FX Daily Strategy: Europe, March 27th

US trade data likely to be the main focus

Lower deficit may still imply weaker growth and lead to a weaker USD

Norges bank decision a close call but NOK biased higher

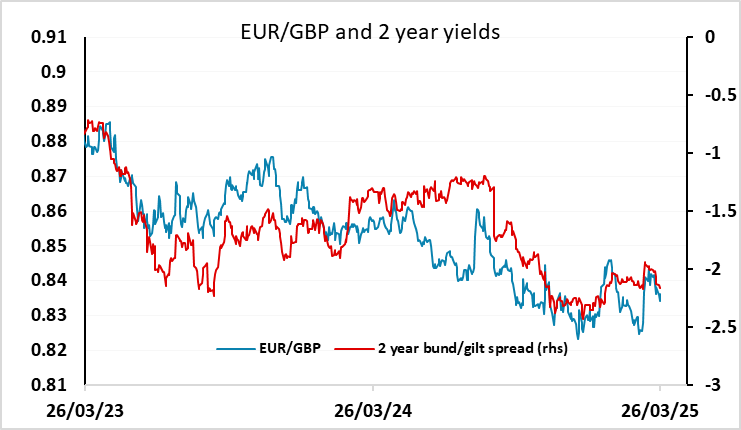

GBP resilient but still biased lower

US trade data likely to be the main focus

Lower deficit may still imply weaker growth and lead to a weaker USD

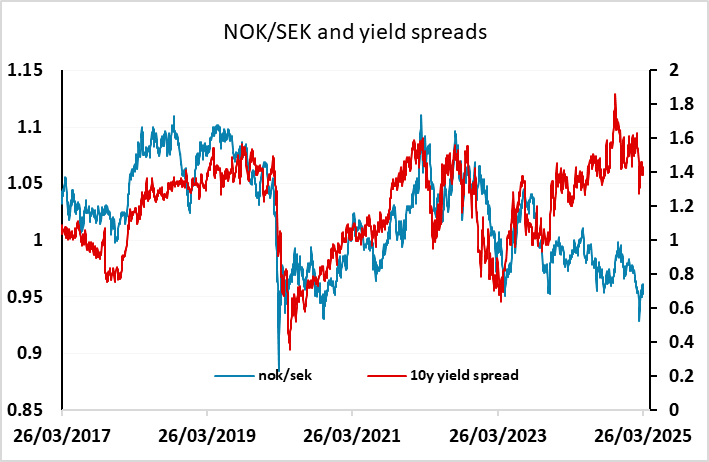

Norges bank decision a close call but NOK biased higher

GBP resilient but still biased lower

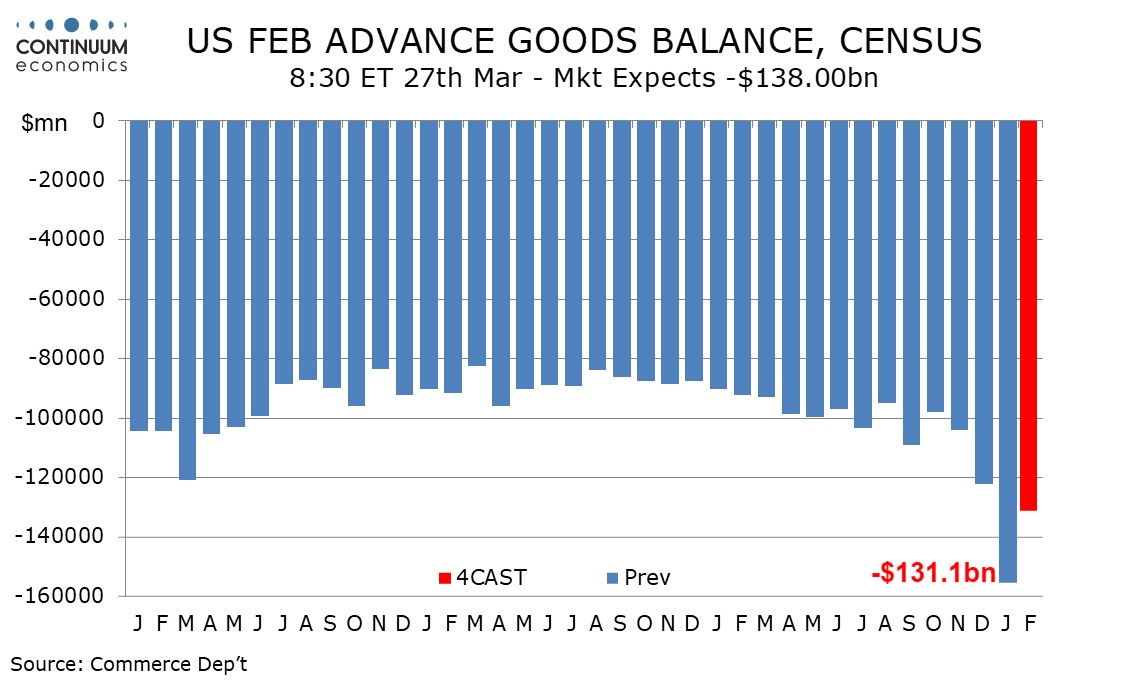

Thursday sees mostly second tier US data, but there will be more interest than usual in the trade balance. We expect a February advance goods deficit of $131.1bn, down from January’s dramatic import-led surge to $155.6bn, but still above December’s $122.1bn, which itself was a record high until January’s data was released. The focus is clearly on imports which surged in January in an attempt to beat threatened tariffs. February is likely to see a correction, particularly in fixed metal shapes which explained 57.5% of January’s rise, but with tariffs still threatened imports may remain above normal levels in February. Released with the advance goods data will be advance February retail and wholesale inventories, which if strong could offset downside GDP implications coming from the trade data. January inventory data however provided only a limited offset, with wholesale inventories up by 0.8% but retail inventories unchanged.

The consensus expectation for trade is for a slightly larger deficit than we expect, so the USD may not suffer despite these extremely wide goods trade deficits. However, USD strength on Wednesday following the better than expected durable goods orders data looked a little overdone, and trade and inventory data that suggests weak Q1 GDP numbers could still prove USD negative, with USD/JPY in particular looking very extended.

