U.S. March Consumer Confidence resilient to higher inflation expectations, February job openings trend near flat

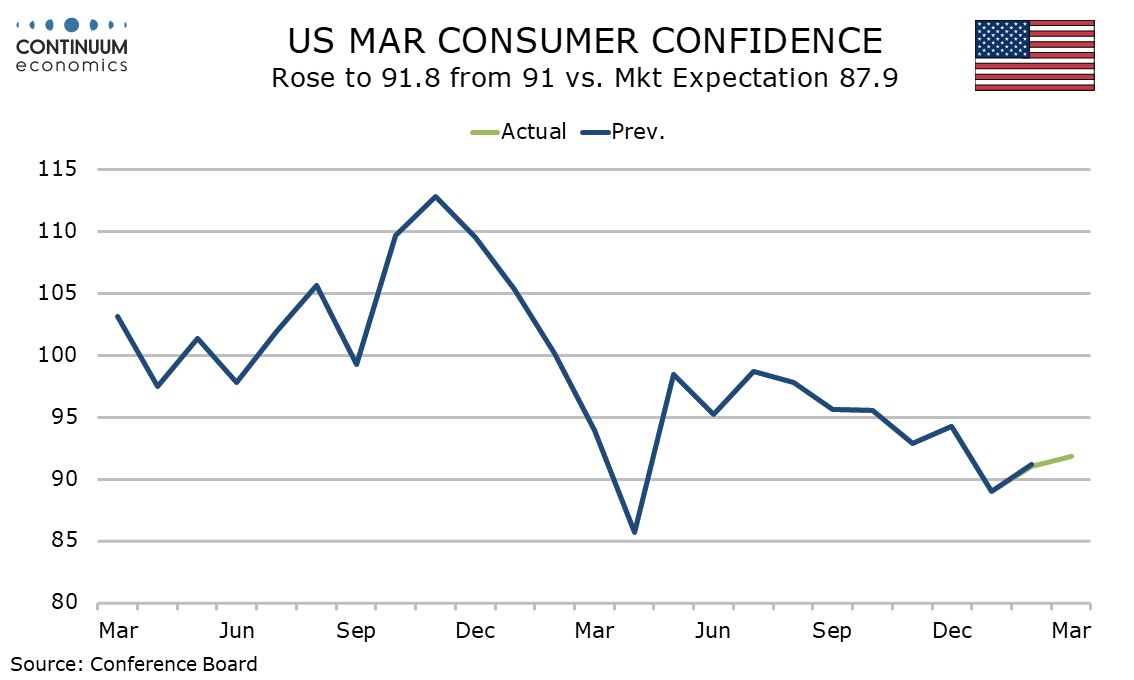

Despite a bounce in inflation expectations, the Conference Board’s consumer confidence index is surprisingly stronger in March at 91.8 from 91.0, a second straight rise though not fully erasing a January dip. February JOLTS data on job openings suggests a fairly stable labor market picture.

