U.S. February Trade Deficit remains very high, Initial Claims still low

Initial claims remain low at 219k, in fact surprisingly so at 219k from 225k, though continued claims at 1.903m from 1.847m are the highest since November 2021, and that could be a warning of a labor market slowing, though the 4-week average is creeping up only slowly.

The initial claims data covers a week two weeks after the one in which March’s payroll was surveyed, while continued claims cover the week after the payroll survey week. The labor market stool looks solid, and we expect a healthy 165k payroll increase in March, though downside risk is building.

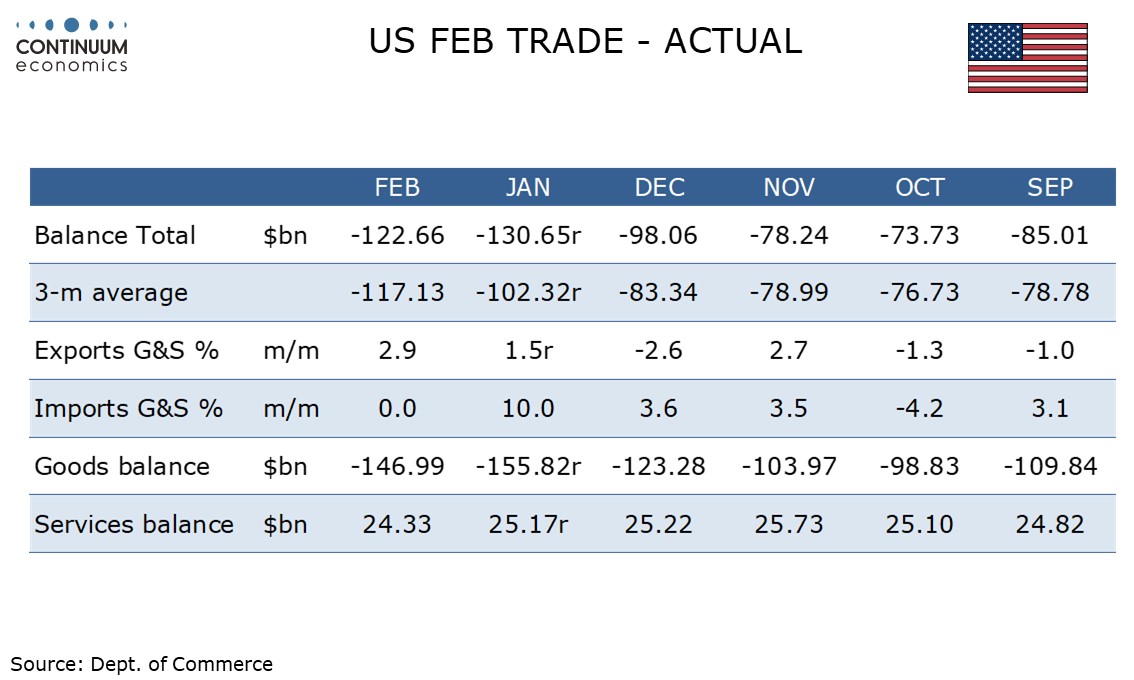

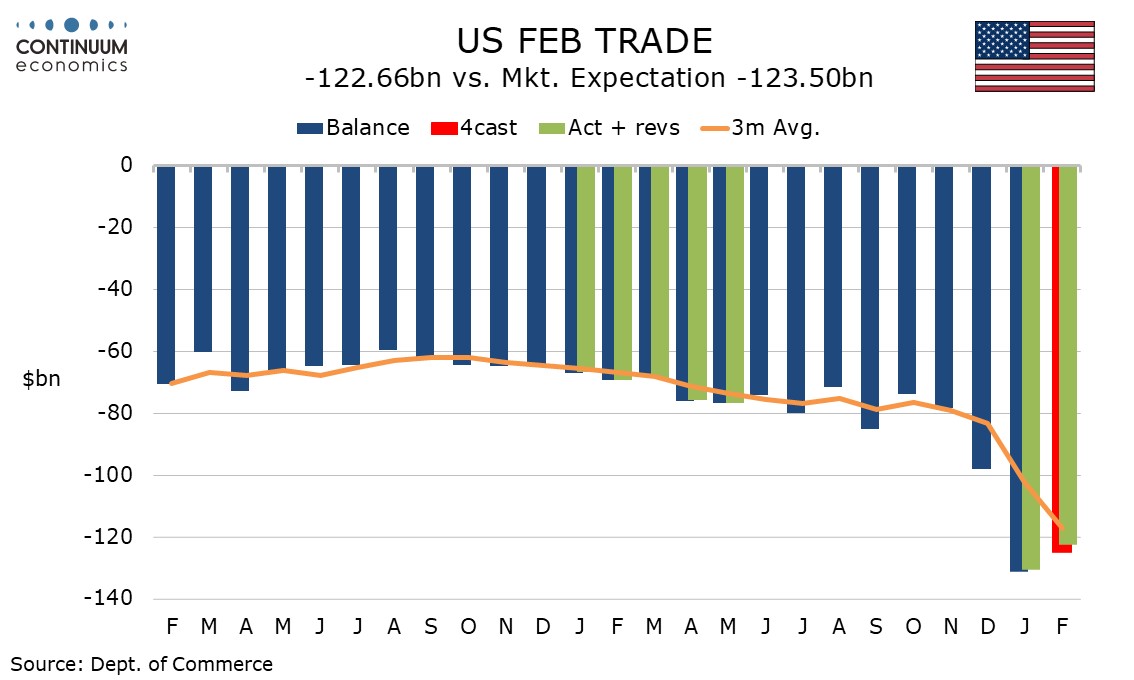

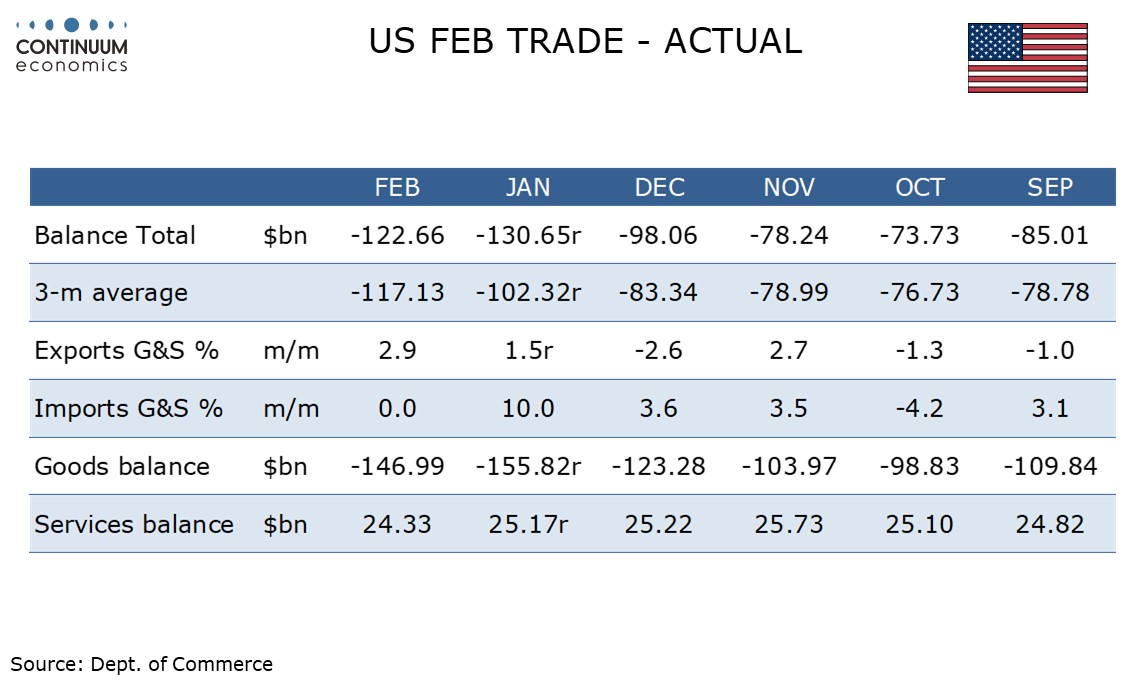

February’s trade deficit of $122.7bn from $130.7bn in January is as suggested by advance goods data, with both deficits dramatically above the $98.0bn seen in December. Exports rose by 2.9% after a 1.5% January increase while imports were unchanged after a 10.0% surge seen in January.

