FX Daily Strategy: Europe, January 30th

FOMC, BOC and Riksbank meetings in focus

Major surprises unlikely, but we favour a mild USD, and CAD downside bias

Riksbank cut rates as expected

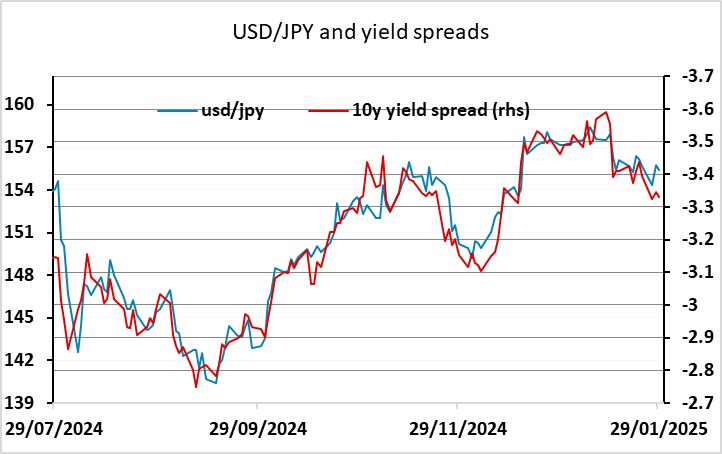

USD/JPY continues to look the most vulnerable

GDP data may have more impact than the ECB meeting

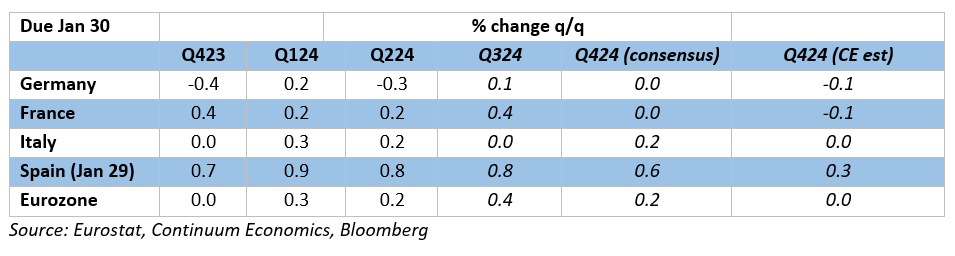

European GDP risks are modest after stronger Spain data

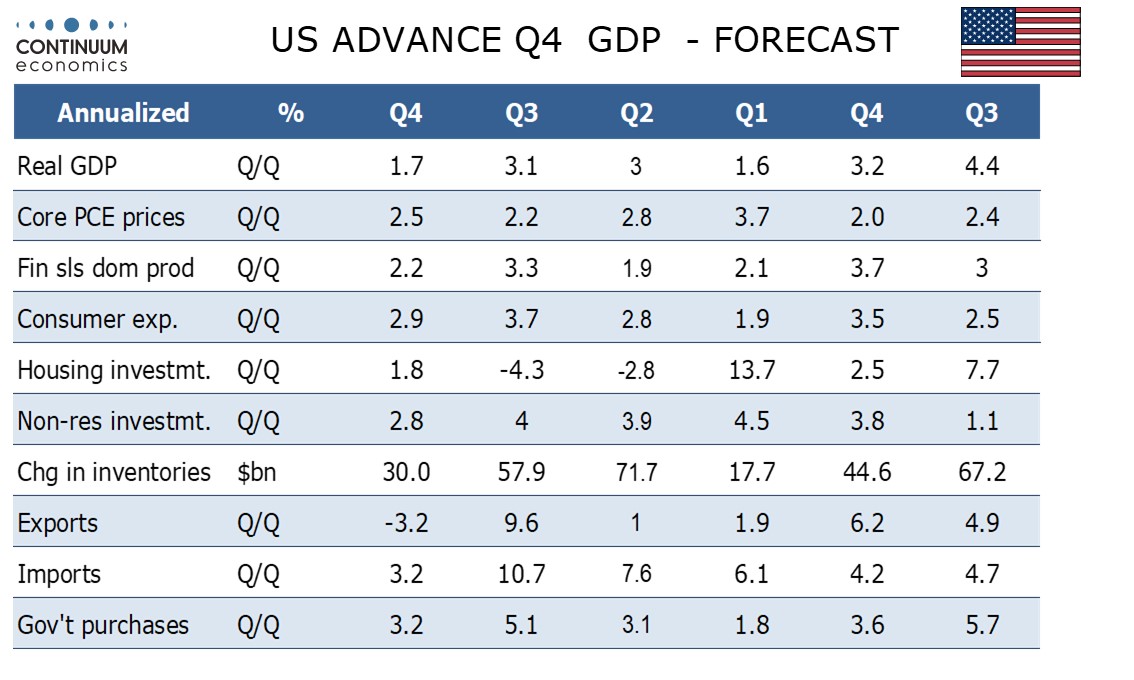

US GDP to come in lower than published consensus after big trade deficit

USD risks consequently on the downside

Thursday sees the ECB meeting, but this seems unlikely to deliver any surprises and there may be more potential for reaction to the GDP data from both the Eurozone and the US.

