FX Daily Strategy: Asia, March 4th

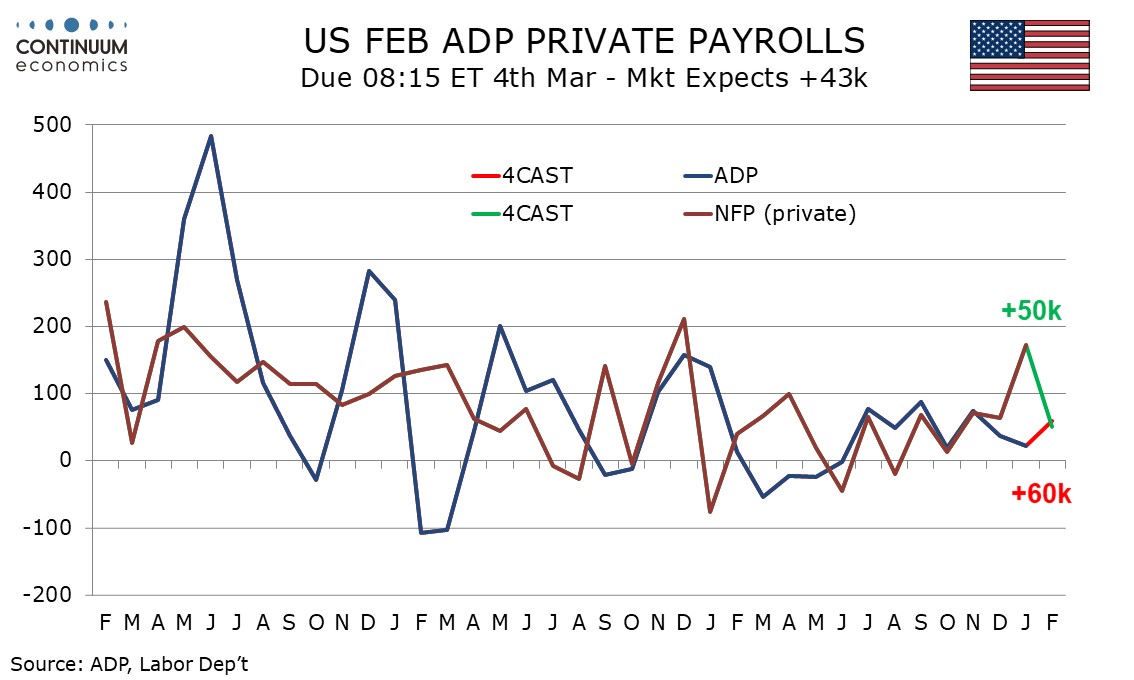

U.S. February ADP Employment To pick up

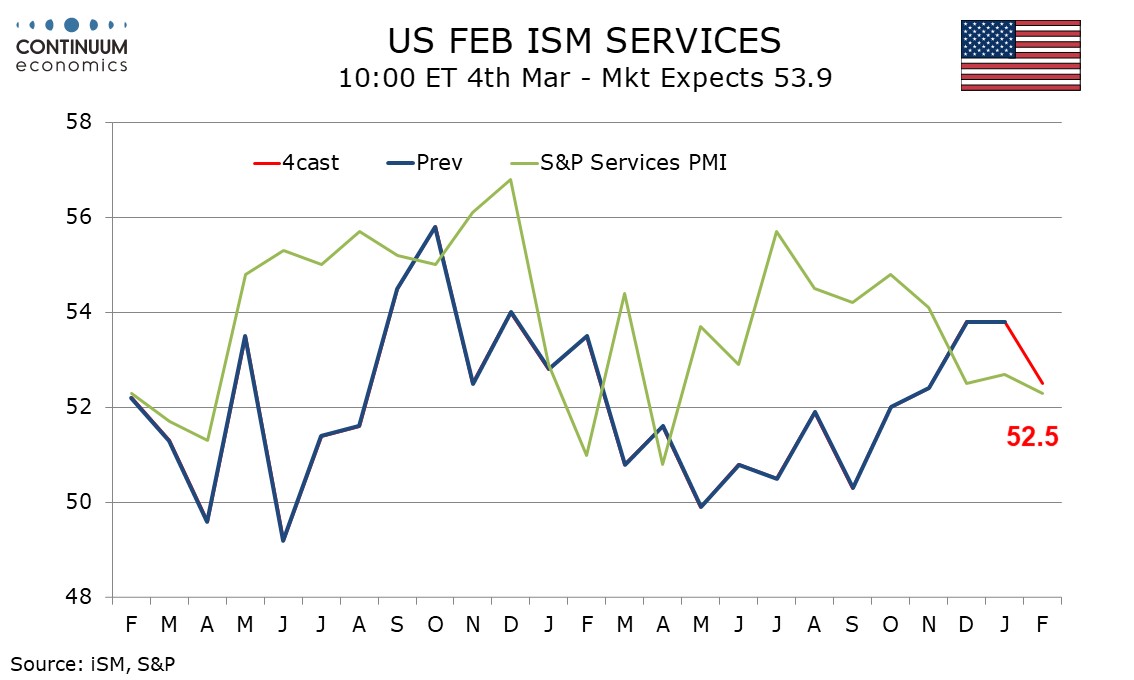

U.S. ISM Services suggest some slowing

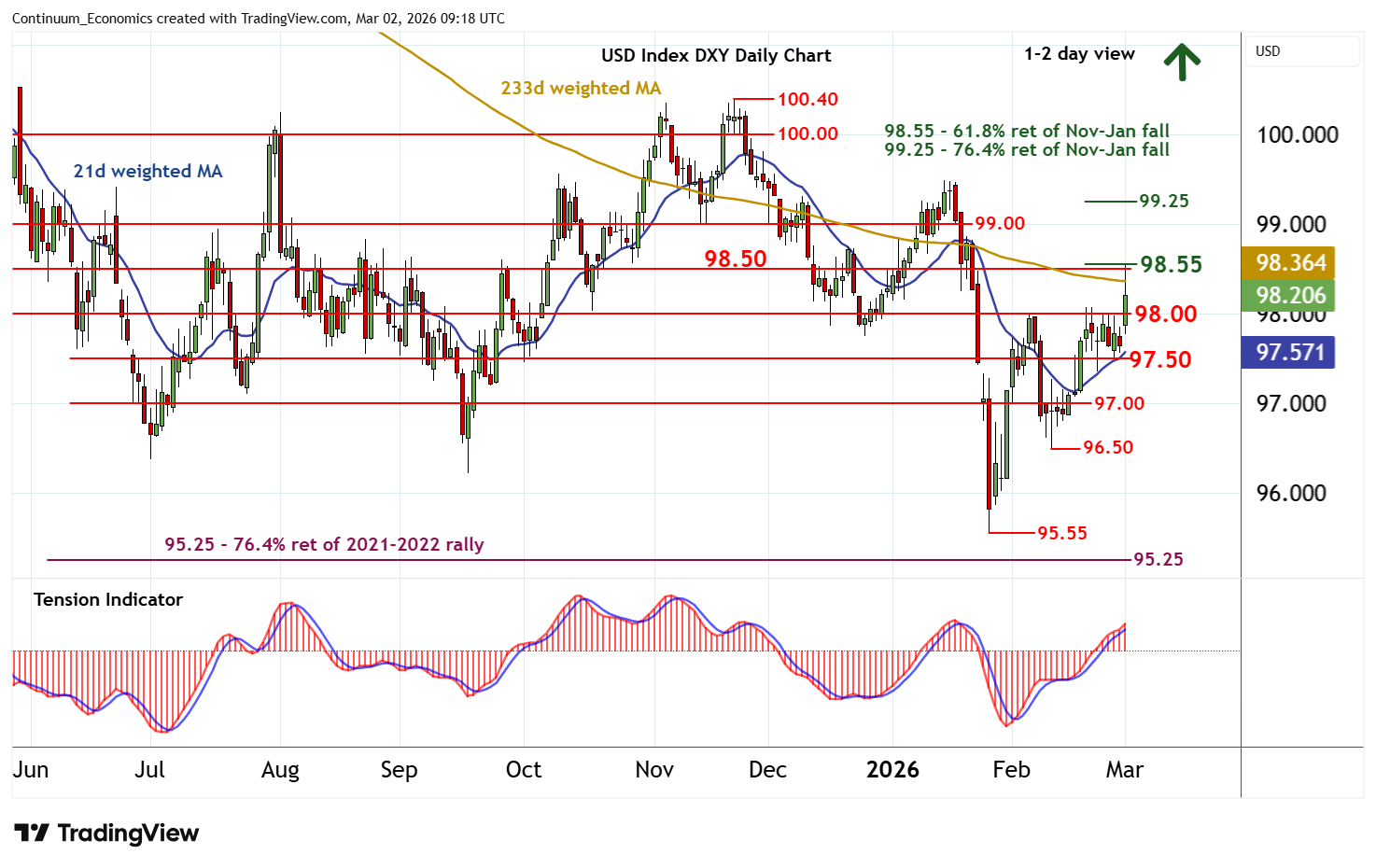

USD Could Gain Further Stronger

We expect a 60k increase in February’s ADP estimate for private sector employment, which would be a significant pick up from January’s 22k, which dramatically underperformed a 172k increase in January’s private sector non-farm payroll. We expect February’s ADP report to marginally outperform a 50k increase in private sector non-farm payrolls, while we expect overall non-farm payrolls to increase by only 35k. Bad weather in late January and early February may impact payrolls more than the ADP data, which tends to be less weather-sensitive than payrolls.

Weekly ADP data shows a 4-week average of 12.75k in the for weeks to February 7. The 4-week average may pick up in the week to February 14, given a fall in initial, claims in that week, the survey week for the monthly report. That would be consistent with a monthly ADP gain of 60k.

We expect February’s ISM services index to slip to 52.5 after two straight months at 53.8. This would still be stronger than each month from March through November of 2025. It would also be slightly stronger than a February S and P services index of 52.3, that was the weakest since April 2025. Regional Fed services sector surveys from the Philly, Richmond, Dallas and Kansas City Feds, as well as the Empire State, were all weaker and negative in February.

We expect January’s detail to show business activity and deliveries making significant corrections from improved January readings and more modest slowings in new orders and employment to complete the breakdown of the composite.

The USD has always been a choice of haven and it made no exception in the U.S.-Iran strikes. Despite U.S. executed their decapitation tactic, it is unlikely Iran military will surrender and likely drag along with missiles and drone attacks. Such geopolitical tension will further exacerbate haven bids, USD, JPY and Gold will likely benefit the most.

On the chart, cautious trade has given way to a sharp break higher, with prices reaching strong resistance at congestion around 98.50 and the 98.55 Fibonacci retracement. A pullback is unfolding, with prices currently trading around 98.25. But daily readings have turned positive and broader weekly charts are improving, highlighting room for further strength in the coming sessions. A close above 98.50/55 will further improve sentiment and extend late-January gains towards congestion around 99.00. Just higher is the 99.25 retracement. But already overbought daily stochastics should limit any tests of this 99.00/25 range in profit-taking/consolidation.