Goods data show exports up 4.8%, stronger than a 4.1% gain seen in the advance data, but goods imports with a 0.2% decline were consistent with the advance data. Services saw a 0.4% fall in exports but a 0.7% rise in imports. Boycotts of US travel by Canadians in particular may be having an impact.

January’s imports surge was led by finished metal shapes, which saw a small correction lower in February, but still stand at $65.9bn in the year to date compared to $6.0bn in the first two months of 2024. Nonmonetary gold imports in the year to date stand at $6.3bn compared with $1.8bn in the first two months of 2024. These components explain most of the dramatic trade deterioration in Q1.

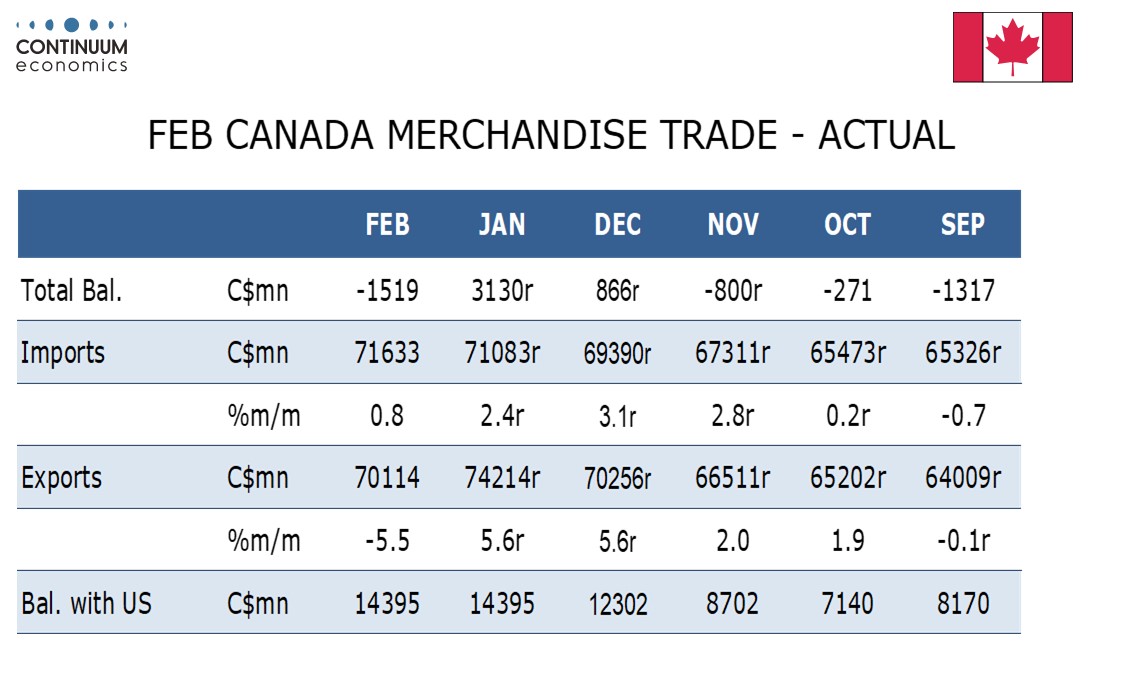

Canada’s February trade balance swing back into deficit at C$1.519bn from a large $3.13bn surplus in January. Exports fell by 5.5% after a 5.6% January rise while imports rose by 0.8% after a 2.4% January rise. Trump threats to impose tariffs on day one of his term, while subsequently delayed, seem to have inflated January exports, though the February exports decline was not confined to the USA.