FX Weekly Strategy: Asia, May 4th-8th

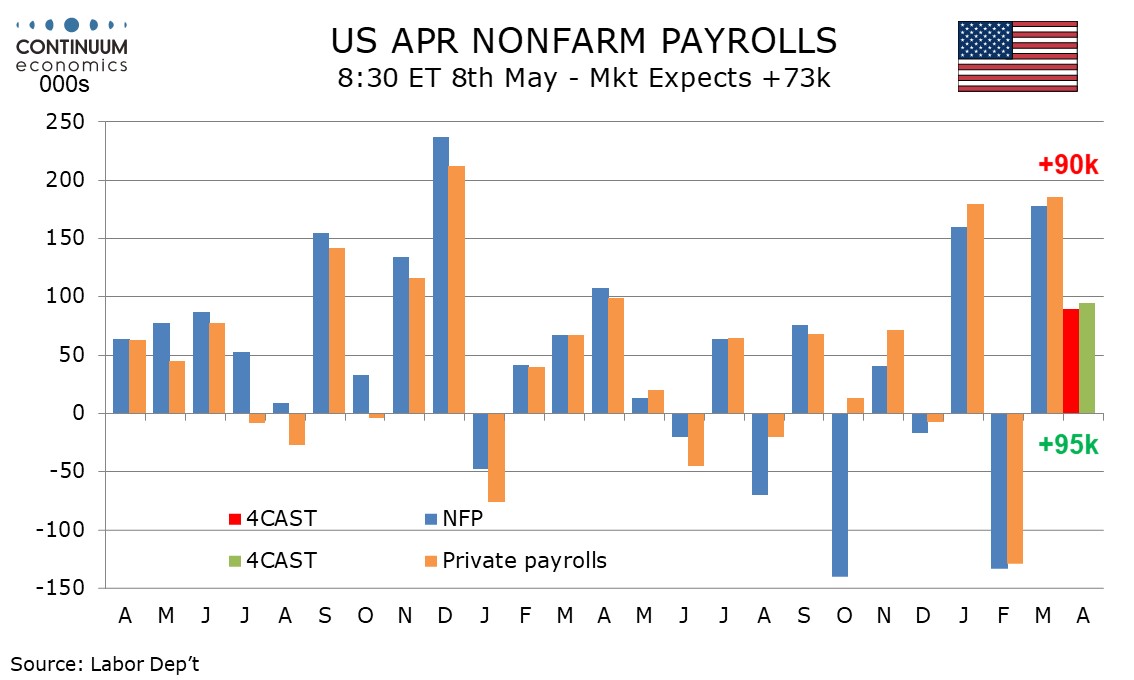

U.S. Non-Farm Payrolls Not as strong as March but some positive signals

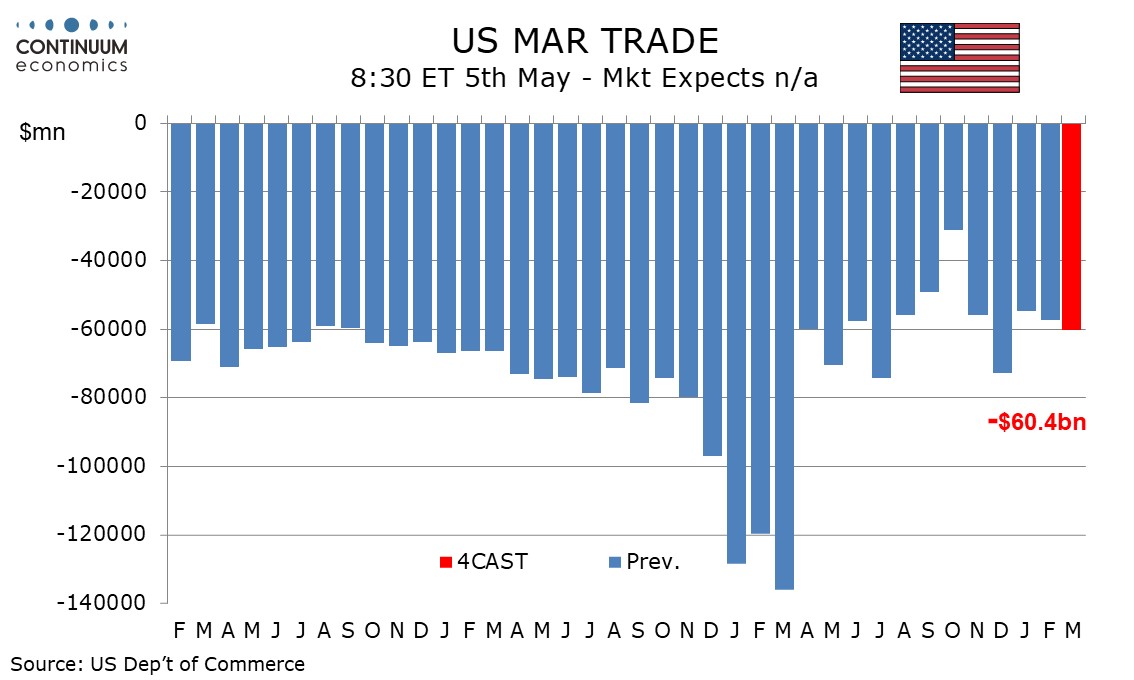

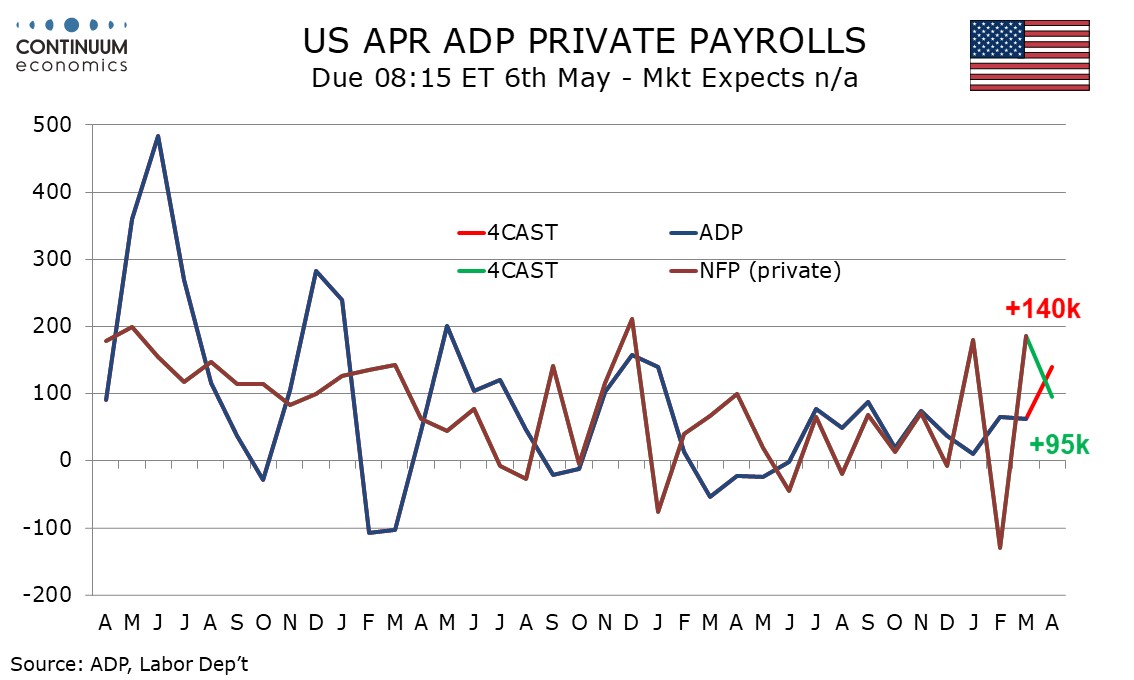

And Other U.S. Data

Sweden Riksbank On Hold and Most Likely Still For Some Time

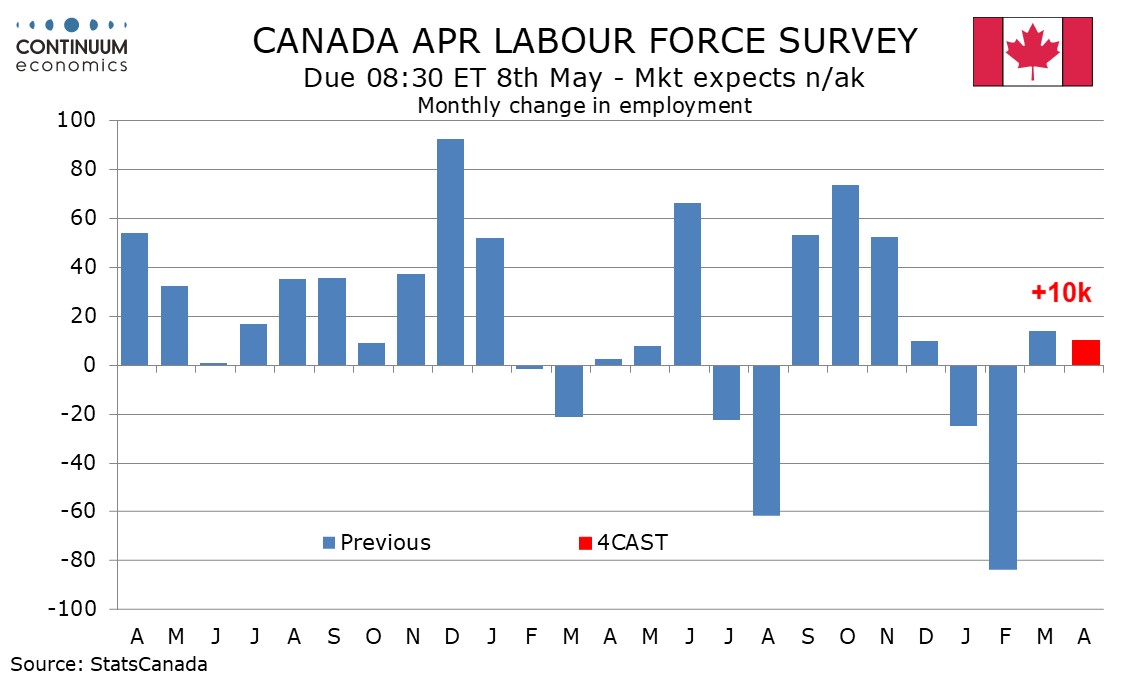

Canada April Employment A modest gain with stable unemployment

We expect April’s non-farm payroll to rise by 90k overall and by 95k in the private sector, less strong than in March but implying some improvement in trend. We expect unemployment to slip to 4.2% from 4.3% and an in line with trend 0.3% increase in average hourly earnings. March’s 178k increase in non-farm payrolls was flattered by 32k returning strikers, who exaggerated a 133k decline in February. February’s weakness was also in part due to bad weather. March bounces in weather-sensitive sectors such as construction and leisure/hospitality will be difficult to match in April. However our forecast is significantly higher than the average of February’s and March’s payrolls, and also a 4-month average of 47k (57.5k for private payrolls) which includes a strong January and a weak December too.

We expect a March trade deficit of $60.4bn, up from $57.3bn in February. We expect gains of 1.5% in exports and 2.1% in imports, extending respective February gains of 4.2% and 4.3% respectively. Advance goods data has already been released showing gains of 2.5% in exports and 3.3% in imports. Expects were mostly strong but consumer goods were an exception. Autos were particularly strong in a broad based gain in imports. This would leave a goods deficit of $89.0bn, up from $84.6bn in February.

We expect a 140k increase in April’s ADP estimate for private sector employment, which would be the strongest since a matching gain in January 2025. It would not be quite as strong as a 4-week average of 39.25k in the weekly ADP employment report for the weeks to April 11 implies. We assume some loss of momentum in the week to April 18, the week of the monthly survey. The positive signals from the weekly ADP data are consistent with low initial claims and renewed slippage in continued claims, as well as increased labor market optimism in the Conference Board’s April consumer confidence report.