Divergent EZ GDP Picture Still Clear in Q4?

The Eurozone GDP numbers will be first on the agenda. We see a below consensus outcome of zero in q/q terms (consensus 0.1%), chiming with what have been weak business survey results. But there are upside risks as actual output data have actually been firmer into mid Q4. But if the data is perkier, the relevant question would be the extent to which any solid GDP figure may reflect (involuntary) inventory building and/or import weakness. What is likely however, is that the GDP numbers will continue to suggest an EZ economy that is still diverging as Germany stutters while Spain prospers, with the Spanish data already released on Wednesday showing an above consensus 0.8% rise. The EZ data may therefore be mildly EUR negative, but the impact is unlikely to be large with the miss probably small, and the market focused on the subsequent ECB meeting.

Potentially more significant could be the US GDP data. After surprisingly weak December advance goods trade and retail and wholesale inventory data on Wednesday we have revised our forecast for Q4 GDP down significantly, now expecting a 1.7% annualized rise rather than our previous estimate of 2.6%. The gain may have been stronger without strikes and hurricanes in early October. Q1 data is also likely to see some adverse weather effects early in the quarter. We expect core PCE prices to see a modest acceleration to 2.5% from Q3’s 2.2%, assuming a 0.2% rise in December. Overall PCE prices will be slightly slower at 2.3% but the overall GDP price index slightly firmer at 2.6%, lifted by subdued export prices marginally outperforming import prices.

The published market consensus is for a rise of 2.7% q/q, but most forecasters will be revising down their numbers after the trade and inventories data, so the true consensus is somewhat lower. The Atlanta Fed GDPNow indicator, which is a nowcast of the GDP numbers and is generally well followed, was revised down to 2.3% from 3.2% in response to the data. However, neither the USD nor US yields declined in response to the data, so there is some downside risks if the numbers are weaker than the published consensus as we expect. The fact that a rising trade deficit is partly responsible should also be seen as USD negative, although inasmuch as it encourages Trump to go ahead with tariff increases it could work the other way. Even so, we see USD downside risks on the data, particularly against the JPY as lower yields should have the clearest impact on US/Japan yield spreads.

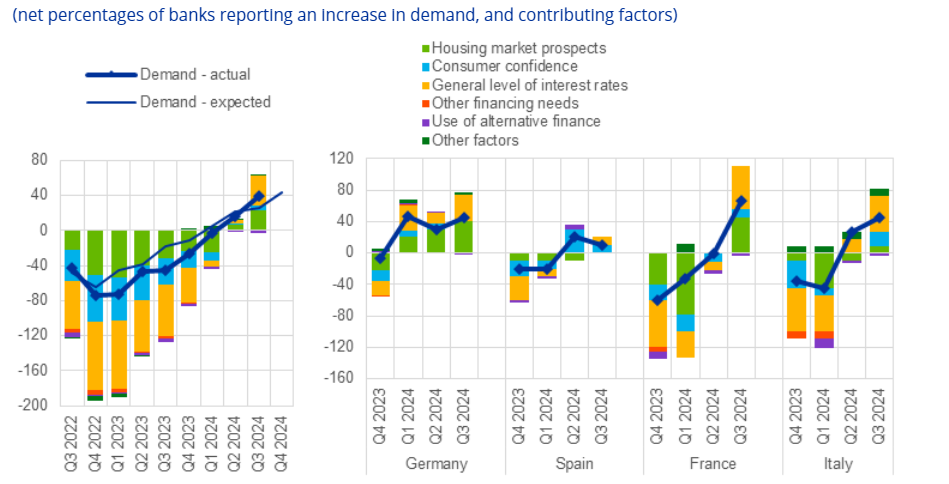

Household Loan Demand Reflecting Better Interest Outlook?

The ECB meeting is less likely to have a significant impact, as a 25bp cut is fully priced in. Admittedly, the door will be left open for further cuts but hints may be made that amid less-soft survey data, possibly including better bank lending signs, the discount rate is approaching a terminal if not a neutral outcome. It is clearly the case that the ECB is discussing what constitutes a neutral rate, but this is occurring more covertly rather than within the confines of the Council meetings. Regardless, we still think that the economy will undershoot ECB thinking and inflation will continue to soften. All of which implies around four 25 bp cuts in H1 this year, with an ensuing around-neutral 2% policy rate. This is broadly what is priced into the market, with the policy rate priced to be 2.03% at the December meeting. Unless the ECB show a clear protest to market thinking, expect the reaction to be mild.