USD, EUR, JPY flows: USD firm but upside limited

USD firm as US yields rise but limited scope for further gains near term. German CPI the focus

German CPI data will be the main focus this morning, ahead of the Eurozone CPI data tomorrow. The preliminary Spanish, French and Italian CPI data was already released last week. French and Italian CPI were on the soft side of consensus, so the published consensus numbers for Germany and the Eurozone are probably on the high side of real expectations, although the Spanish numbers were slightly on the firm side.

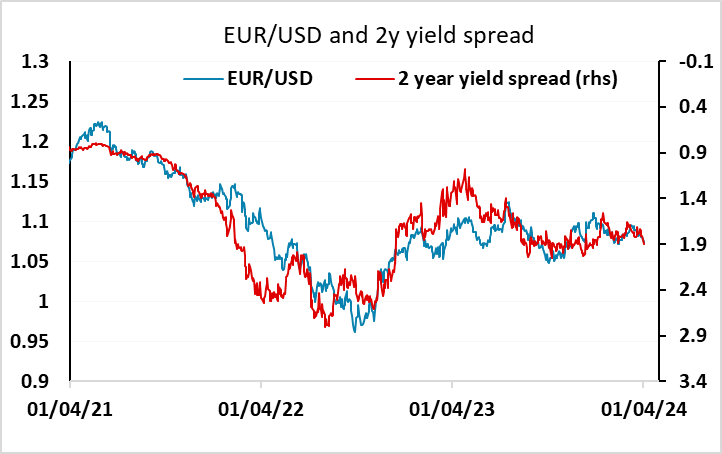

EUR/USD is already under some downside pressure with the USD making general gains on Monday as US yields rose, helped by stronger than expected ISM manufacturing numbers, although US yields had already started to rise ahead of the data, reportedly due to some unwinding of month end related long positioning. The rise in US yields was quite sharp, with 2 year yields up 10 bps on the day, and the decline in EUR/USD has correlated with that move. Some hawkish Fed comments over the last week has also helped, and the market is now pricing 20bps less Fed easing than ECB by the end of the year. But it still looks hard to price in a lot more ECB easing, with a June cut already priced in and 3 ½ rate cuts priced by year end, so although there is downside pressure on EUR/USD, the lows of the year at 1.0695 are likely to present significant short term support.

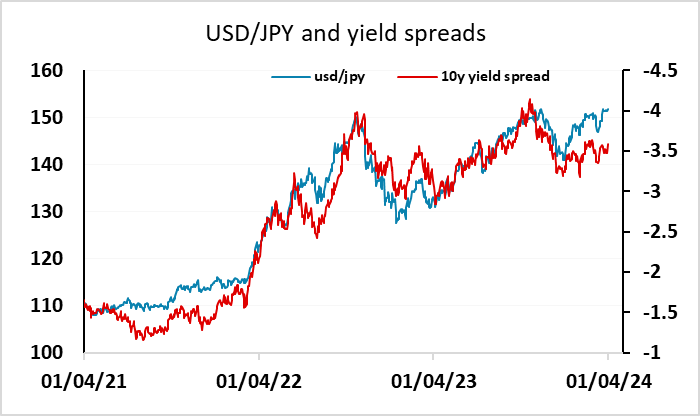

The rise in US yields has also maintained upside pressure on USD/JPY. The 151.97 34 year high that was traded last week is under pressure but has not yet been breached, with the market playing grandmother’s footsteps with the BoJ as the Japanese authorities continue with verbal intervention. We would still see upside for USD/JPY as quite limited here, with yield spreads well short of the highs seen in October last year, but a major turn is still likely to require a less risk positive market tone.