FX Daily Strategy: APAC, January 15th

JPY may get a brief reprieve but intervention still likely to be needed

GBP downside risks on GDP

USD firm and unlikely to be derailed by data

JPY may get a brief reprieve but intervention still likely to be needed

GBP downside risks on GDP

USD firm and unlikely to be derailed by data

The JPY managed a modest recovery through North American hours on Wednesday, which likely takes the pressure off the BoJ to intervene on Thursday. But recent history suggests this is likely to be a short-lived reprieve. While it is possible that external events like the Iran situation or a Supreme Court ruling on the legality of tariffs have a negative impact on USD/JPY, the last year has shown that the underlying JPY downtrend is unlikely to break without official action. Certainly, the JPY typically will benefit from a weaker equity market, and it is possible we will see that in the short term, as a correction is overdue. But the JPY also typically benefits from narrowing yield spreads in its favour and rising equity risk premia, but has failed to do so in the last year. To turn the trend, the BoJ are likely to have to cap USD/JPY with intervention to change the risk/reward characteristics in the market. All the typical metrics and fundamentals suggests USD/JPY should be lower, so if traders perceive the USD/JPY upside to be capped, we are likely to see a significant correction. But if the BoJ stay out of the market, and correction is likely to be seen as a buying opportunity before too long.

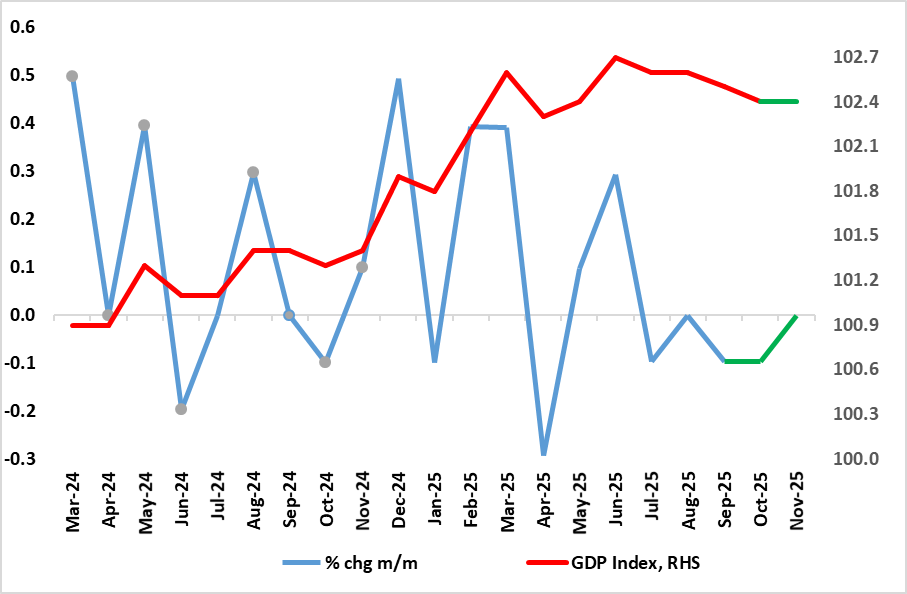

The UK focus will be in the November GDP data, after a very weak run in recent months. UK GDP has hardly moved since March and this became even clearer with the last (October) GDP release, the question being whether weakness is getting more discernible and significant. Indeed, it has fallen in three of the last four months and we see no improvement in the looming November numbers with a flat m/m outcome envisaged. Admittedly, a further recovery from a cyber-attack at JLR vehicle manufacturing does provide modest upside risks, but these are offset by wet and warm weather swings, which seemingly accounted for the already-reported soft November retail sales figure. This points to Q4 GDP possibly falling by 0.1% q/q; indeed, a non-negative outcome would need growth of over 0.1% in both Nov and Dec GDP figures. A negative outcome would be below the BoE’s flat expectation, this revised down last month from its previous 0.3% forecast. This weakness chimes nevertheless with what surveys still suggest (especially construction), namely the economy is at best moving sideways, and very probably likely to contract further.

UK GDP

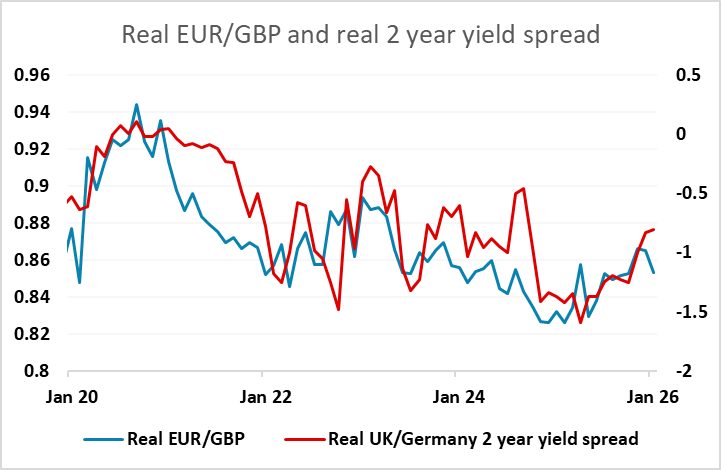

For GBP, this suggests some downside risks, as the market is anticipating a 0.1% m/m rise. In any case, the gradual narrowing of the real yield spread at the front end of the curve suggests there are already some upside risks for EUR/GBP. These would be more likely to be realised on weaker UK data, especially in a more risk negative environment.

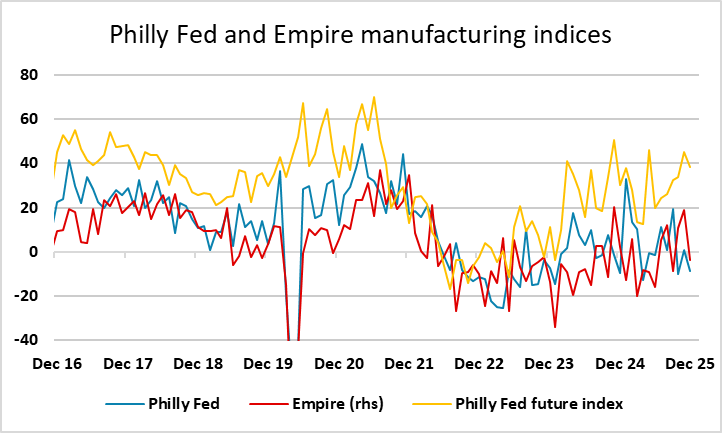

The US has jobless claims and the Philly Fed and Empire manufacturing surveys on Thursday, and these look unlikely to undermine perceptions of a strong US economy in Q4. Other things equal, we would expect the USD to stay firm on the back of this data. There has been no sign of any pick-up in initial claims, and the Philly Fed and Empire surveys have been choppy but fairly neutral, although the Philly Fed future index has been stronger of late, and suggests some upside risks. We doubt the USD’s fortunes on Thursday will be determined by data, with geopolitics likely to be a factor.