufacturing surveys from the Empire State at -2.4 from a very weak January reading of -43.7 and the Philly Fed which turned positive at 5.2 from -10.6 were both significantly improved. This follows improved national data from the ISM and S and P manufacturing surveys in January.