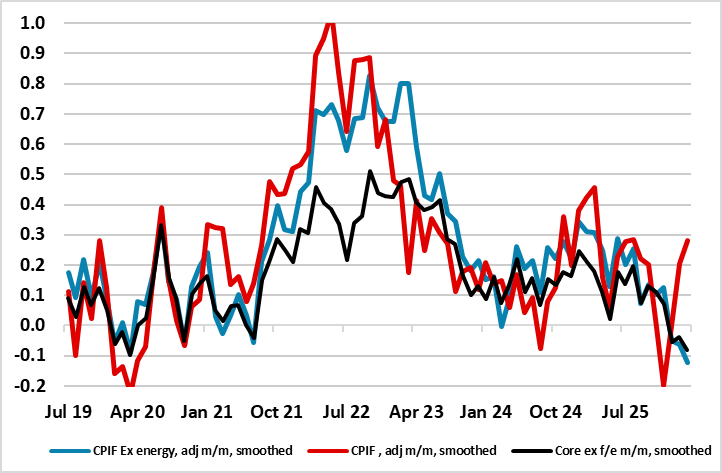

Figure: Core CPI Inflation Still Surprising to the Downside

Sweden sees the next Riksbank verdict on May 7, a decision that will not come with fresh official projections. But with inflation (Figure) and real economy numbers having undershot both its and consensus expectations, the Riksbank might have been contemplating a fresh easing at this juncture if not for events in Middle East. But stable policy seems to be the accepted alternative in current circumstances and this will be the verdict next Thursday, even if it is accompanied by less friendly rhetoric. More likely, the Board will repeat its assertion of no change for some time to come but still qualified it somewhat by noting that amid Middle East conflict making the outlook very uncertain, it would adjust monetary policy if the outlook for inflation and economic activity so requires – this presumably suggesting a move in either direction.

We expect Canadian employment to increase by 10k in March, a second straight modest rise to follow a gain of 14.1k in March, still not close to erasing the steep loss of 83.9k in February which extended a substantial 24.8k decline in January. We expect a 6.7% unemployment rate for a third straight month. This would be consistent with an economy entering Q2 with only modest momentum, growing but struggling to make a significant dent in the output gap. The hit from tariffs is fading while higher energy prices will have a mixed impact on Canadian GDP, but will probably act as a net restraint on job growth. January and February weakness was probably influenced by weather but can also be seen as corrective from overstated gains in September. October and November of 2025, each of which exceeded 50k.

For the Week Ahead

UK

Coming before final PMI data (Wed), Thursday sees construction PMI data as well in what is a holiday shortened week. But the focus of the week are the elections on Thursday. The biggest set of elections since the 2024 general election will see millions of UK voters head to the polls on 7 May. Voters in Scotland and Wales will elect representatives to their two respective national parliaments, while a wide number of local council and mayoral polls will take place in England, with major ones occurring in Greater London. Already, UK markets are fretting about the possible outcome, in particular that serious electoral damage to the Labour Party currently running the government could make it swing more to left and dilute fiscal prudence with or without a change in PM. This is a clear risk, but it is not the only one.

Eurozone

Data wise final manufacturing and services PMI numbers (Mon/Wed) and then the construction counterpart (Thu). Retail sales and PPI data will attract little attention. Otherwise, the week ends with German orders (Thu) and industrial production on Friday, the latter likely to see a further m/m correction back.

Rest of Western Europe

Sweden sees the Riksbank verdict (Thu). With inflation and real economy numbers having undershot both its and consensus expectations, the Riksbank might have been contemplating a fresh easing if not for events in Middle East. But stable policy seems to be the accepted alternative in current circumstances and this will be the verdict next Thursday, even if it is accompanied by less friendly rhetoric. More likely it will repeat its assertion of no change for some time to come but still qualified it somewhat by noting that amid Middle East conflict making the forecast very uncertain, it would adjust monetary policy if the outlook for inflation and economic activity so requires – this presumably suggesting a move in either direction. Flash April CPI numbers due Wednesday will make little difference to Board thinking

Switzerland also sees CPI data with headline likely to rise further from March’s 0.3% y/y. Norway sees the next Norges Bank decision next Thursday and while we acknowledge the hawkish and active manner of the Board we adhere to a stable policy decision, not least given the similar verdicts its neighbouring central banks we think will have offered by then.

