FX Daily Strategy: APAC, June 4th

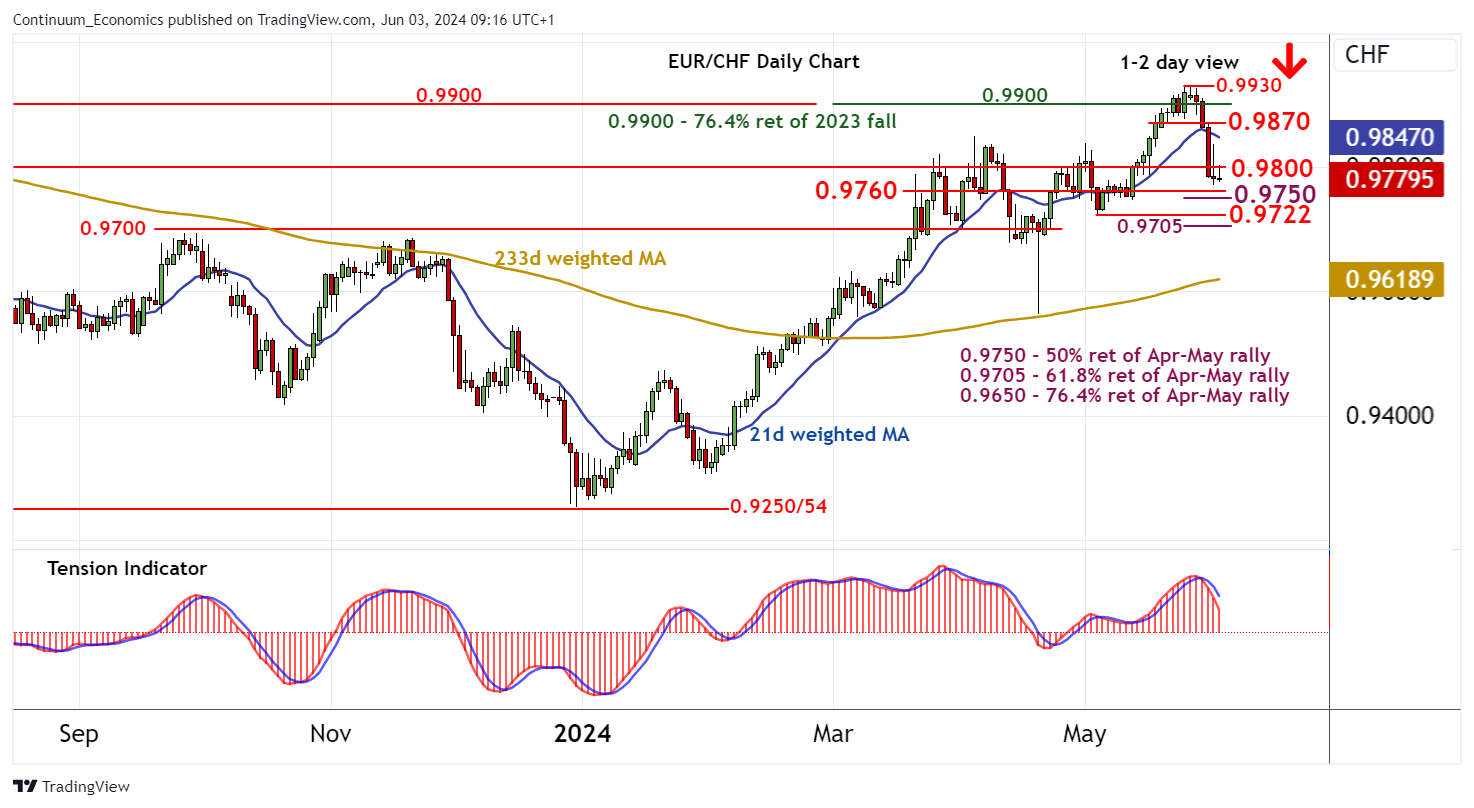

Focus on Swiss CPI on Tuesday

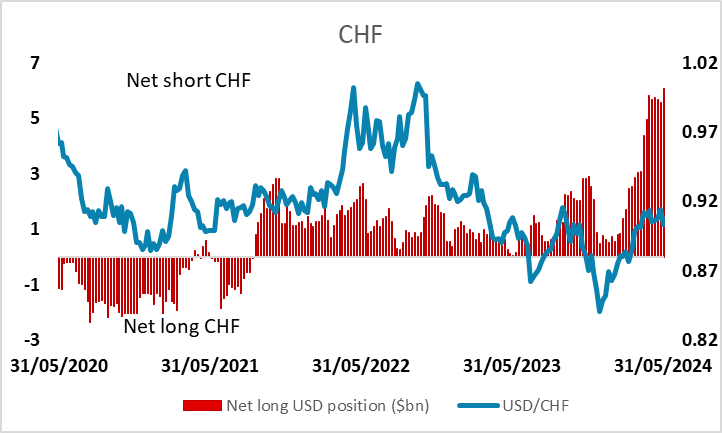

CHF may still have further to rise and positioning looks very short

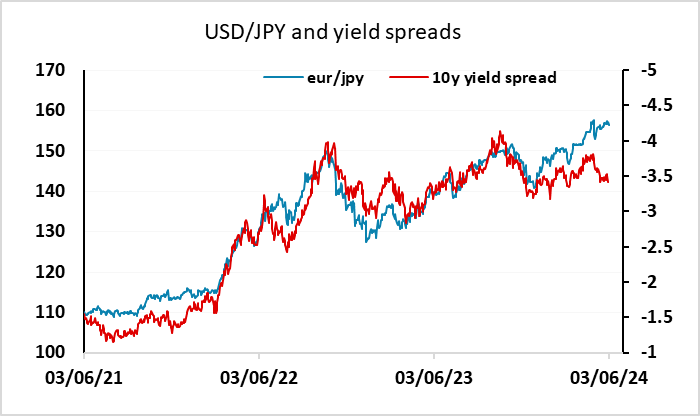

JPY still has scope to benefit from declining yields in the US and Europe

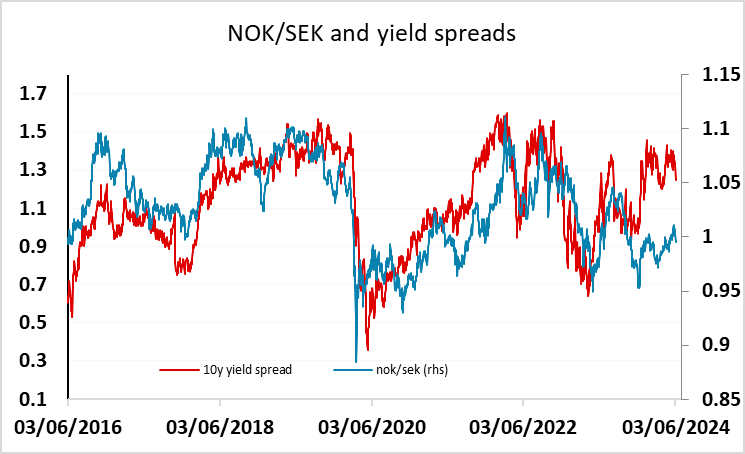

Scandis look attractive but NOK may be the better bet

Focus on Swiss CPI on Tuesday

CHF may still have further to rise and positioning looks very short

JPY still has scope to benefit from declining yields in the US and Europe

Scandis look attractive but NOK may be the better bet

Tuesday is a relatively light calendar, with little that it likely to be market moving. There is Swiss CPI in Europe, which could be significant in view of the stronger CHF of late and the strong Swiss GDP data that triggered it. The CHF weakened against the EUR fairly steadily from the beginning of the year before EUR/CHF peaked on May 24, but has been pulling back since and EUR/CHF continues to press to the downside. The near term risks do look to be on the low side, partly because the ECB is set to catch up with the SNB’s lead by cutting rates this week. While the SNB was first, the ECB (and others) will in the end cut rates more, so there is likely to be yield movement in favour of the CHF against the higher yielding currencies. This is of limited significance since the CHF doesn’t tend to be driven much by yield spreads, but could reverse the weakness seen since the SNB cut rates on March 21, when EUR/CHF opened below 0.97 and traded up to near 0.98.

