FX Daily Strategy: Asia, May 1st

Tokyo CPI Should Remain Below 2%

USD/JPY Threatens Further Break

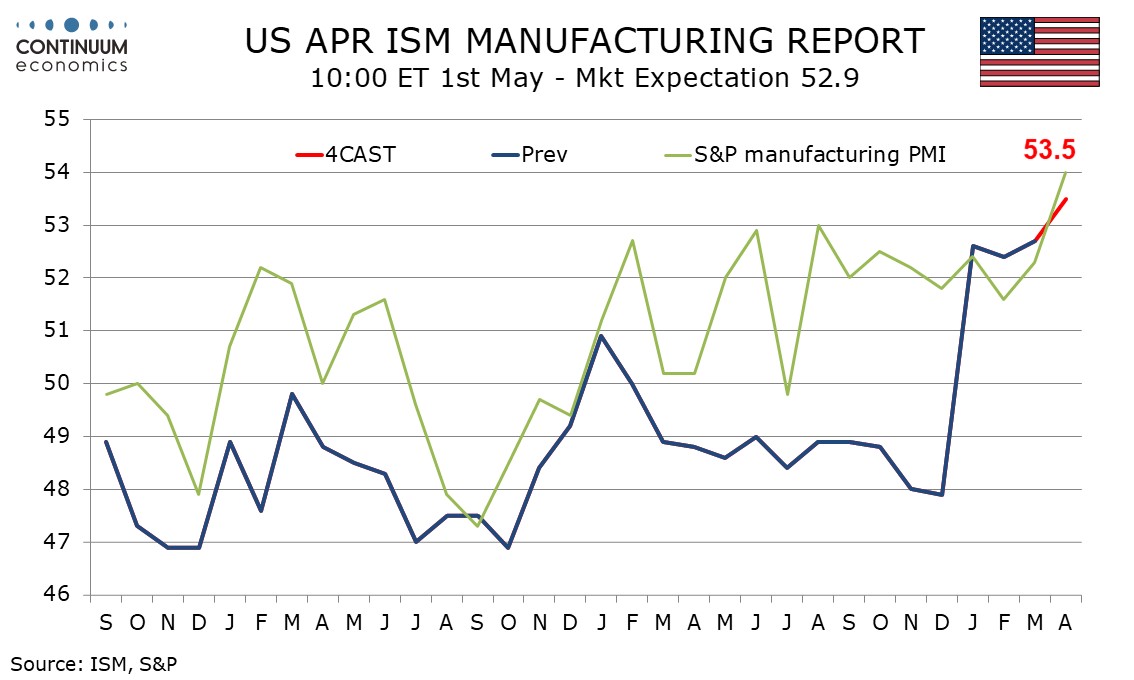

U.S. April ISM Manufacturing Highest composite and prices paid since 2022

Tokyo headline CPI is expected to arrive below target range of 2% as energy stimulus continue to cushion the oil spike due to Middle East disruption. Core-Core inflation will likely stay above target range while core CPI could be close to 2%. Until wage growth is shown to be affected by energy prices, we believe the underlying inflation momentum is unfazed and should see sustainable inflation trajectory intact.

However, with the lack of hawkish committment from the BoJ. USD/JPY is likely to search for higher grounds as haven bids favor USD. The lack of strong commitment from the BoJ may disappoint hawks that have priced in a June/July hike. If they realize such maybe inappropriate from the drag in Middle East, market pricing maychange rapidly and cutting the legs off JPY.

On the chart, bounce from the 159.00 level has seen gains to extend the broader gains from the 157.50 low of 17 April to retest the March current year high at 160.46. Reaction here see prices unwinding overbought intraday studies but a later break cannot be ruled out. Clearance here will turn focus to the 161.95 multi-year high of July 2024. Meanwhile, support is raised to the 160.00/159.85 recent April highs which should now underpin. Break here will ease the upside pressure and see room for return to the 159.00 support.

Despite risks coming from the Middle East, we expect April’s ISM manufacturing index to increase to 53.5 from 52.7, delivering a fourth straight clearly positive reading and the highest level since June 2022. Signaling a stronger reading are improved data from the S and P manufacturing index, Philly Fed and Empire State surveys.

These surveys suggest a bounce in new orders after two straight slowings, we expect to 55.0 from 53.5. We expect production to be little changed at 55.0 from 55.1 and only marginal increases in employment and inventories, to still negative levels. Delivery times may be inflated by war-related supply shortages and we expect a rise to 61.0 from 58.9, completing the breakdown of the composite.