FX Daily Strategy: Europe, April 27th

BoJ Hold 6-3

Could See Support for the JPY

Else Geopolitics Dominate

While we favor an April hike from the BoJ on a sustainable inflation standpoint, BoJ's Ueda seems to be worried about a potential prolong disruption of energy supply will indirectly affect wage growth. That is a reasonable call for both holding and hiking by 25bps in the April meeting, the key lies in BoJ's confidence in sustainable wage growth in the face of rising energy cost, which is likely 50-50. Nevertheless, the BoJ will guide a hike imminent and Ueda will likely sounded more hawkish in his press conference if we are not seeing an April hike. Suck will provide minor support for the JPY in a short run.

As per forecast, the BoJ has kept rates unchanged at 0.75% in the April meeting with three votes dissent that is looking for another 25bps hike. There hasn't been any changes to BoJ's stance of more hike but the geopolitical tension in Middle East may have a temporary negative effect on wage growth in Q2. It led the BoJ to revise their economic forecast for 2026 lower before rebounding in 2027. Inflation forecast is revised higher to 2.5-3% in 2026 before rotating lower in 2027 and reaching target at 2028.

On the chart, there is little change as prices drift narrowly following retest of the recent highs at 159.85/160.00. This is expected to cap and see prices extend consolidation within the broad ranging action between the 160.00/158.00 area. Lower high sought to further pressure support at the 159.00 level. Below this will see room for retest of the 158.50/158.00 congestion. Lower still will see room to strong support at 157.50. Break here will confirm a top in place at the 160.46 March current year high and see room for deeper pullback to retrace gains from the January low.

The back and forth headlines between U.S. and Iran have shown us there is no easy path towards the geopolitical picture. More importantly, Iran seems to be having a fractured order of command where the Revolutionary Guards are saying different things with the Iran Foreign Ministry. It complicates the picture as one side seem to be up for negotiation while the other believe they will win by continue taking the Strait of Hormuz hostage. The original planned talks are heading no where for now and will rely on future development to cue the market.

Market participants are cautiously optimistic, which will likely lead to strong correction on negative headlines, even false ones. The complication regarding the Strait of Hormuz will likely drag on. The physical supply disruption will soon hit the market if no easing is seen before June. The DXY will likely be volatile in the meantime with back and forth headline.

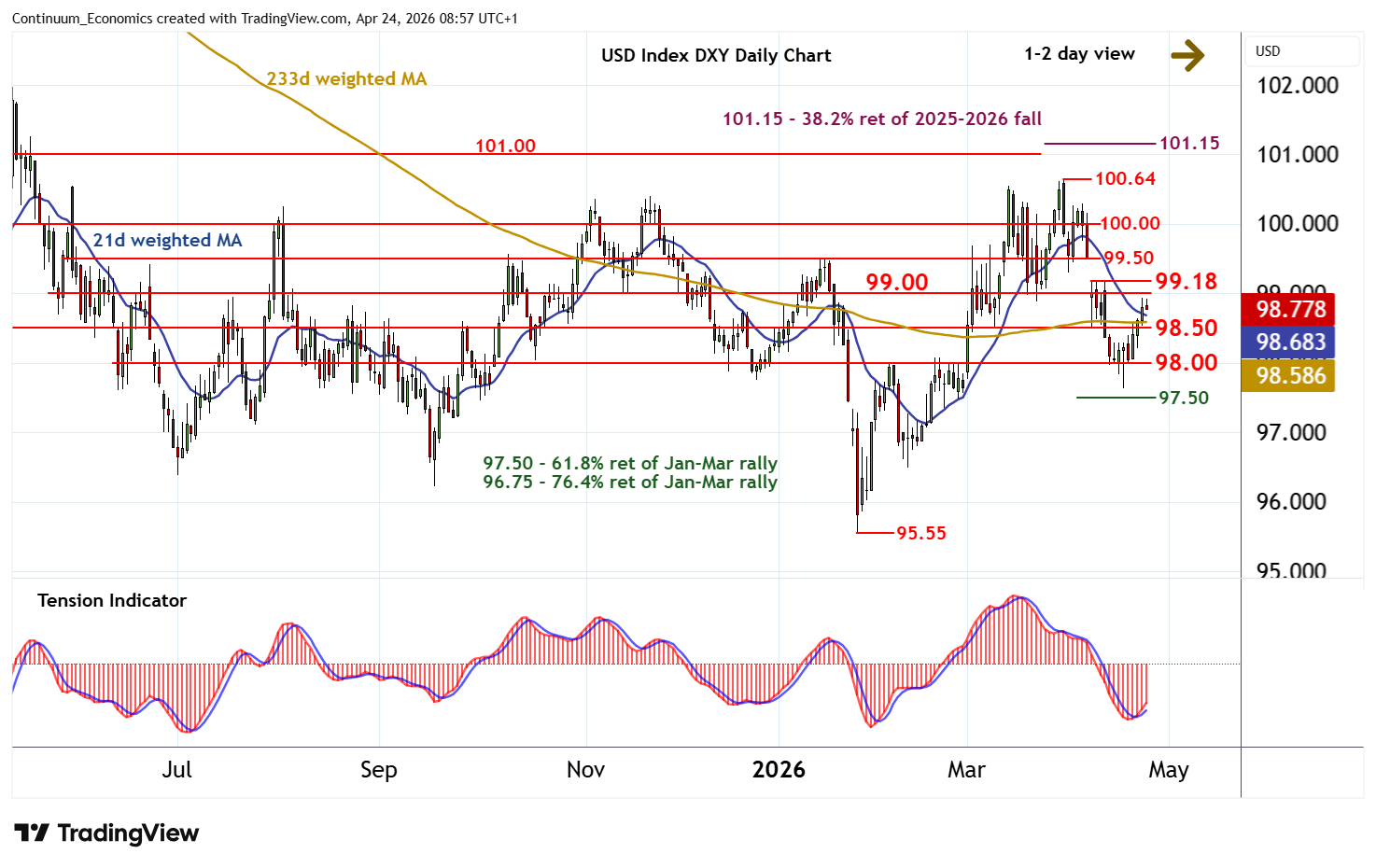

On the chart, daily stochastics and the daily Tension Indicator continue to rise, however, highlighting potential for continuation towards strong resistance at congestion around 99.00 and the 99.18 high of 18 April. But negative weekly charts should limit any immediate tests of this range in renewed selling interest/consolidation. Meanwhile, support remains at congestion around 98.50. A close beneath here will turn sentiment neutral and prompt fresh consolidation above further congestion support at 98.00.