Another factor suggesting upside risks for the CHF is positioning, with the latest CFTC data showing the larger net short speculative CHF position on record. Many of these positions will be held against the USD, but could be pressured by the USD/CHF break below 0.90.

Otherwise, there isn’t a lot on the calendar to move markets, although there will be some interest in the IBD/TIPP economic optimism index and the JOLTS data, in view of the upcoming US employment report and the soft ISM manufacturing index reported on Monday. The USD came under pressure after the ISM, and USD/JPY in particular looks vulnerable if US yields stay lower and the ECB cut rates this week as expected, particularly if the equity market fails to benefit as it did on Monday. USD/JPY risks remain heavily weighted to the downside given current yield spreads, but JPY strength would become much more likely in a more risk negative market.

Otherwise there isn’t a great deal on the calendar, with German unemployment not typically market moving. There is French budget data, which may garner a little attention after the France downgrade at the weekend, but is still unlikely to be market moving. One notable move on Monday was the rise in the SEK, which gained more than 0.5% after the stronger than expected Swedish PMI. SEK gains have taken it a little above the level suggested by yield spreads, but there is some attraction in the SEK as a European recovery play, as it does tend to benefit from relative European growth improvement. However, from a yield spread perspective, the NOK is much more attractive, with the dip below parity on Monday likely to be seen as a long term buying opportunity.