USA

US data focus will be on the labor market, particularly Friday’s non-farm payroll for April. We expect a respectable 90k increase, 95k in the private sector, with a 0.3% rise in average hourly earnings and a fall in unemployment to 4.2% from 4.3%. Weekly data suggests Wednesday’s ADP report on private payrolls could outperform the non-farm payroll, following underperformance in March. We expect a 140k increase. Other labor market indicators include March’s JOLTS report on job openings on Tuesday, while Thursday sees Q1 productivity and costs and weekly initial claims. The latter will be of interest after a preceding fall to the lowest level since 1969.

Monday sees March factory orders. On Tuesday we expect March’s trade deficit to increase to $60.4bn from $57.3bn and April’s ISM services index to incase to 54.5 from 54.0. Also due are new home sales for both February and March. We see both months at 675k, up from a below trend 587k in January. Thursday also sees construction spending for both February and March followed by March consumer credit while Friday also sees the preliminary May Michigan CSI and March wholesale sales. Fed speakers scheduled include Williams on Monday, Musalem and Goolsbee on Wednesday, Hammack and Williams again on Thursday, and Goolsbee again on Friday.

CANADA

Canada releases April employment data on Friday. We expect a modest 10k increase with an unchanged unemployment rate of 6.7%. Also due are March’s trade balance and April’s S and P services PMI on Tuesday and April’s Ivey manufacturing PMI on Wednesday.

JP

Quite a quiet calendar for Japan next week with a few holiday. Labor Cash Earning for march will be released on Thursday an it will be critical. The key reason for BoJ to delay hiking is the possibility of wage slowing in sight of rising energy cost and lower business margin. If we see a below 2% growth, it could mean the BoJ is right. Else, June hike remains on the card. We also have BoJ minutes on the same day but it wouldn’t provide things we do not already know.

AU

The RBA rate decision is on Tuesday and very likely we will see another 25bps move as the RBA looks set to hike to keep inflation in check. The Australian inflation picture is double teamed by rising underlying demand and oil shock, which are more than enough to convince the RBA to tighten. However, the forward guidance will be important as most market participants are not seeing more than one more hike in 2026. If the RBA go all hawkish, market pricing will significantly change and drive the Aussie higher. We also have private inflation on Monday. PMIs on Tuesday and the more important trade balance on Thursday.

NZ

Labors data and wage will be important to watch for the Kiwi on Wednesday.