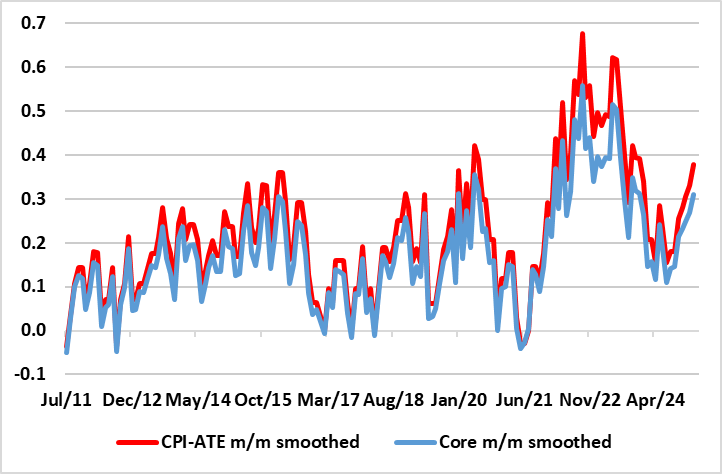

Higher Short-term Price Pressures Led by Food Surge not Included in Core Measure of Norwegian inflation

Higher Short-term Price Pressures Led by Food Surge not Included in Core Measure

Source: Stats Norway, CE, smoothed = 3 mth mov avg

In Europe there is a Norges Bank rate decision which looks like a close call. Recent inflation data have questioned whether the well flagged rate cut will now be delivered. Clearly, inflation has moved further above target, but has been boosted by a series of one-offs and also by the CPI basket re-weighting. The question is whether the (hawkish) Norges Bank judge price pressures appear to be more persistent than it previously assumed. The odds of a cut may now be near balanced. Regardless, under any scenario, the rate path will be revised significantly higher. We see the Norges Bank deferring the move, but it is a close call. The market is pricing a cut as around a 35% chance, and is pricing just one and a half cuts over the year. A no change decision should be supportive for the NOK, with NOK/SEK in particular looking ripe for gains with the SEK outperforming yield spreads both against the EUR and NOK of late, and yesterday’s Swedish confidence data showing some weakening.

GBP was a focus on Wednesday but in the end showed relatively little reaction to the UK fiscal statement, although it did soften modestly after the weaker than expected CPI data. We still see downside risks for the pound, with the weaker UK growth forecasts and further fiscal tightening increasing the chances of greater BoE easing, helped also by the softer CPI data. A May rate cut looks to us more likely than the 45% chance currently priced in. MPC dove Dhingra speaks on Thursday, but given her dovish status, we doubt there will be much impact form her speech. GBP, along with the other higher yielders, remains most vulnerable to general weakness in risk sentiment, which looks more likely to come from US data.