FX Daily Strategy: APAC, June 24th

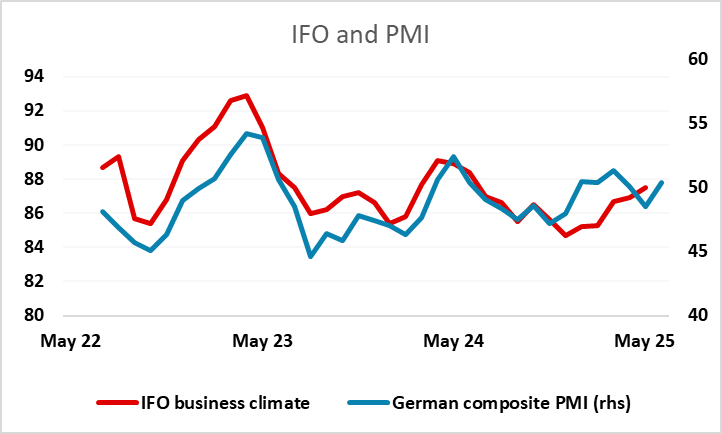

IFO to show small rise but little impact likely

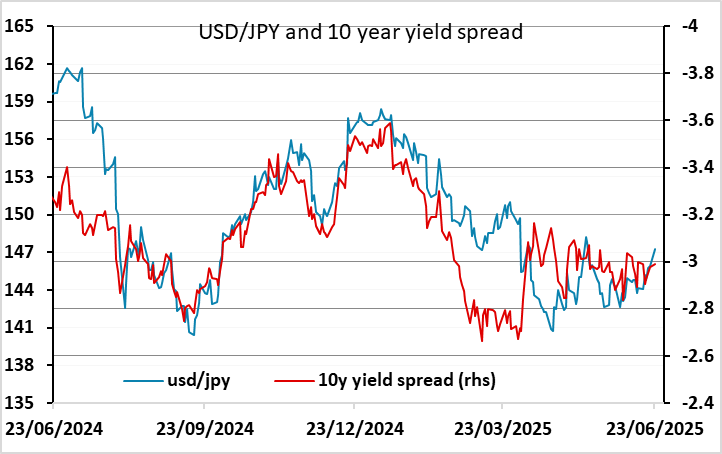

JPY can extend recovery in the absence of more geopolitical shocks

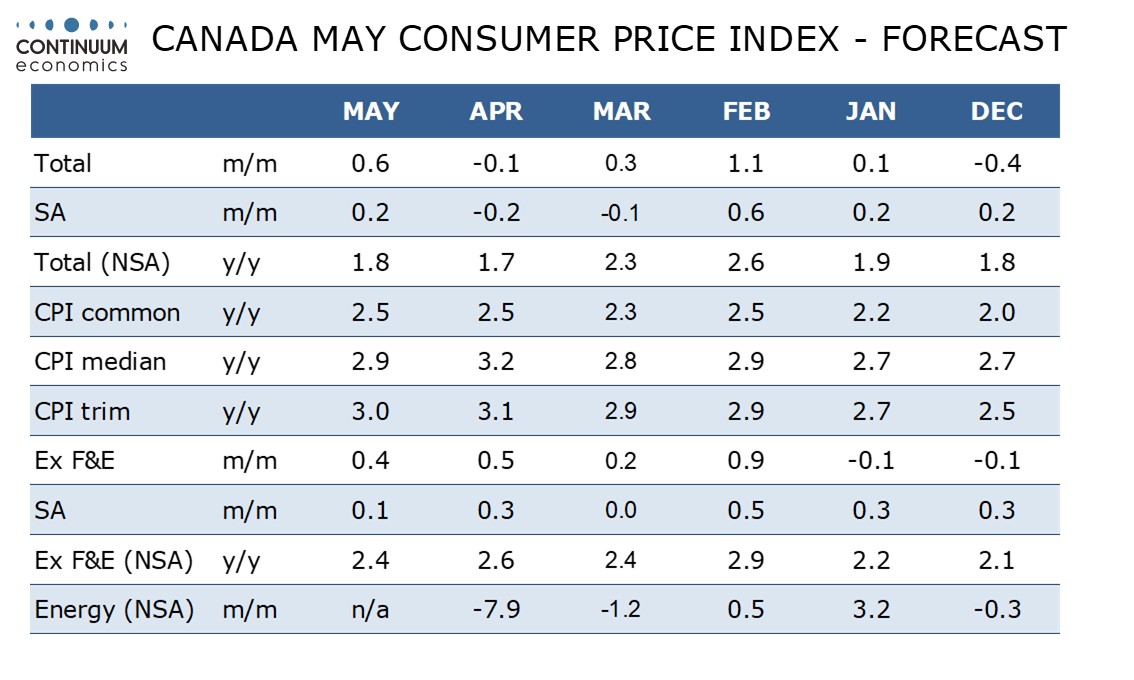

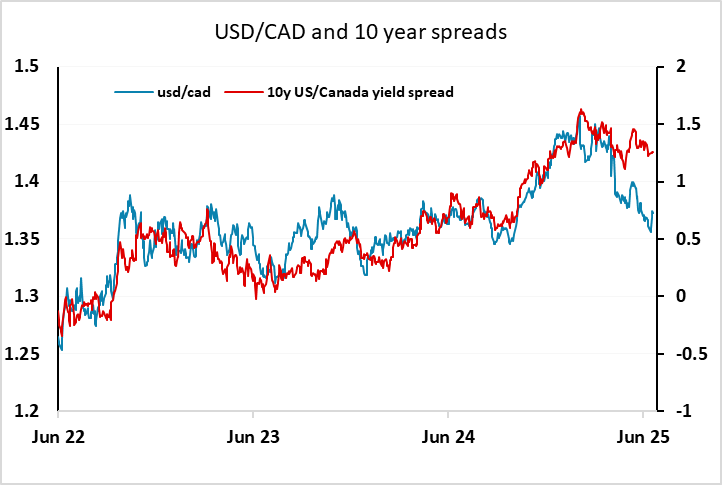

CAD upside quite limited even though CPI risks are on the upside

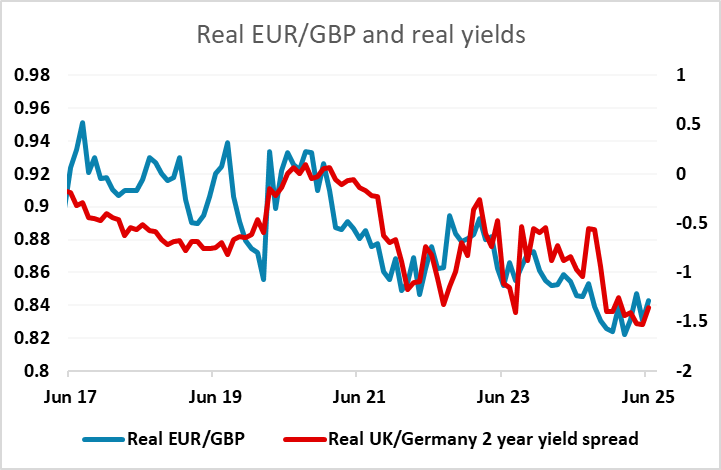

EUR/GBP could extend rally if BoE speeches sound more dovish

IFO to show small rise but little impact likely

JPY can extend recovery in the absence of more geopolitical shocks

CAD upside quite limited even though CPI risks are on the upside

EUR/GBP could extend rally if BoE speeches sound more dovish

Tuesday’s calendar is fairly quiet, with the German IFO survey in the morning of some interest, but less so given that the PMI survey has already been released. The market consensus is for a modest rise in the business climate index, and this is consistent with the PMI data released on Monday, so it seems unlikely that the IFO will provide any surprises.

The main focus will still likely be on geopolitics, with the market in the lookout for any Iranian retaliation to the US strike at the weekend. The reaction on Monday suggests that the market now expects any retaliation to be modest and probably performative, so that the US won’t feel the need to escalate. EUR/USD and the S&P 500 are both back to the levels seen at Friday’s close having seen a dip in early Asia on Monday morning. The oil price is also back to Friday’s closing levels, and only USD/JPY among the G10 USD pairs is still significantly above Friday’s closing level. This seems anomalous and we would expect USD/JPY to also return to a 145 handle by the end of Tuesday unless there are new geopolitical developments.

The May Canadian CPI data is also released and could be significant for USD/CAD. As it stands, the market is pricing in a 35% chance of a 25bp rate cut at the July 30 BoC meeting. We expect May Canadian CPI to see a marginal rise to 1.8% yr/yr from 1.7% in April, correcting a fall from 2.3% in March that was fully explained by the abolition of the consumer carbon tax. However, after an acceleration in April, we expect some slowing in the Bank of Canada’s core rates in May. This is consistent with the market consensus, so although the consensus sees an unchanged headline rate, it seems unlikely to have a notably impact. The risks may be slightly to the upside suggesting the CAD could have some scope to rally, but the USD/CAD declines since the announcement of reciprocal tariffs make it harder to see further significant losses.

There isn’t much of significance out of the US but there are speeches from BoE governor Bailey and chief economist Pill in the wake of last week’s 6-3 MPC vote. Pill has been clearly on the hawkish side so any softening of that position in the wake of the meeting could be taken as a signal that a rate cut is more likely at the August meeting than the 57% chance currently priced in. Although EUR/GBP has run a little ahead of moves in yield spreads in recent weeks, a suggestion of a further contraction in the real UK/Eurozone yield spread would support the case for the EUR/GBP rally extending towards 0.86.