Recap of the Week

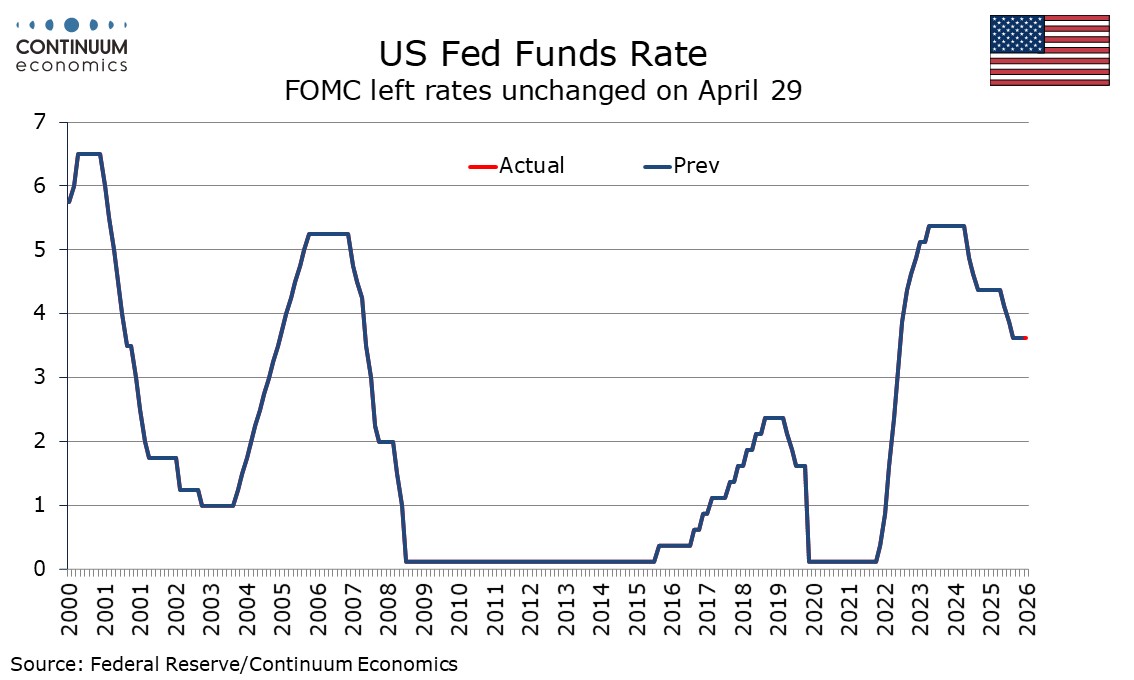

FOMC keeps rates on hold but three of four dissents are hawkish

BoE MPC Playing Its Cards Safe

ECB Mixed Communications

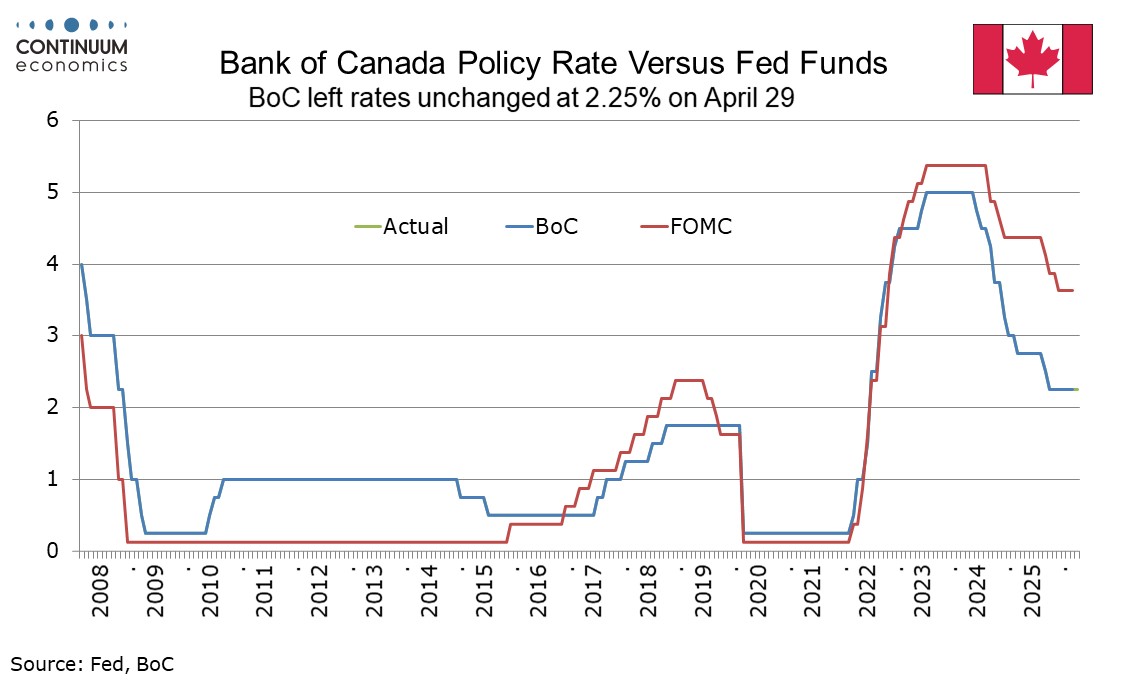

Bank of Canada Policy seen appropriate under baseline assumption

BoJ Slightly Hawkish Hold

The main surprise in the FOMC statement was the number of dissents, one dovish, Miran continuing to call for a 25bps easing, and three hawkish, with Hammack, Kashkari and Logan in agreement with the decision to leave rates unchanged but objecting to the inclusion of an easing bias. This means three of the four rotating regional voters made hawkish dissents, the exception being Philly Fed’s Paulson, and it is likely some of the non-voting regional presidents hold similar views. That none of the permanent voters dissented is however significant, suggesting Warsh, who is likely to Chair the next meeting, may be able to count on a majority of votes, though once Warsh enters Miran will exit.

