FX Daily Strategy: Europe, April 23rd

Geopolitical Tension Sees No Easy Ease

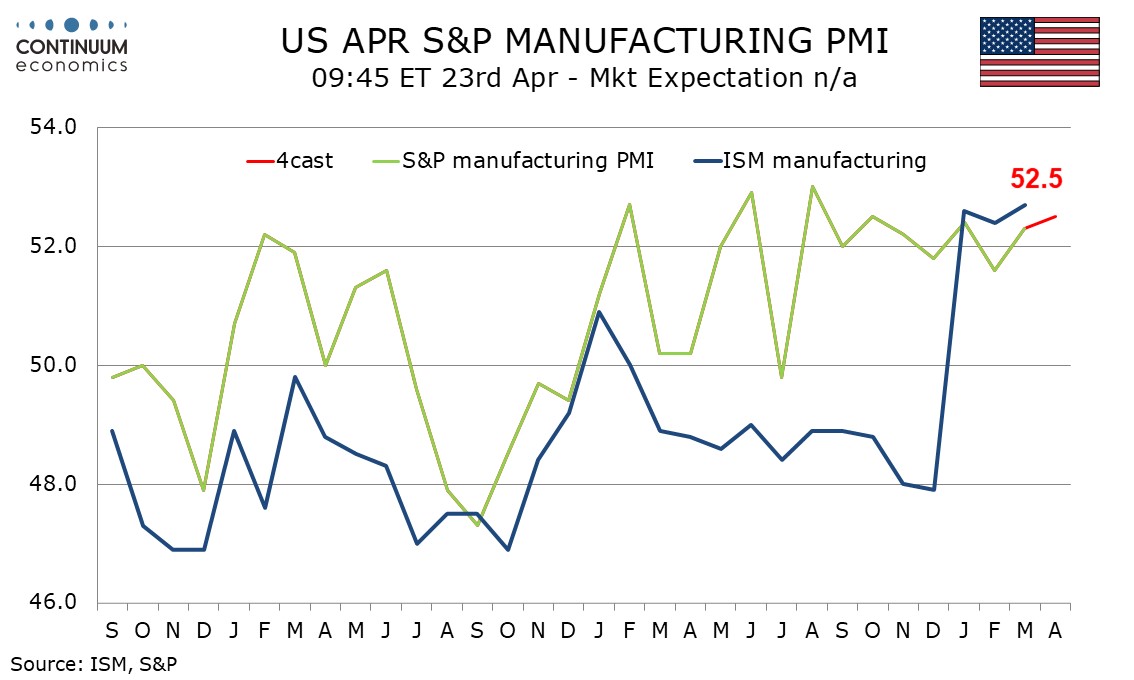

U.S. April S&P PMIs Slightly firmer despite Middle East risk

DXY Warrants Cautious trade Technically

The back and forth headlines between U.S. and Iran have shown us there is no easy path towards the geopolitical picture. More importantly, Iran seems to be having a fractured order of command where the Revolutionary Guards are saying different things with the Iran Foreign Ministry. It complicates the picture as one side seem to be up for negotiation while the other believe they will win by continue taking the Strait of Hormuz hostage. The original planned talks are heading no where for now and will rely on future development to cue the market.

We expect modest increases in April’s S and P PMIs, manufacturing to a healthy 52.5 from 52.3 and services to a neutral 50.0 after March’s 49.8 fell below neutral for the first time since January 2023. Improved Empire State and Philly Fed manufacturing surveys in April are positive signals for S and P manufacturing, though March manufacturing output lost a little momentum, contrasting strong ISM data. The scale of the ISM’s Q1 improvement may be a little overstated, but the S and P’s manufacturing index has been stable at a healthy level for significantly longer, and looks set to remain solid in April despite the risks coming from the Middle East.

The S and P services index probably sees more risk than manufacturing from the situation in the Middle East, with consumers already having looked vulnerable even before the gasoline price surge. However, we feel a stabilization near neutral is more likely than a further move into negative territory. The slowdown in the S and P services index has significantly underperformed ISM services data, though the two series are not well correlated.

On the chart, there is little change as prices extend consolidation above congestion support at 98.00. Intraday studies and oversold daily stochastics are edging higher, suggesting room for a move towards congestion resistance at 98.50. But bearish weekly charts should limit any initial tests in fresh consolidation. Meanwhile, a close back below congestion support at 98.00 will add weight to sentiment and extend late-March losses back towards 97.50. Already oversold daily stochastics could limit any initial tests in short-covering/consolidation.