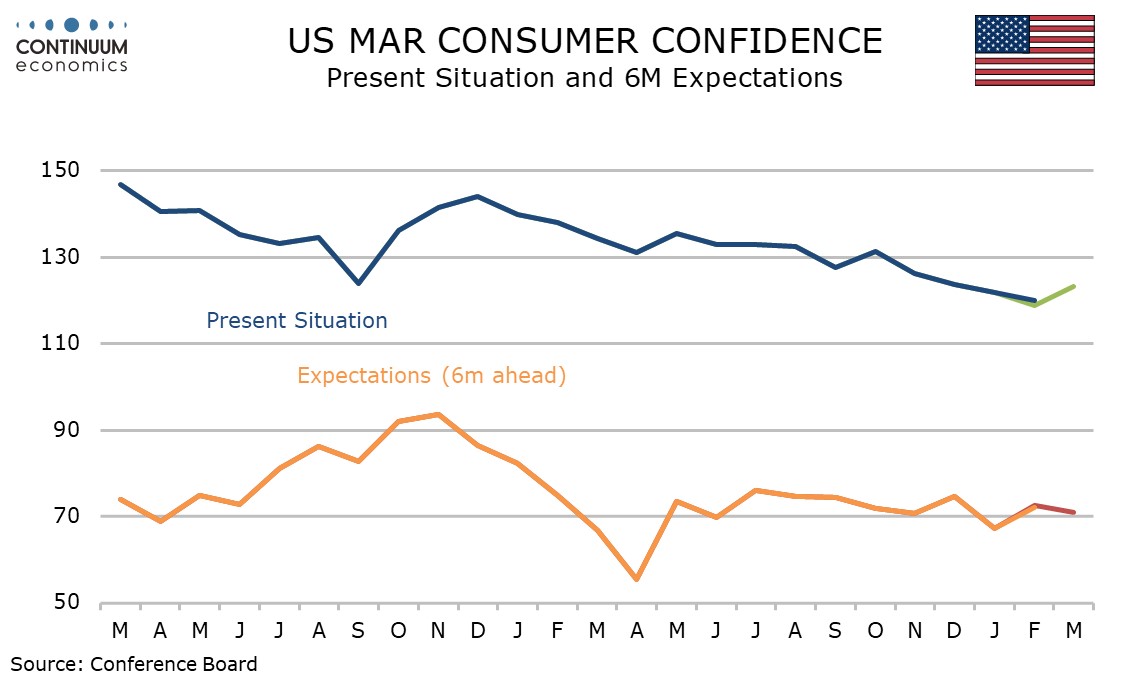

The consumer confidence detail shows a contrast between a stronger present situation at 123.3 from 118.7, but weaker 6-month expectations at 70.7 from 72.6, the latter probably influenced by energy prices but both remain within their recent range.

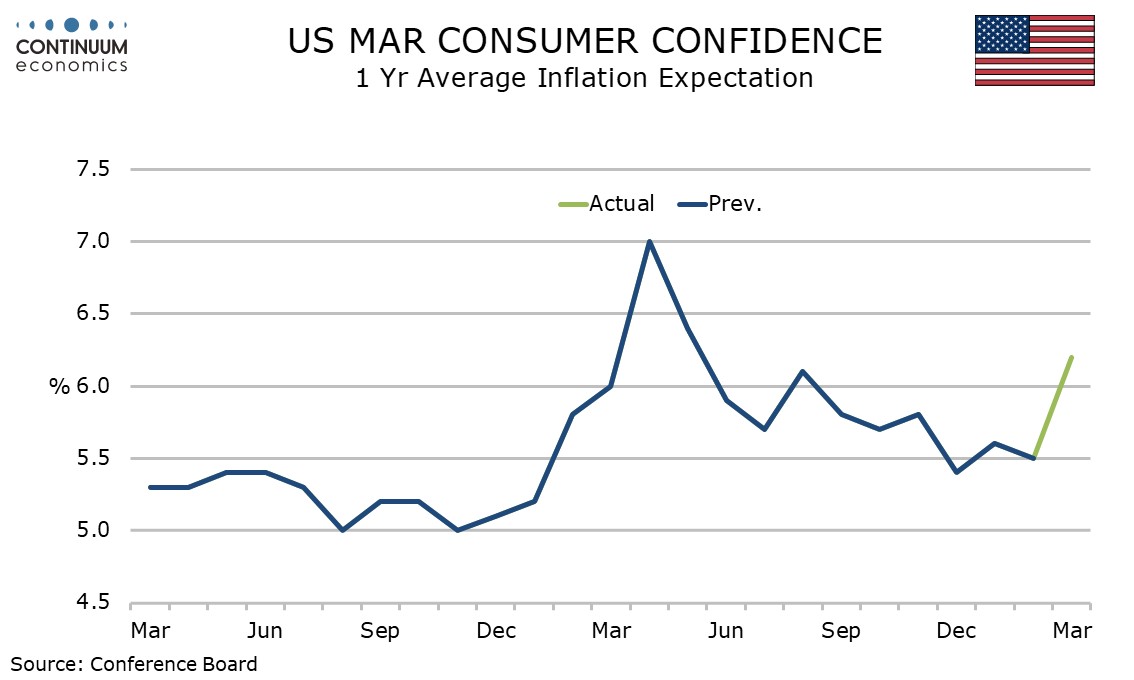

The 12-month average inflation expectation of 6.2% from 5.8% is the highest since May 2025 while the median rose to 5.2% from 4.5%. The average seems to be boosted by a minority of very pessimistic respondents, but the gap narrowed in March.