The easing bias is not strongly explicit, the statement repeating a reference to the extent and timing of additional adjustments, but the three hawkish dissenters appear to want it made clear that adjustments could go in either direction, something that recent minutes have suggested was advocated by some. In the assessment of the economy the statement is a little more hawkish, the qualifier on average added to the view that job gains remain low, and inflation now described as elevated rather than somewhat elevated, with energy prices now noted explicitly as a factor. The statement is also more explicit about the role developments in the Middle East are playing in contributing to high uncertainty.

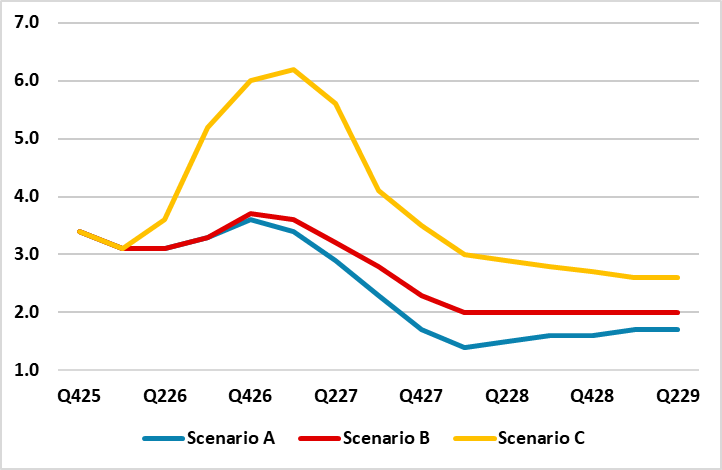

Figure: The BoE’s Three Scenarios

Very clearly, the BoE kept rates on hold with the MPC last month and the same decision was both expected and delivered this time around but with only token fresh dissent, with Chief Economist Pill wanting an immediate hike from the current 3.75%. But splits were more evident in the individual MPC member statements (as expected) where more diverging views in an around the three scenarios that the BoE is now projections all based on modest hiking of around 50 bp over the coming year. We still think that the BoE is offering too much information in these individual views and as a result is confusing markets just as it did in March. But among the key and relatively common themes is that financial conditions have tightened even without actual hikes and that the labor market is loosening. And it this tightening that pulls policy severely back towards conditions when Bank Rate peaked that makes up see a much softer real economy outlook than the strangely similar GDP outlooks in all of the BoE scenarios.

What is notable and as the updated projections do show, is that this energy shock is justifiably viewed by the BoE as being different to that of 2022, occurring at a point when the economy is operating with a margin of spare capacity and where policy is already restrictive. We think this very much reduces the chances of second round effects as does the already loosening labor market where earrings growth have slowed to a rate consistent with the 2% inflation target.

