Published: 2024-10-30T16:54:59.000Z

Preview: Due November 5 - U.S. September Trade Balance - Deficit rebounding after August narrowing

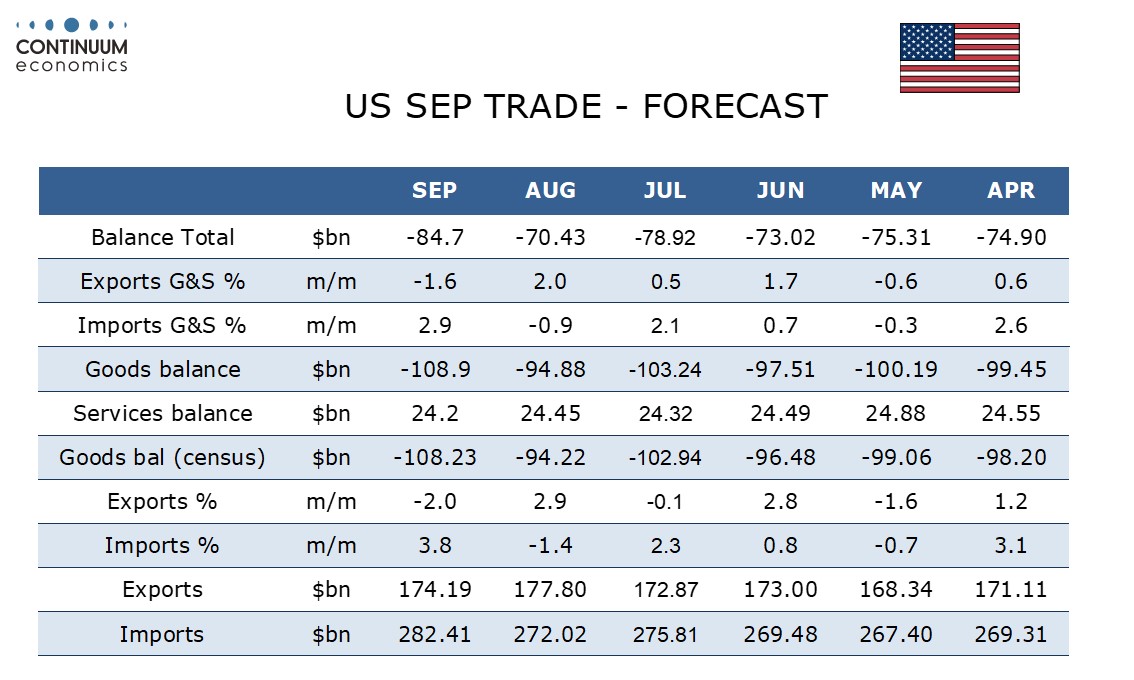

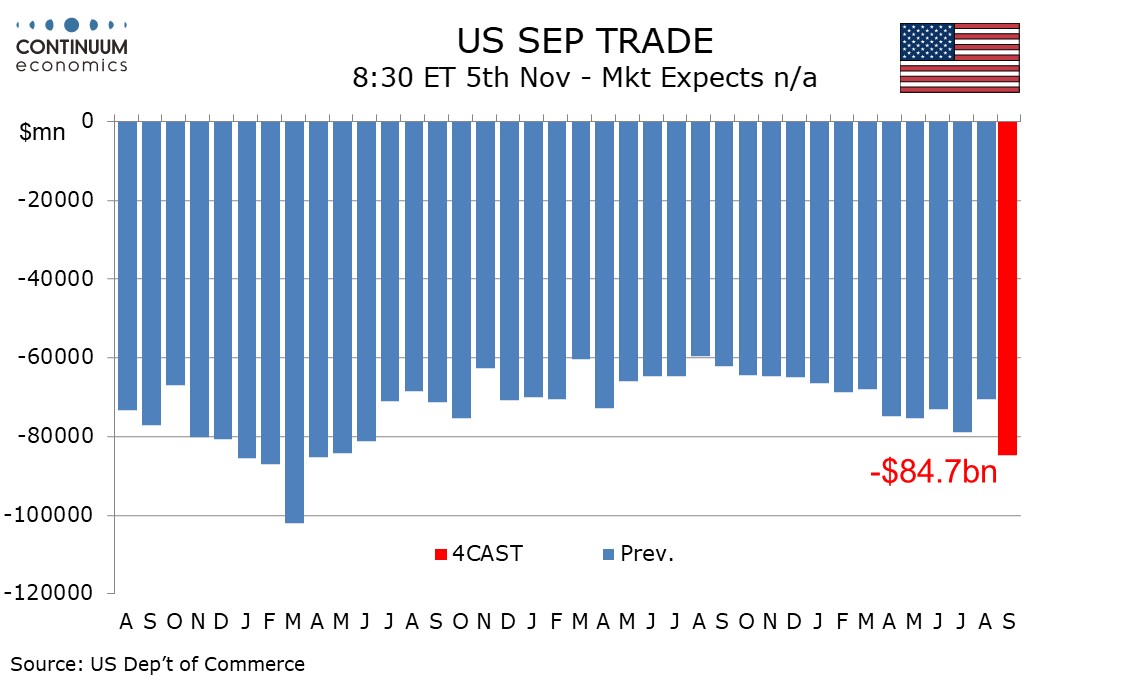

2

We expect a September trade deficit of $84.7bn, up from $70.4bn in August and the widest since April 2022. We expect exports to fall by 1.6% after a 2.0% August increase and imports to bounce by 2.9% after a 0.9% August decline.

We expect goods to show a 2.0% decline in exports and a 3.8% increase in imports in line with advance goods data already released. This will restore a negative trend after August saw a significant narrowing of the deficit.

We expect a marginal decline in the services surplus with exports down by 0.9% and imports down by 0.8%. Declines in both series would be unusual but consistent with the assumptions made for September in the Q3 GDP report.