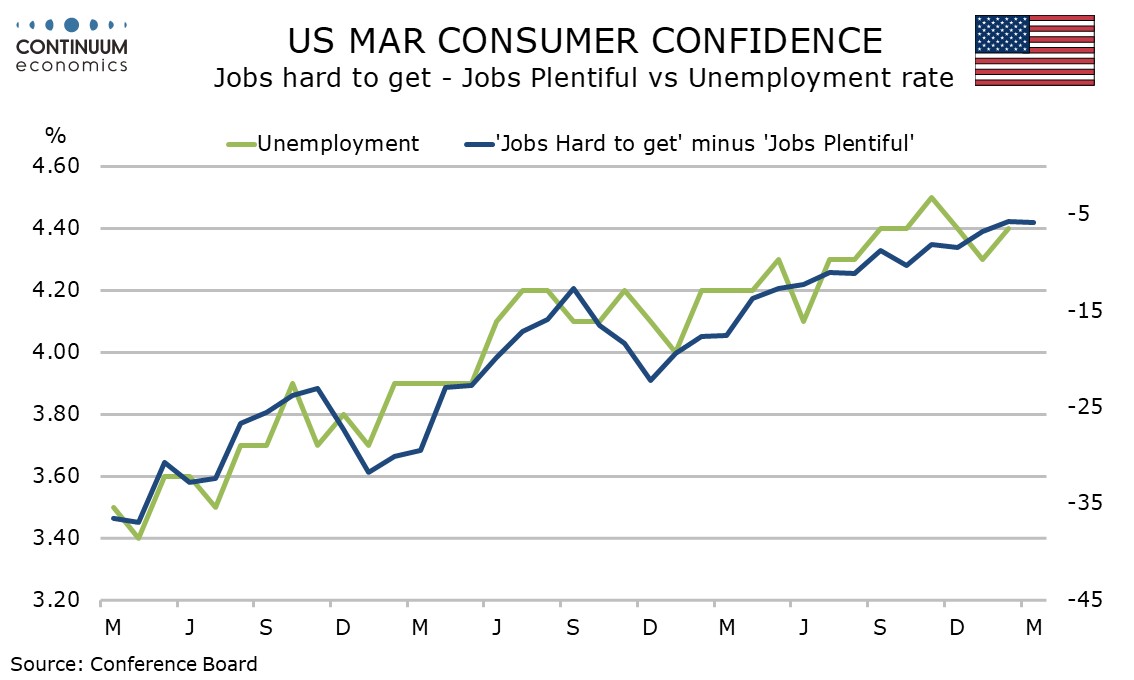

The proportion seeing jobs as plentiful exceed those seeing them as hard to get by 5.8%. up from 5.7% in February but the last two months have seen a significant slowing.

Improved perceptions of business conditions also supported the present situation index. Higher tax refunds given tax cuts passed in 2025 may be offsetting some of the damage done by higher gasoline prices, though the full impact of the latter has probably still to be seen.

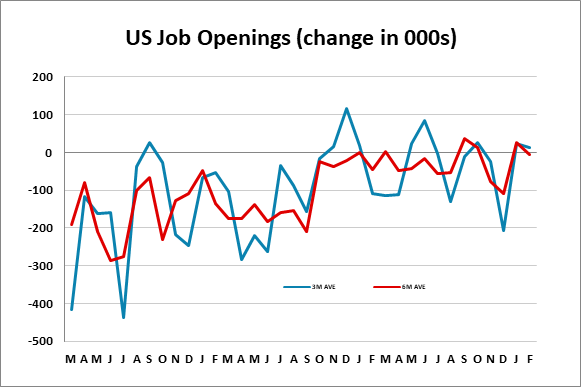

JOLTS data shows a 358k decline in job openings in February but with January revised to a rise of 690k from 396k the net picture is little changed. Three and six month averages are back to near neutral from negatives in December.

Elsewhere the JOLTS report shows hiring down by 498k but separations down by only 173k, explaining weakness in February’s payroll. Most of the fall in separations came from a 157k fall in quits, which is not a positive sign.