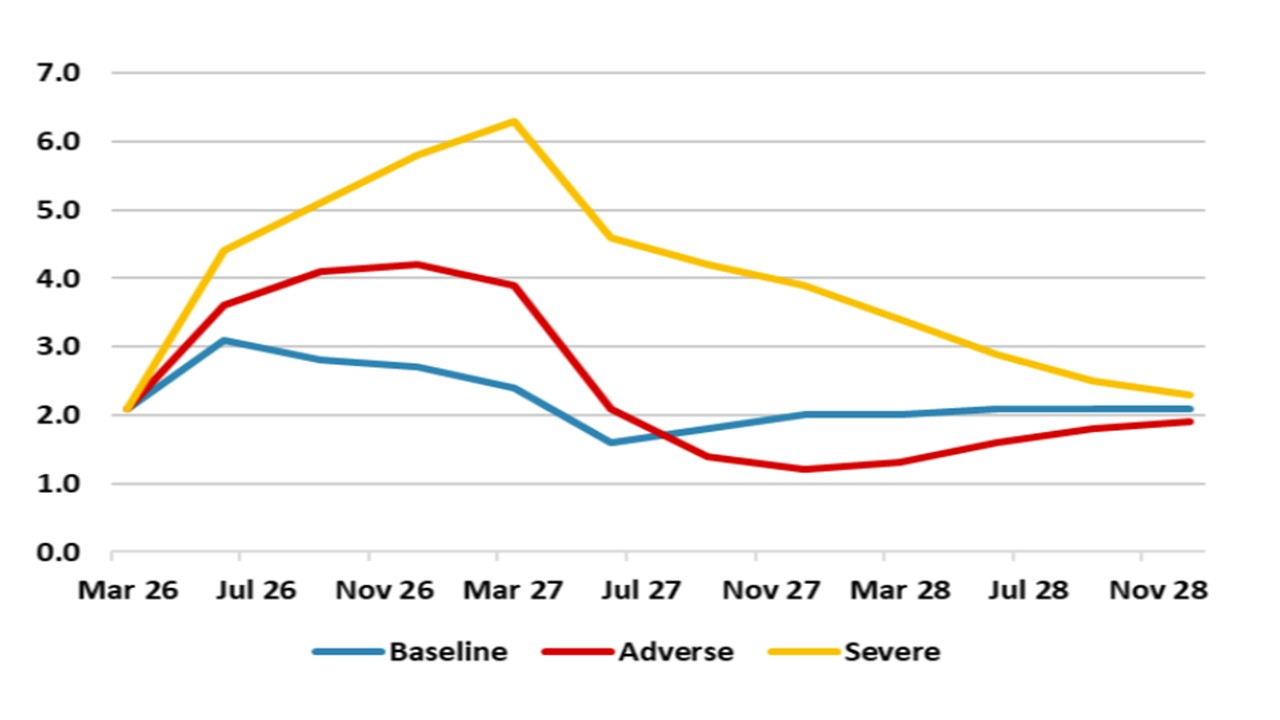

Figure: EZ HICP Including Projections From March Forecasts (%)

Overall, the June and July meetings have live risks that the ECB could undertake a modest 25bps hike. If a partial reopening of the Straits of Hormuz occurs then the ECB will likely keep hawkish, but not actually hike. We feel that the ECB is overestimating natural gas prices, while financial conditions and the economy argue for caution against hiking. Lagarde did note in the Q/A that financial conditions tightening is evident. The odds would then be that the ECB does not hike in 2026. Alternatively, if the Straits of Hormuz is still closed by the June 11 meeting, then the hawks could be able to push a 25bps hike through at the June meeting or commit to a move in July. The doves would counter that 2nd round wage effects are absent meaning a hike would not be guaranteed.

The Bank of Canada left rates unchanged at 2.25% as expected and Governor Macklem sees policy as appropriate under a BoC baseline that assumes oil prices evolves according to market expectations and US tariff rates remaining unchanged. This supports our view for steady BoC policy through 2026, though Macklem added that policy may need to be nimble given unusually elevated uncertainty. The BoC is prepared to move in either direction, but tightening later in the year is probably a greater risk than easing.

Oil prices are assumed to decline to around $75 per barrel by the middle of next year and if that happens CPI, which increased to 2.4% in March from, 1.8% in February, is seen peaking at around 3% in April and easing back to the 2% target by early next year. Independent of the oil shock, CPI is due for an acceleration in April due to the April 2025 abolition of the carbon tax lifting the base.

The BoJ has kept rates unchanged at 0.75% in the April meeting with three votes dissent that is looking for another 25bps hike. There hasn't been any changes to BoJ's stance of more hike but the geopolitical tension in Middle East may have a temporary negative effect on wage growth in Q2. It led the BoJ to revise their economic forecast for 2026 lower before rebounding in 2027. Inflation forecast is revised higher to 2.5-3% in 2026 before rotating lower in 2027 and reaching target at 2028.

The geopolitical disruption is unlikely to derail BoJ's plan to further tighten as the business wage/price setting momentum has gained traction. Their major concern lies on short term wage growth slowdown on lower business margin. Their 2026 GDP forecast is halved from January forecast of 1%. Core CPI0.9% higher while core-core CPI 0.4% higher than earlier expectation.

We suspect Ueda will sound more hawkish than usual in his press conference with no change in forward guidance. They are assessing the situation in Middle East and should hike as early as in the June meeting if energy disruption is eased.